how to build a personal budget: Managing money has become more challenging than ever. Rising living costs, subscription services, unexpected bills, and changing financial priorities can make it feel like your paycheck disappears before the month ends.

If you’ve ever wondered where your money went, you’re not alone. Millions of households struggle with budgeting—not because they don’t earn enough, but because they don’t have a realistic spending plan.

The good news is that learning how to build a personal budget doesn’t require complicated spreadsheets or financial expertise. A practical budget simply helps you decide where your money should go before you spend it.

Whether you’re saving for a home, paying off debt, building an emergency fund, or simply trying to stop living paycheck to paycheck, a well-designed personal budget gives every dollar a purpose.

This guide explains exactly how to create a budget that works in 2026 using simple, practical steps that are easy to follow and maintain.

A Story Almost Everyone Can Relate To

Emma had a stable full-time job and earned a respectable salary every month. Yet by the third week of each month, she often found herself checking her bank balance before buying groceries.

She wasn’t overspending on luxury items. Instead, dozens of small purchases, recurring subscriptions, online shopping, and restaurant meals quietly consumed her income.

After creating a simple personal budget, everything changed. She identified unnecessary expenses, started saving automatically, and finally built an emergency fund.

Within one year, Emma paid off her credit card balance and reduced much of her financial stress.

Her story isn’t unique. A realistic budget can completely change the way you manage money.

What You’ll Learn

By the end of this guide, you’ll understand:

- What a personal budget actually is

- Why budgeting matters

- How to calculate your income correctly

- The easiest way to track expenses

- Common budgeting mistakes to avoid

- Practical budgeting strategies

- How to build long-term financial confidence

Let’s begin with the foundation of every successful financial plan. how to build a personal budget

