Introduction

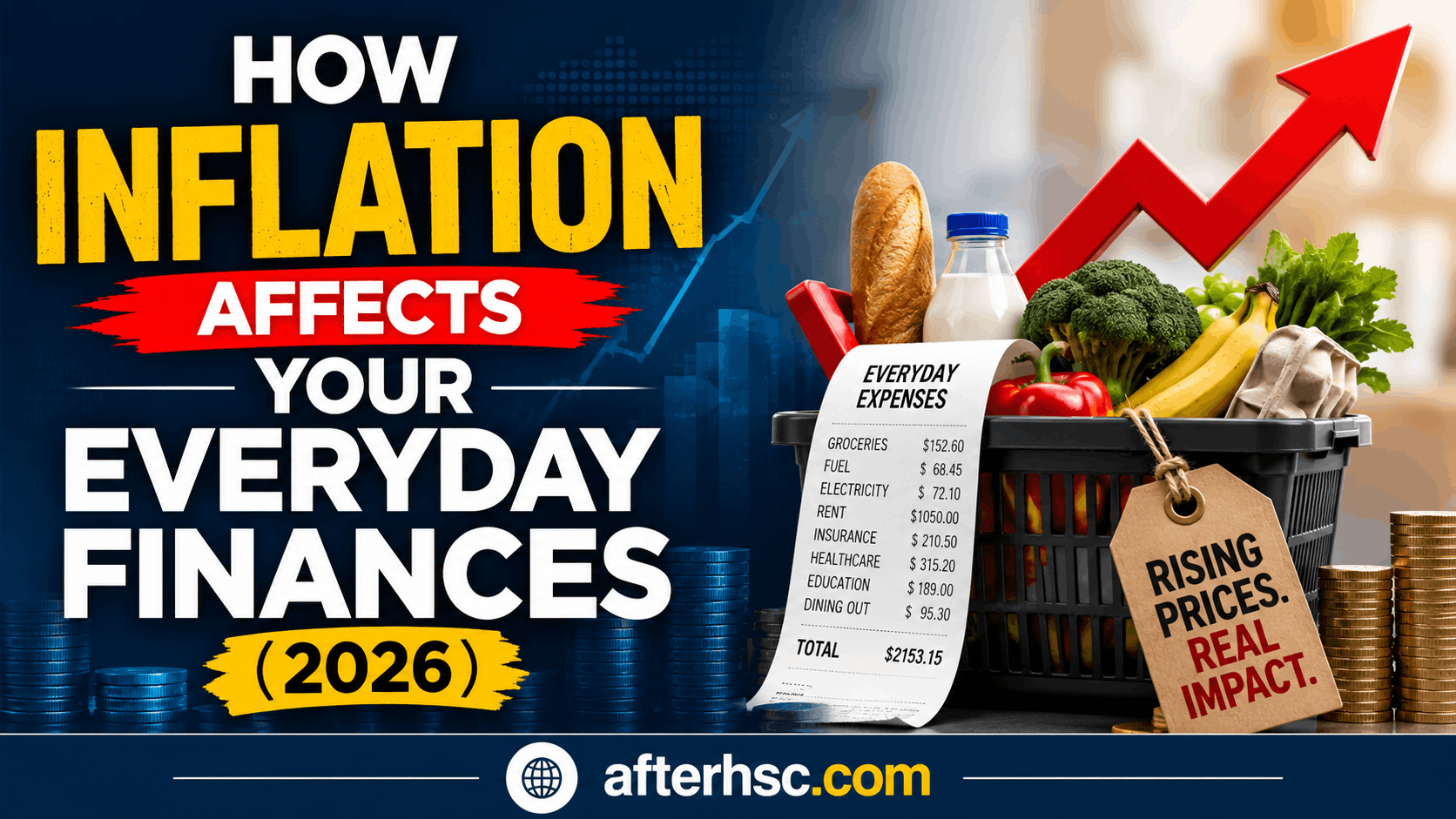

How Inflation Affects Your Everyday Finances: Have you ever looked at your grocery receipt and wondered why it keeps getting longer even though you bought the same items as last month? Maybe your rent went up, your favorite takeout meal costs a few dollars more, or your electricity bill seems higher without any major change in usage. Even monthly expenses like insurance, streaming services, and school supplies have become noticeably more expensive.

