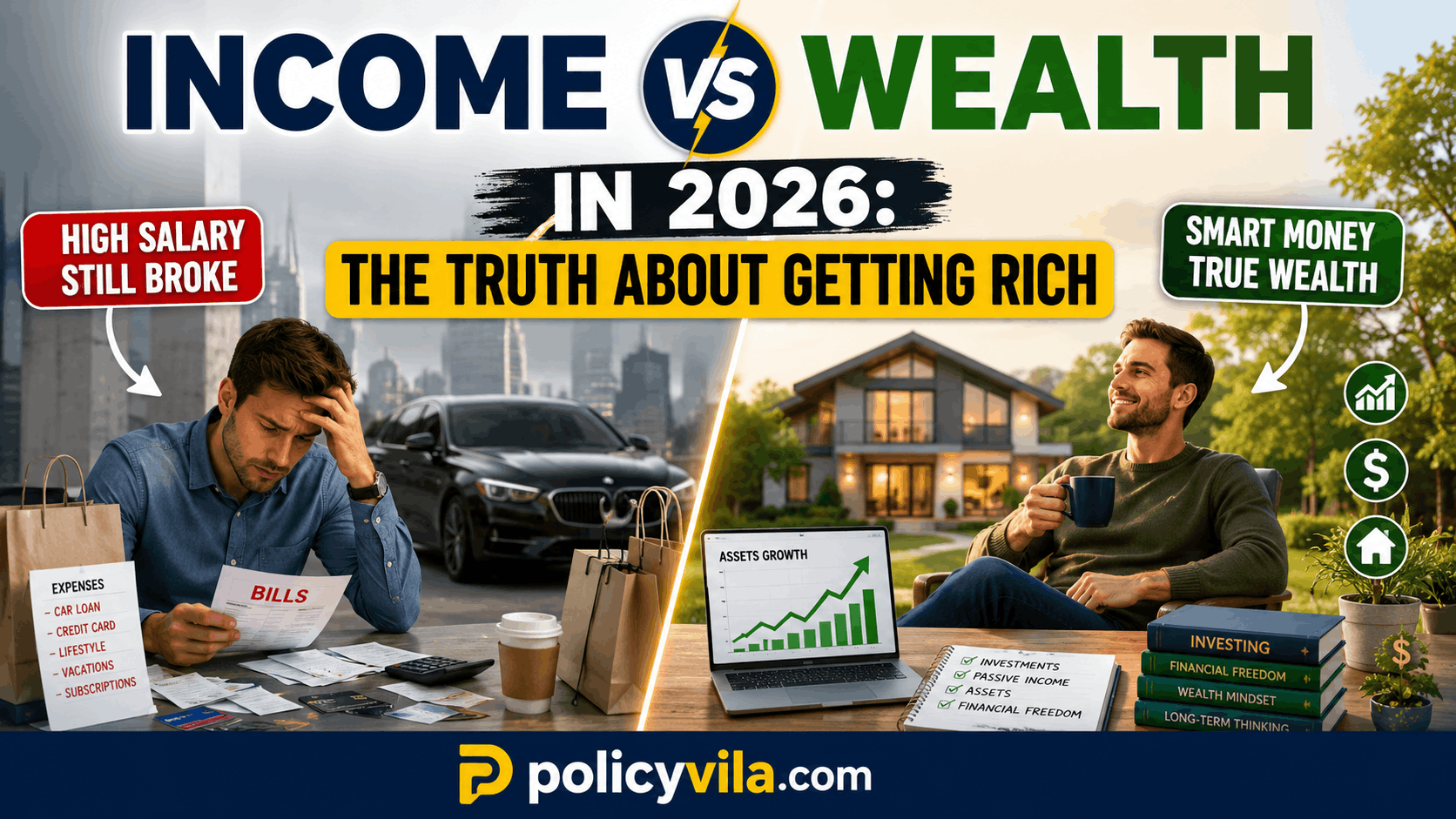

Income vs Wealth: Have you ever wondered why some people earning six-figure salaries still worry about money, while others with average incomes seem calm, confident, and financially secure?

Imagine two neighbors.

Neighbor A earns $250,000 a year. They drive a luxury SUV, own a large house with a hefty mortgage, take expensive vacations every year, and often upgrade to the newest gadgets. Their social media looks impressive, but behind the scenes they’re juggling credit card balances, car payments, and constant financial stress.

Neighbor B earns $85,000 a year. Their home is comfortable but affordable. They drive a reliable car that’s fully paid off. Every month, they consistently save, invest, and avoid unnecessary debt. They don’t live extravagantly, yet they sleep peacefully knowing their financial future is getting stronger every year.

So, who is actually richer?

Most people would immediately choose Neighbor A because of the higher salary and luxurious lifestyle.

But the real answer is often Neighbor B.

Why?

Because income creates cash flow, while wealth creates freedom.

This is one of the most misunderstood concepts in personal finance. Many people spend years chasing higher salaries, believing that earning more automatically leads to financial success. Yet countless high earners remain trapped in a cycle of spending, debt, and financial pressure.

Meanwhile, millions of ordinary earners quietly build impressive net worth by making smart financial decisions over many years.

Understanding Income vs Wealth can completely change how you think about money. It’s not just about earning more. It’s about keeping more, growing more, and allowing your money to work for you instead of constantly working for your money.