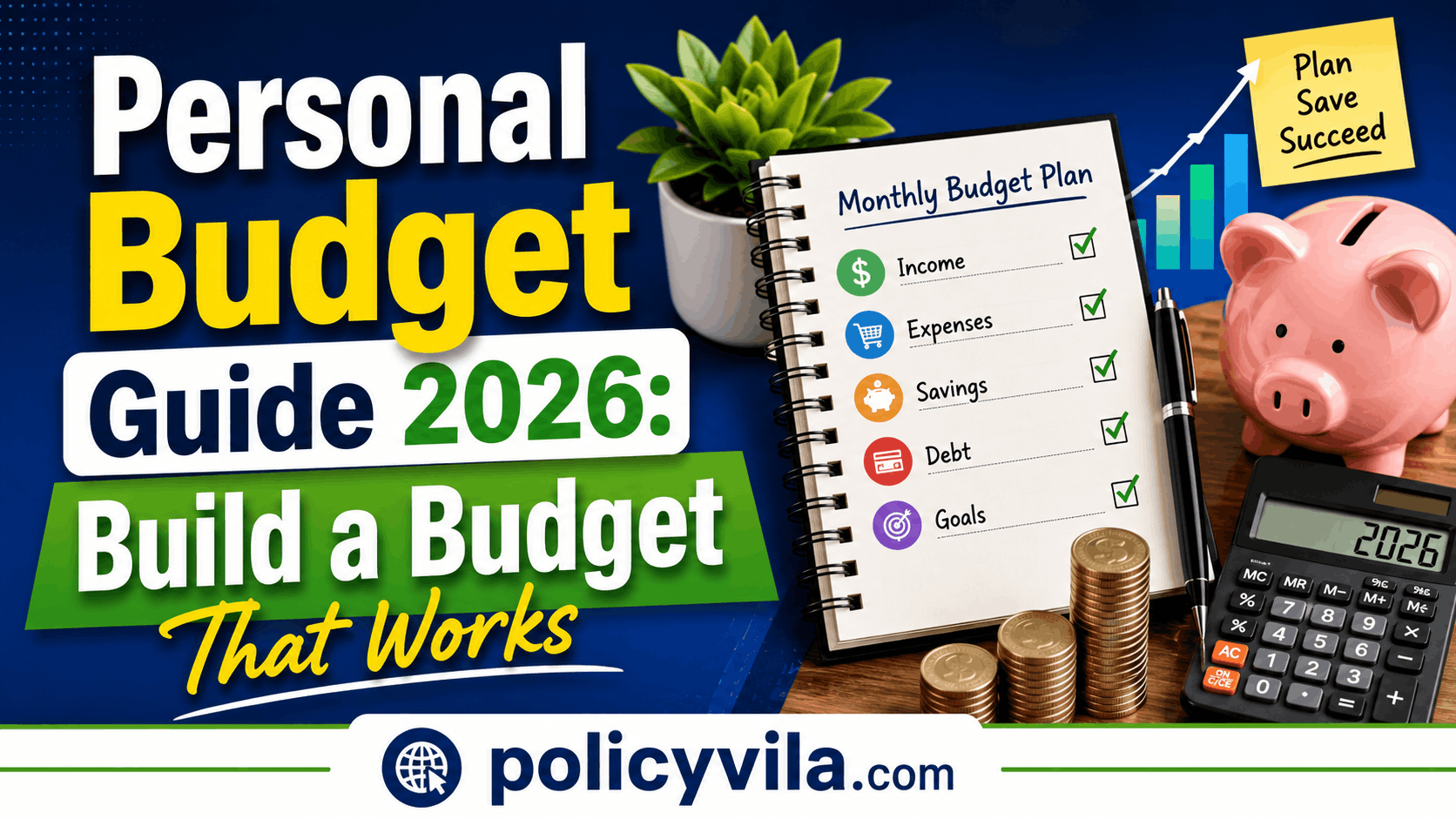

What Is a Personal Budget?

A personal budget is a financial plan that outlines how much money you earn, how much you spend, and how much you save during a specific period, usually one month.

Instead of asking where your paycheck disappeared, a budget helps you decide in advance where every dollar should go.

Think of a budget as a roadmap for your finances. Just as a GPS helps you reach your destination efficiently, a budget guides your money toward your financial goals.

A well-designed personal budget typically includes:

- Monthly income

- Fixed expenses

- Variable expenses

- Savings contributions

- Debt payments

- Financial goals

The goal of budgeting is not to stop spending money.

The goal is to spend with purpose.

Why Budgeting Matters

Without a budget, it’s easy to underestimate spending.

Small purchases that seem harmless individually can quietly consume hundreds or even thousands of dollars each year.

A realistic budget helps you:

- Understand spending habits

- Build savings consistently

- Prepare for emergencies

- Reduce unnecessary debt

- Reach financial goals faster

- Lower financial stress

Budgeting also helps you make major life decisions with greater confidence, including buying a home, changing careers, starting a family, or planning retirement.

Common Budgeting Myths

Many people avoid budgeting because they believe it is restrictive or complicated.

Myth: Budgets are only for people with financial problems.

Reality: Successful people use budgets to build wealth and stay financially organized.

Myth: Budgeting means you can’t enjoy life.

Reality: A good budget allows spending on entertainment while protecting long-term financial goals.

Myth: Budgeting is difficult.

Reality: Most effective budgets are surprisingly simple.

Myth: I already know where my money goes.

Reality: Most people underestimate monthly spending until they begin tracking every expense.

Why Every Household Needs a Budget in 2026

Economic conditions continue to evolve. Inflation, housing costs, healthcare expenses, higher interest rates, and rising everyday expenses make budgeting more valuable than ever.

A practical budget allows households to stay financially stable regardless of economic uncertainty. how to build a personal budget

Rising Cost of Living

Everyday expenses continue increasing.

Housing, groceries, transportation, utilities, insurance, and healthcare consume a larger share of household income than they did only a few years ago.

Without careful planning, these higher costs gradually reduce savings.

Inflation Impacts Purchasing Power

Inflation means the same amount of money buys fewer goods and services over time.