These aren’t isolated price increases—they’re all connected by one powerful economic force: inflation.

Inflation touches nearly every part of daily life. It quietly raises the cost of food, transportation, housing, healthcare, entertainment, and countless other necessities. Because these increases usually happen little by little, many people don’t realize how much extra they’re spending until their monthly budget starts feeling stretched.

The real challenge is that inflation doesn’t only make things more expensive. It also reduces the value of the money you already earn and save. Even if your paycheck stays the same—or increases slightly—you may still find it harder to cover everyday expenses because prices are rising faster than your income.

Learning how inflation affects your everyday finances is one of the most important money skills you can develop. Once you understand why prices increase and where hidden costs appear, you can make smarter budgeting decisions, protect your savings, and reduce the financial pressure caused by rising living costs.

This guide explains inflation in simple, everyday language. You’ll discover what inflation really means, why it happens, how it affects your purchasing power, and the first six hidden costs that may already be draining your money in 2026.

What Is Inflation?

Inflation is the gradual increase in the average price of goods and services over time. As prices rise, every dollar in your wallet buys a little less than it did before. In simple terms, inflation reduces the purchasing power of your money.

Think about buying lunch at your favorite restaurant. Last year, a burger and fries may have cost $8. This year, the exact same meal costs $9, even though the portion size and ingredients haven’t changed. You’re spending more money without receiving additional value. That extra dollar reflects inflation.

Inflation affects much more than restaurant meals. It influences the prices of groceries, gasoline, rent, healthcare, clothing, insurance, travel, and household products. When many prices rise across the economy at the same time, families often notice that their monthly budget doesn’t stretch as far as it once did.

Normal Inflation vs. High Inflation

Not all inflation is harmful. In fact, a moderate level of inflation is considered a normal part of a healthy economy. Businesses regularly face higher wages, transportation costs, raw material expenses, and operating costs. Slight price increases help companies continue operating while supporting economic growth.

Problems begin when inflation rises much faster than incomes. During periods of high inflation, the cost of living can increase quickly, making it difficult for households to keep up with everyday expenses.

| Normal Inflation | High Inflation |

|---|---|

| Prices rise gradually over time. | Prices increase rapidly in a short period. |

| Household budgets remain easier to manage. | Families struggle to cover basic expenses. |

| Businesses adjust prices slowly. | Frequent price increases create uncertainty. |

| Savings lose value at a slower pace. | Purchasing power declines much faster. |

Understanding this difference helps explain why some years feel financially comfortable while others put more pressure on household budgets.

Why Inflation Happens

Inflation doesn’t happen because of a single event. Instead, it’s usually the result of several economic factors working together. Some causes begin within a country, while others are linked to global events that affect businesses and consumers around the world.

Here are some of the most common reasons prices rise.

Increased Consumer Demand

When people have more money to spend, they often buy more products and services. If businesses cannot produce enough goods to meet that demand, prices typically increase.

Imagine a popular gaming console during the holiday season. If thousands of shoppers want one but stores receive limited inventory, retailers may raise prices because demand exceeds supply.

Supply Chain Problems

Every product goes through a long journey before reaching store shelves. Raw materials must be collected, products manufactured, packaged, shipped, stored, and delivered.

If any step in this process experiences delays, shortages, or higher transportation costs, businesses usually pay more to bring products to customers. Those extra expenses are often reflected in higher retail prices.

Rising Energy Costs

Energy plays a role in almost every industry. Trucks delivering groceries need fuel. Factories require electricity. Farmers rely on diesel-powered equipment. Airlines, shipping companies, and manufacturers all depend on energy to operate efficiently.

When oil, natural gas, or electricity prices increase, companies often experience higher operating costs. To maintain profitability, many businesses pass part of those expenses on to consumers.

Labor Shortages and Higher Wages

Businesses need employees to produce goods and provide services. When qualified workers become harder to find, employers often increase wages to attract and retain staff.

Higher wages benefit workers, but they can also increase business expenses. Companies may respond by raising the prices of products or services.

Government Spending

Government spending can stimulate economic activity by increasing demand for goods, services, and infrastructure projects. If demand grows faster than the economy’s ability to produce enough products, inflationary pressure may develop.

Government spending alone doesn’t always cause inflation, but it can contribute when combined with strong consumer demand and limited supply.