Budgeting helps families adjust spending before financial pressure becomes overwhelming.

Better Emergency Preparedness

Unexpected expenses happen when you least expect them.

Examples include:

- Medical emergencies

- Car repairs

- Home maintenance

- Job loss

- Emergency travel

A budget allows you to build an emergency fund before these situations arise.

Easier Debt Management

Budgeting clearly shows how much money can safely be directed toward paying debt each month.

This reduces missed payments and helps lower interest costs over time.

Saving for Future Goals

Whether your goal is purchasing a home, paying for education, taking a dream vacation, or retiring comfortably, budgeting provides a realistic savings plan.

Every dollar saved intentionally moves you closer to your goals.

Less Financial Stress

Financial uncertainty creates anxiety.

Knowing your bills are covered, your savings are growing, and your spending is under control provides confidence and peace of mind.

Budgeting is not just about money.

It is about creating financial stability for yourself and your family.

Step 1: Calculate Your Monthly Income

Before creating a personal budget, determine exactly how much money enters your household every month.

Many budgeting problems begin because people estimate their income instead of calculating it accurately.

Include Every Income Source

Your monthly income may include:

- Full-time salary

- Part-time wages

- Freelance work

- Business income

- Rental income

- Investment income

- Side hustles

- Government benefits where applicable

Gross Income vs. Net Income

Understanding the difference is essential.

Gross income is the amount earned before taxes and deductions.

Net income is the amount deposited into your bank account after taxes, retirement contributions, and insurance deductions.

For budgeting purposes, most financial experts recommend using net income because it reflects the money you actually have available.

Practical Example

Suppose Sarah earns:

- Salary: $4,800

- Freelance writing: $600

- Online tutoring: $400

Total monthly income:

$5,800

This becomes the starting point for building her monthly budget.

Budgeting with Variable Income

Freelancers, contractors, and business owners often experience fluctuating monthly income.

Instead of budgeting based on your highest-income month, calculate your average income over the past six to twelve months.

This creates a more stable financial plan.

Step 2: Track Every Monthly Expense

After calculating your income, identify exactly where your money goes.

Expense tracking is often the biggest eye-opener for first-time budgeters.

Many people discover they spend far more than expected on everyday purchases.

Fixed Expenses

Fixed expenses usually remain consistent each month.

Examples include: how to build a personal budget

- Rent or mortgage

- Auto loans

- Insurance premiums

- Internet service

- Phone bills

- Student loans

- Personal loans

- Subscription services

Because these expenses rarely change, they are easier to plan for.

Variable Expenses

Variable expenses change from month to month.

Examples include:

- Groceries

- Fuel

- Dining out

- Coffee

- Shopping

- Entertainment

- Household supplies

- Gifts

These categories usually offer the greatest opportunity to reduce spending.

Small Purchases Matter

Buying coffee every workday for six dollars may not seem expensive.

However:

$6 × 22 working days equals $132 each month.

Over one year, that’s $1,584.

Tracking spending helps uncover hidden habits like these before they damage your financial goals.

Easy Ways to Track Spending

You don’t need expensive software.

Simple options include:

- Budget notebook

- Spreadsheet

- Printable budget worksheet

- Expense tracker

- Mobile budgeting app

- Bank account history

Step 3: Set Clear Financial Goals

Once you understand your income and expenses, the next step is deciding what you want your money to accomplish. A budget without goals often fails because there’s no clear purpose behind the numbers.

Financial goals help you stay motivated and make smarter spending decisions. Instead of asking, “Can I afford this?” you’ll start asking, “Does this purchase help me reach my goals?”

Set Short-Term Goals

Short-term goals are usually achieved within one year.

Examples include:

- Build a $1,000 emergency fund

- Pay off a credit card

- Save for a vacation

- Buy a new laptop

- Cover holiday expenses

These smaller achievements build confidence and encourage consistent budgeting.

Set Long-Term Goals

Long-term goals often take several years to achieve.

Examples include:

- Buying a home

- Paying off student loans

- Saving for retirement

- Starting a business

- Paying for a child’s education

Your monthly budget should include money set aside specifically for these long-term objectives.

Use SMART Financial Goals

A goal should be:

| SMART Principle | Example |

|---|---|

| Specific | Save for a house down payment |

| Measurable | Save $15,000 |

| Achievable | Save $500 every month |

| Relevant | Supports long-term financial security |

| Time-Bound | Reach goal within 30 months |

SMART goals make progress easier to track and help prevent frustration.

Step 4: Choose the Right Budgeting Method

Not every budgeting method works for everyone. The best budget is the one you can realistically follow month after month.

Fortunately, several proven budgeting systems have helped millions of people take control of their finances.

The 50/30/20 Budget Rule

This is one of the simplest budgeting methods.

Your after-tax income is divided into three categories:

- 50% for needs

- 30% for wants

- 20% for savings and debt repayment

This approach is easy for beginners and offers flexibility.

Zero-Based Budget

With zero-based budgeting, every dollar has a specific purpose.

Income minus expenses equals zero—not because you’ve spent everything, but because every dollar has been assigned to bills, savings, investments, or debt payments.

This method provides maximum control over spending.

Pay Yourself First

Instead of saving whatever money remains at the end of the month, you save first.

As soon as you receive your paycheck, transfer money into: how to build a personal budget

- Savings

- Retirement accounts

- Investments

Then use the remaining income for monthly expenses.

This method helps build wealth consistently.

Envelope Budgeting

Traditionally, cash is divided into envelopes for different spending categories.

For example:

- Groceries

- Entertainment

- Dining Out

- Shopping

When an envelope becomes empty, spending stops for that category until next month.

Today, many people use digital versions of this system.

Budgeting Method Comparison

| Budgeting Method | Best For | Advantages | Disadvantages |

|---|---|---|---|

| 50/30/20 Rule | Beginners | Simple and flexible | Less detailed |

| Zero-Based Budget | Families & debt payoff | Maximum spending control | Requires more planning |

| Pay Yourself First | Savers | Builds savings automatically | Doesn’t track spending closely |

| Envelope Budget | Overspenders | Controls impulse spending | Less convenient for digital payments |

There is no universally perfect budgeting system.

Choose the one that matches your lifestyle and financial habits.

Step 5: Build Your Monthly Budget

Now it’s time to combine everything you’ve learned into a practical monthly budget.

Start with your monthly income, then allocate money toward each spending category before the month begins.

Every dollar should have a purpose.

Sample Monthly Budget

Suppose your monthly net income is $5,000.

| Category | Monthly Amount |

|---|---|

| Housing | $1,400 |

| Utilities | $250 |

| Groceries | $600 |

| Transportation | $350 |

| Insurance | $300 |

| Debt Payments | $500 |

| Savings | $700 |

| Entertainment | $350 |

| Miscellaneous | $300 |

| Total | $5,000 |

This example demonstrates balanced spending while still prioritizing savings.

Separate Needs from Wants

One of the easiest ways to improve your budget is learning the difference between essential expenses and discretionary spending.

Needs

Needs are expenses required for daily living.

Examples include:

- Housing

- Utilities

- Groceries

- Insurance

- Transportation

- Basic healthcare

Wants

Wants improve your lifestyle but aren’t essential.

Examples include:

- Streaming subscriptions

- Dining out

- Designer clothing

- Premium electronics

- Vacations

- Entertainment

Reducing wants—not eliminating them entirely—creates room for higher savings and faster debt repayment.

Leave Room for Unexpected Expenses

Every month brings surprises.

You might need:

- Car maintenance

- Home repairs

- Medical expenses

- School supplies

- Gifts

- Pet care

Including a small miscellaneous category in your budget prevents these unexpected costs from disrupting your financial plan.