Interest Rates

Central banks use interest rates to help manage inflation.

Lower interest rates make borrowing cheaper, encouraging consumers and businesses to spend more. Higher interest rates make loans more expensive, reducing borrowing and slowing overall demand.

Although changes in interest rates don’t affect prices immediately, they often influence inflation over time.

Global Events

Modern economies are connected through international trade. A major event in one region can affect prices around the world.

Examples include:

- Shipping disruptions

- International conflicts

- Trade restrictions

- Global health emergencies

- Changes in oil production

These events can reduce the supply of important products, making them more expensive.

Natural Disasters

Floods, hurricanes, droughts, and wildfires can damage crops, factories, roads, and transportation networks.

When fewer goods are available because production has been disrupted, prices often increase until supply improves.

Currency Value

Countries import many of the products they use every day. If a country’s currency weakens compared with others, imported goods become more expensive.

Retailers usually adjust prices to cover these higher purchasing costs, adding another source of inflation.

Although these factors may seem unrelated, they often combine to influence the prices consumers see every day.

How Inflation Reduces Purchasing Power

One of the biggest effects of inflation is its impact on purchasing power.

Purchasing power refers to the amount of goods and services your money can buy. As prices increase, each dollar purchases less than it did before.

Imagine you earn $4,500 per month, and your salary stays exactly the same for two years. During that time, rent increases by 8%, groceries rise by 10%, gasoline costs more, insurance premiums increase, and utility bills become higher.

Your income hasn’t changed, but your expenses have. Even though your paycheck looks identical, it no longer covers as much as it once did.

This is why inflation can feel like receiving an invisible pay cut.

A Simple Example

Suppose you saved $100 for a shopping trip.

Last year, you could buy:

- A week’s worth of groceries

- Household cleaning supplies

- Personal care products

Today, that same $100 might only cover groceries, leaving little room for the other items.

The money hasn’t disappeared—its buying power has simply declined.

Why Purchasing Power Matters

Many people celebrate receiving a salary increase, but what matters most is whether that raise keeps pace with inflation.

For example:

- Annual salary increase: 3%

- Annual inflation rate: 6%

Although your paycheck is larger, your living expenses are growing even faster. Your real buying power has actually decreased.

This explains why many households feel financially stressed despite earning more than they did a few years ago.

Common Signs Your Purchasing Power Is Declining

You may already be experiencing reduced purchasing power if you find yourself:

- Spending more during routine grocery trips.

- Filling your gas tank less often.

- Delaying vacations or weekend trips.

- Cutting back on restaurant meals.

- Reducing monthly savings.

- Depending more on credit cards.

- Comparing prices more carefully than before.

- Waiting for sales before making purchases.

These changes often happen gradually, making inflation difficult to notice until your monthly budget becomes noticeably tighter.

Recognizing these warning signs early allows you to adjust your spending habits before rising costs create long-term financial stress.

read also: The Psychology of Spending: Why We Buy Things We Don’t Need in 2026

17 Hidden Ways Inflation Affects Everyday Finances

Inflation doesn’t always appear as a dramatic jump in prices. More often, it shows up through small increases that quietly affect your budget month after month. The following hidden costs reveal how inflation influences everyday spending in ways many people overlook.

1. Grocery Bills Quietly Increase

For most households, groceries are one of the first places where inflation becomes noticeable. Prices for everyday essentials such as bread, milk, eggs, fresh vegetables, meat, and cooking oil rarely increase all at once. Instead, they rise gradually over time, making each shopping trip slightly more expensive than the last.

Because these increases happen little by little, many shoppers don’t realize how much more they’re spending until they compare receipts from previous months. A weekly grocery bill that’s only $15 higher may not seem significant, but over an entire year, that adds up to nearly $800 in additional spending without buying more food.

Food manufacturers also face higher transportation, packaging, and labor costs, which contribute to rising shelf prices. Seasonal weather events and supply shortages can make certain foods even more expensive.

Money-saving tip: Plan meals before shopping, create a grocery list, compare unit prices, and choose seasonal produce whenever possible. These simple habits can reduce unnecessary spending while keeping your household budget under control.

2. Shrinkflation Means You’re Paying More for Less

Not every price increase appears on the price tag. Sometimes manufacturers reduce the size of a product while keeping the price exactly the same. This practice is known as shrinkflation.