Don’t Aim for Perfection

Many people quit budgeting because their first month doesn’t go exactly as planned.

Remember that budgeting is a process of continuous improvement.

Your budget should evolve as:

- Income changes

- Expenses increase

- Family size changes

- Financial goals change

Review your budget every month and make adjustments when necessary. how to build a personal budget

Step 6: Reduce Unnecessary Spending

One of the fastest ways to improve your budget isn’t earning more money—it’s spending more intentionally. Most households have at least a few expenses they can reduce without significantly affecting their quality of life.

The goal isn’t to eliminate everything you enjoy. Instead, identify spending that doesn’t provide enough value.

Review Your Monthly Subscriptions

Subscription services can quietly drain your budget because payments happen automatically.

Take a few minutes to review your bank or credit card statement and look for recurring charges.

Examples include:

- Streaming services

- Music subscriptions

- Fitness memberships

- Cloud storage plans

- Premium apps

- Magazine subscriptions

Ask yourself:

- Do I still use this service?

- Is it worth the monthly cost?

- Can I switch to a cheaper plan?

Canceling just two unused subscriptions could save hundreds of dollars each year.

Reduce Impulse Purchases

Impulse spending is one of the biggest reasons budgets fail.

Instead of buying immediately, try using the 24-hour rule.

Wait one full day before purchasing non-essential items.

You’ll often discover you don’t really need them.

Cook More Meals at Home

Eating out is convenient, but restaurant meals add up quickly.

For example:

- Lunch: $15

- Five workdays: $75

- One month: About $300

Preparing meals at home can significantly reduce monthly expenses while improving your overall health.

Shop With a List

Whether you’re shopping for groceries or household items, always use a list.

A shopping list helps you:

- Stay focused

- Avoid impulse purchases

- Compare prices

- Reduce unnecessary spending

Compare Prices Before Buying

Don’t purchase expensive items immediately.

Compare prices online and in stores.

Even a small discount can make a noticeable difference over multiple purchases. how to build a personal budget

Avoid Lifestyle Inflation

As income increases, many people automatically increase spending.

Instead of upgrading everything after receiving a raise, consider directing part of the extra income toward:

- Savings

- Investments

- Debt repayment

Your future self will thank you.

Step 7: Automate Your Savings

Saving money becomes much easier when you remove the need to think about it every month.

Automation helps eliminate temptation and ensures your financial goals remain a priority.

Save Before You Spend

Many people save whatever money remains at the end of the month.

Unfortunately, very little often remains.

Instead, treat savings like any other monthly bill.

Schedule an automatic transfer immediately after payday.

Build an Emergency Fund

Financial emergencies happen to everyone.

A strong emergency fund can help cover:

- Medical bills

- Vehicle repairs

- Home maintenance

- Temporary job loss

- Unexpected travel

Many financial experts recommend saving enough to cover three to six months of essential living expenses.

Automate Retirement Contributions

If your employer offers a retirement plan, consider automatic contributions.

Small monthly investments made consistently over many years can grow significantly through compound growth.

Automate Bill Payments

Automatic bill payments help you: how to build a personal budget

- Avoid late fees

- Protect your credit history

- Reduce stress

- Simplify money management

Just make sure sufficient funds are available before payments are processed.

Step 8: Review and Adjust Your Budget Every Month

A budget is not something you create once and forget.

Life changes constantly, and your budget should change with it.

Reviewing your budget monthly helps you stay on track and identify areas for improvement.

Compare Budgeted vs Actual Spending

At the end of each month, compare:

- Planned spending

- Actual spending

Ask yourself:

- Which categories stayed within budget?

- Which categories exceeded expectations?

- Why did the differences occur?

Small adjustments each month lead to long-term success.

Update Income Changes

If your income increases because of:

- Promotions

- Bonuses

- Freelance work

- Side businesses

Update your budget accordingly.

Try increasing savings before increasing lifestyle spending.

Prepare for Seasonal Expenses

Some expenses occur only once or twice each year.