You may notice cereal boxes containing fewer ounces, snack bags with less product, smaller ice cream containers, or rolls of paper towels with fewer sheets. At first glance, the packaging looks almost identical, making these changes easy to overlook.

Although the shelf price hasn’t changed much, the cost per ounce or per serving has increased. Over time, buying smaller quantities at the same price quietly raises your overall spending.

Shrinkflation has become increasingly common because businesses often believe consumers are less likely to notice smaller packages than higher prices.

Money-saving tip: Always compare the unit price displayed on store shelves instead of relying only on the package price. This helps you identify the best value regardless of package size.

3. Higher Electricity and Utility Bills

Electricity, water, natural gas, internet service, and waste collection are essential household expenses that often become more expensive during periods of inflation.

Energy providers face higher fuel prices, maintenance costs, infrastructure investments, and labor expenses. These additional costs eventually influence the rates consumers pay each month.

Even if your household uses the same amount of electricity, your bill may still increase because the price charged per unit of energy has risen. Seasonal weather can add further pressure, especially during extremely hot summers or cold winters when heating and cooling systems work harder.

Many families underestimate how much utilities affect their annual budget because monthly increases are often relatively small. However, over several years, these higher bills can significantly reduce the amount available for savings or other financial goals.

Money-saving tip: Replace old light bulbs with LED lighting, unplug electronics when not in use, improve home insulation, and adjust your thermostat to reduce unnecessary energy consumption.

4. Rising Gasoline and Transportation Costs

Transportation costs extend far beyond filling your vehicle’s fuel tank. When gasoline and diesel prices rise, the effects spread throughout the entire economy.

Delivery companies pay more to transport products, airlines face higher operating expenses, and public transportation systems may increase fares. Businesses often recover these additional costs by charging customers more for goods and services.

Families with long commutes or multiple vehicles usually feel these increases first. Higher fuel prices also contribute to more expensive groceries, online deliveries, construction materials, and household products because transportation is part of nearly every supply chain.

Vehicle ownership becomes more expensive as repair services, replacement parts, tires, and routine maintenance also increase in price.

Money-saving tip: Combine errands into one trip, maintain proper tire pressure, follow your vehicle’s maintenance schedule, and compare local fuel prices before filling your tank.

5. Rent Continues to Rise

Housing represents one of the largest expenses for most families, making rent increases especially difficult to absorb.

Landlords often face rising property taxes, insurance premiums, maintenance costs, repair expenses, and utility bills. To offset these higher operating costs, many increase rent when leases are renewed.

Even a monthly increase of $100 can add $1,200 to your yearly housing expenses without providing additional living space or improved amenities. As housing consumes a larger portion of household income, families may need to reduce spending in other areas such as entertainment, travel, or savings.

Growing housing costs can also make it more difficult to build an emergency fund or prepare for future financial goals.

Money-saving tip: Research local rental rates before renewing your lease. Negotiating early or signing a longer lease may help secure a lower monthly payment.

6. Buying a Home Becomes More Expensive

Inflation affects homebuyers differently than renters, but the financial impact can be just as significant.

When inflation remains high, interest rates often increase. Higher mortgage rates raise monthly loan payments, even if home prices stay relatively stable. As a result, many buyers qualify for smaller mortgages or delay purchasing a home altogether.

Existing homeowners may also experience higher costs through increased property taxes, homeowners insurance, maintenance expenses, and repair bills. Materials such as lumber, roofing supplies, plumbing fixtures, and appliances often become more expensive during inflationary periods.

Owning a home involves far more than making a mortgage payment, and inflation increases many of these ongoing expenses simultaneously.

Money-saving tip: Before buying a home, calculate the total cost of ownership—including taxes, insurance, maintenance, repairs, and emergency savings—to ensure your budget can handle future price increases.

7. Insurance Premiums Become More Expensive

Insurance costs often rise quietly over time. Auto, health, home, and life insurance companies adjust premiums to cover higher repair costs, medical expenses, and claim payouts. Even if you’ve never filed a claim, your monthly premium may still increase.

Tip: Compare quotes every year and ask about available discounts before renewing your policy.

8. Restaurant Meals Cost More

Dining out becomes more expensive as restaurants face higher food, labor, rent, and utility costs. Smaller portions, added service fees, and higher menu prices all increase your total bill.

Tip: Cook more meals at home and reserve restaurant visits for special occasions. How Inflation Affects Your Everyday Finances

9. Streaming Subscriptions Get Pricier

Small monthly subscription increases can quietly drain your budget. Streaming services, music apps, cloud storage, and software memberships often raise prices over time.

Tip: Review subscriptions every few months and cancel services you rarely use.

10. Medical Expenses Increase

Healthcare costs often rise with inflation. Doctor visits, prescription medications, dental care, and health insurance premiums may all become more expensive, making routine care harder to afford.

Tip: Build a healthcare emergency fund and use preventive care whenever possible.

11. School and Childcare Costs Rise

Parents often face higher expenses for tuition, daycare, school supplies, uniforms, books, and extracurricular activities. These increases can significantly impact a family’s monthly budget.

Tip: Shop during sales, reuse supplies when possible, and create a yearly education budget.

12. Travel Costs More

Flights, hotels, rental cars, and vacation activities usually become more expensive during inflation. Even road trips cost more because of higher fuel prices.

Tip: Book early, travel during off-peak seasons, and compare prices before making reservations.

13. Credit Card Debt Becomes Harder to Manage

Higher interest rates often mean higher credit card charges. Carrying a balance becomes more expensive, making it harder to pay off debt.

Tip: Pay more than the minimum payment and focus on eliminating high-interest debt first.

14. Savings Lose Purchasing Power

Money sitting in a regular savings account may lose value if inflation grows faster than the interest you earn. Your balance stays the same, but it buys less over time.

Tip: Consider savings options that offer competitive interest rates and review your savings strategy regularly.

15. Retirement Planning Gets More Difficult

Inflation increases the amount of money you’ll need during retirement. Healthcare, housing, and daily living costs may all be much higher in the future.

Tip: Increase retirement contributions whenever your income grows and review your investment plan regularly.

16. Home Maintenance Costs More

Home repairs become more expensive as labor and building material prices rise. Small repairs that once cost a few hundred dollars may cost much more in 2026.

Tip: Perform regular maintenance to prevent expensive repairs later. How Inflation Affects Your Everyday Finances

17. Small Daily Purchases Add Up Faster

A coffee on the way to work, snacks, convenience store stops, or online impulse purchases may seem inexpensive individually. However, inflation makes these everyday purchases cost more, adding hundreds of dollars to your yearly spending.

Tip: Track small daily expenses for one month. You may discover easy opportunities to save without making major lifestyle changes.

Real-Life Example: A Family Budget in 2024 vs. 2026

To understand how inflation affects your everyday finances, let’s look at a fictional family of four. Their lifestyle hasn’t changed much between 2024 and 2026, but rising prices have increased many of their monthly expenses.

Monthly Household Budget Comparison

| Expense | 2024 | 2026 |

|---|---|---|

| Rent | $1,500 | $1,700 |

| Groceries | $650 | $780 |

| Fuel | $220 | $290 |

| Utilities | $180 | $230 |

| Insurance | $300 | $360 |

| Entertainment | $180 | $220 |

| Savings | $700 | $450 |

What Changed?

The family still lives in the same home, drives the same vehicles, and buys similar groceries. However, inflation has increased the cost of housing, food, transportation, utilities, and insurance. As a result, they now save $250 less each month than they did in 2024.

This example shows that inflation doesn’t always require major lifestyle changes to affect your finances. Even small increases across several categories can significantly reduce your ability to save and invest.

Inflation vs. Wage Growth

Many people expect a yearly raise to keep their finances on track. However, a higher salary doesn’t always mean you’re financially better off.

The key factor is whether your income grows faster than inflation.

For example, imagine you receive a 3% salary increase, but inflation rises by 6% during the same year. Although your paycheck is larger, your everyday expenses are increasing even faster. This means your real income, or buying power, has actually declined.

Example

- Annual salary: $60,000

- Salary increase: 3%

- New salary: $61,800

- Inflation: 6%

While you earn an additional $1,800, the cost of groceries, housing, transportation, insurance, and other essentials has increased even more. As a result, your money doesn’t stretch as far as it did before.

Why This Matters

If wage growth consistently lags behind inflation, households may need to:

- Reduce discretionary spending.

- Delay major purchases.

- Save less each month.

- Use credit cards more often.

- Rework their household budget.