Examples include:

- Holiday shopping

- School supplies

- Property taxes

- Vehicle registration

- Insurance renewals

Planning ahead prevents these costs from disrupting your monthly finances.

Celebrate Progress

Budgeting should feel rewarding.

Celebrate milestones such as: how to build a personal budget

- Paying off a loan

- Reaching a savings goal

- Staying within budget for three consecutive months

Choose affordable rewards that don’t undo your financial progress.

15 Smart Budgeting Tips to Save More and Stress Less

Even small changes can produce meaningful financial improvements over time.

Here are fifteen practical budgeting habits that actually work.

1. Track Every Dollar

Knowing where your money goes is the foundation of every successful budget.

2. Create Realistic Spending Limits

Unrealistic budgets often fail within weeks.

Build a budget you can actually follow.

3. Build an Emergency Fund First

Unexpected expenses are inevitable.

Savings reduce financial stress.

4. Plan Meals Before Grocery Shopping

Meal planning reduces food waste and lowers grocery costs.

5. Shop With a List

Avoid unnecessary purchases by knowing exactly what you need.

6. Cancel Unused Subscriptions

Small recurring charges become expensive over time.

7. Pay Bills On Time

Avoid late fees and protect your credit history.

8. Avoid Emotional Spending

Stress, boredom, and excitement often lead to unnecessary purchases.

Pause before buying.

9. Compare Prices

Always look for discounts before making major purchases.

10. Increase Income When Possible

A side hustle or freelance work can accelerate your financial goals.

11. Save Windfalls

Tax refunds, bonuses, and gifts can boost your savings instead of increasing spending.

12. Review Bank Statements Monthly

Look for forgotten subscriptions, duplicate charges, or unusual spending.

13. Use Cash for Flexible Spending Categories

Cash naturally limits overspending in categories like entertainment and dining out.

14. Review Your Goals Regularly

Financial priorities change.

Update your budget to match your current goals.

15. Stay Consistent

Perfect budgets don’t exist.

Consistent budgeting produces long-term financial success.

Remember that budgeting isn’t about restricting your lifestyle.

Common Budgeting Mistakes to Avoid

Even the best budgeting plan can fail if you make a few common mistakes. Fortunately, most budgeting errors are easy to fix once you recognize them.

Setting Unrealistic Spending Limits

One of the biggest reasons people abandon their budgets is because they make them too restrictive.

For example, if you usually spend $500 a month on groceries, reducing your budget to $200 overnight is unlikely to be sustainable.

Instead, make gradual improvements that fit your lifestyle.

Forgetting Annual or Irregular Expenses

Many people only budget for monthly bills and forget expenses that occur once or twice a year.

Examples include: how to build a personal budget

- Car registration

- Property taxes

- Holiday gifts

- School supplies

- Home maintenance

- Annual insurance premiums

Divide these expenses by 12 and save a small amount every month so they don’t become financial surprises.

Ignoring Small Purchases

A coffee here, an online subscription there, and a few impulse purchases may not seem significant.

However, dozens of small expenses every month can quietly cost hundreds or even thousands of dollars each year.

Track every purchase, no matter how small.

Not Building an Emergency Fund

Without emergency savings, unexpected expenses often lead to credit card debt or personal loans.

Even saving a small amount each month creates a financial safety net over time.

Failing to Review Your Budget

A budget should never remain unchanged forever.

Income, expenses, and financial priorities change throughout the year.

Review your budget at least once every month.

Giving Up Too Quickly

Nobody creates the perfect budget on the first attempt.

Budgeting is a skill that improves with practice.

If one month doesn’t go according to plan, adjust your budget and continue moving forward.

Progress is more important than perfection.

Budgeting Tools That Can Help

You don’t need expensive software to manage your money successfully.

Many simple tools can help you stay organized and monitor your spending.

Budget Spreadsheets

Spreadsheets are popular because they allow complete customization.

You can create categories, track expenses, calculate savings, and monitor progress with basic formulas.

They’re an excellent option for people who enjoy detailed financial planning.

Budget Journals

Some people prefer writing everything down.

A budgeting journal helps you:

- Record daily spending

- Set financial goals

- Review monthly progress

- Stay accountable

Writing expenses by hand can also make spending habits more noticeable.

Mobile Budgeting Apps

Budgeting apps automatically categorize many expenses and provide real-time spending updates.

Features often include:

- Expense tracking

- Savings goals

- Bill reminders

- Spending alerts

- Monthly reports

Choose an app that fits your needs and protects your personal information.

Expense Trackers

Expense trackers focus primarily on recording purchases rather than creating a complete budget.

They’re ideal for identifying spending patterns before building a full budgeting system.

Bank Budgeting Features

Many banks now include built-in budgeting tools within online and mobile banking platforms.

These features may automatically: how to build a personal budget

- Categorize transactions

- Display spending summaries

- Show monthly trends

- Track savings goals

Since these tools are connected to your accounts, they can simplify everyday money management.

Frequently Asked Questions

How do I build a personal budget?

Start by calculating your monthly income, tracking every expense, setting financial goals, choosing a budgeting method, and reviewing your budget regularly. The key is creating a realistic plan you can consistently follow.

What is the best budgeting method?

There isn’t one perfect budgeting method for everyone. Popular options include the 50/30/20 Rule, Zero-Based Budgeting, Pay Yourself First, and Envelope Budgeting. Choose the system that best matches your financial habits and goals.

How much should I save every month?

A common recommendation is to save at least 20% of your income if possible. However, even smaller amounts saved consistently can make a significant difference over time.

Is budgeting difficult?

No. Budgeting becomes much easier after you understand your income and spending patterns. Most successful budgets are simple and only require regular review.

Should I budget if I have debt?

Absolutely. A budget helps you prioritize debt payments while still covering essential expenses and building savings for emergencies.

How often should I update my budget?

Review your budget every month. Update it whenever your income, expenses, or financial goals change.

Can budgeting improve my credit score?

Budgeting itself doesn’t directly affect your credit score. However, it helps you pay bills on time, reduce debt, and avoid missed payments, all of which support a healthier credit profile.

What if my income changes every month?

If your income varies, calculate your average monthly income using the previous six to twelve months. Budget conservatively and adjust as your earnings change.

Is the 50/30/20 Rule still effective?

Yes. The 50/30/20 Rule remains one of the simplest budgeting methods in 2026, although some households may need to adjust the percentages based on housing costs and local living expenses.

How long does it take to see budgeting results?

Many people notice improvements within the first month. Larger goals, such as paying off debt or building significant savings, usually take several months or years depending on consistency.

Final Verdict

Learning how to build a personal budget is one of the most valuable financial skills you can develop.

A budget isn’t designed to limit your freedom—it gives you greater control over your money and helps you make confident financial decisions.

By understanding your income, tracking expenses, choosing the right budgeting method, reducing unnecessary spending, and reviewing your progress every month, you create a strong foundation for long-term financial success.

Remember that no budget is perfect. Your financial situation will continue to change throughout your life, and your budget should evolve with it.

The most successful budget isn’t the most detailed one.

It’s the one you can consistently follow.

Conclusion

A successful personal budget is about giving every dollar a purpose rather than restricting every purchase. When you know exactly where your money is going, you gain confidence, reduce financial stress, and make steady progress toward your goals.

Whether you’re building an emergency fund, paying off debt, saving for a home, or planning for retirement, consistent budgeting can help you get there faster. Small improvements made month after month often produce remarkable long-term results.

Start with a simple plan, review it regularly, and don’t be discouraged by occasional setbacks. Financial success isn’t achieved through perfection—it’s built through consistency, discipline, and smart decisions repeated over time. The sooner you begin, the sooner you’ll experience the peace of mind that comes from taking control of your financial future. how to build a personal budget