In this guide, you’ll learn:

- Why income and wealth are completely different

- Why earning more doesn’t automatically make you rich

- How financially successful people think differently about money

- Why lifestyle inflation quietly destroys long-term wealth

- Everyday habits that build lasting financial independence

- A practical roadmap for turning today’s income into tomorrow’s financial freedom

Let’s begin by exploring one of the biggest financial myths people believe.

The Biggest Financial Myth Most People Believe

Ask someone to describe a wealthy person, and you’ll often hear answers like:

- “They earn a huge salary.”

- “They have a fancy house.”

- “They drive expensive cars.”

- “They wear designer clothes.”

These answers reveal one of society’s biggest financial misconceptions.

High Salary Doesn’t Equal Financial Success

A large paycheck can certainly make life more comfortable. It provides more opportunities and flexibility.

However, income alone says very little about someone’s actual financial position.

Consider these two individuals.

| Person | Annual Income | Annual Spending | Savings | Net Worth Trend |

|---|---|---|---|---|

| Person A | $250,000 | $245,000 | $5,000 | Slow growth |

| Person B | $85,000 | $55,000 | $30,000 | Strong growth |

Person A earns nearly three times more but saves very little.

Person B earns much less but consistently builds assets and increases net worth every year.

Financial success isn’t determined by how much money enters your bank account.

It’s determined by how much stays there—and what that money becomes over time.

Why Society Measures Income Instead of Wealth

Income is visible.

We often know someone’s job title, business, or profession. We can estimate their salary based on what they do.

Wealth, on the other hand, is mostly invisible.

You can’t easily see:

- Investment accounts

- Emergency savings

- Retirement funds

- Business ownership

- Rental income

- Debt balances

- Net worth

Someone living modestly may quietly have significant financial security, while another person displaying luxury could be carrying substantial debt.

That’s why appearances can be misleading.

Social Media Makes the Problem Worse

Today’s digital world encourages comparison.

People frequently post:

- Luxury vacations

- New cars

- Designer shopping

- Expensive restaurants

- Beautiful homes

Very few people post:

- Their monthly savings

- Investment contributions

- Debt payoff progress

- Emergency fund growth

- Increasing net worth

This creates a distorted picture of financial success.

Many people begin spending money simply to match what they see online, even when it doesn’t improve their financial future.

Keeping Up With Everyone Else

Psychologists call this social comparison. Income vs Wealth

When friends upgrade their homes, buy new vehicles, or wear luxury brands, it’s natural to feel pressure to do the same.

The problem is that financial decisions driven by comparison rarely create lasting happiness.

Instead, they often create:

- Higher monthly expenses

- Larger debt payments

- Increased financial anxiety

- Reduced savings

- Delayed financial independence

True wealth rarely needs public approval.

In many cases, the wealthiest people are the least interested in showing off.

Income vs Wealth: What’s the Real Difference?

Understanding the difference between income and wealth is one of the most valuable lessons in personal finance.

Although people often use these terms interchangeably, they describe two completely different financial concepts.

What Is Income?

Income is money you receive.

It usually comes from:

- Salary

- Wages

- Freelance work

- Business profits

- Bonuses

- Side jobs

Income provides cash flow.

Without income, paying everyday expenses becomes difficult.

However, income alone doesn’t guarantee long-term financial security.

If every dollar earned is immediately spent, wealth never has the opportunity to grow.

What Is Wealth?

Wealth is everything you own after subtracting everything you owe.

In simple terms:

Wealth = Assets − Liabilities

Wealth includes things like:

- Savings

- Investments

- Home equity

- Business ownership

- Retirement accounts

- Valuable appreciating assets

Unlike income, wealth keeps working even when you’re not actively earning.

That’s why wealth provides options and freedom.

Understanding Cash Flow

Cash flow refers to the movement of money in and out of your life.

Positive cash flow means more money comes in than goes out.

Negative cash flow means expenses consistently exceed income.

Healthy cash flow creates opportunities to save, invest, and build assets.

Poor cash flow often leads to debt and financial stress.

What Is Net Worth?

Net worth measures your overall financial health.

Formula:

Assets – Liabilities = Net Worth

For example:

Assets:

- Savings: $40,000

- Investments: $120,000

- Home Equity: $180,000

Total Assets = $340,000

Liabilities:

- Mortgage Balance: $150,000

- Car Loan: $15,000

Total Liabilities = $165,000

Net Worth = $175,000

Notice that income isn’t part of this calculation.

Someone earning less may still have a much higher net worth.

Assets vs Liabilities

Understanding this distinction changes how people make financial decisions.

Assets generally:

- Increase in value over time

- Produce income

- Strengthen financial security

Liabilities generally:

- Require ongoing payments

- Lose value over time

- Reduce available cash flow

We’ll explore this topic in greater detail later in the guide.

Financial Freedom Starts With Wealth

Income pays your bills.

Wealth pays your future.

As wealth grows, it begins producing its own income through appreciating assets and other cash-generating resources.

Eventually, people may reach a point where their assets help cover living expenses, reducing their dependence on active work.

That’s one of the core ideas behind financial independence.

Income vs Wealth Comparison

| Income | Wealth |

|---|---|

| Money you earn | Money you own |

| Pays monthly bills | Creates long-term security |

| Depends on working | Can grow independently |

| Temporary | Long-lasting |

| Creates cash flow | Creates financial freedom |

| Can disappear if work stops | Continues growing with smart management |

| Measured yearly | Measured through net worth |

The key takeaway is simple.

A high income gives you the opportunity to build wealth.

Only consistent financial habits actually make it happen.

Why High Earners Often Stay Broke

Many people assume that earning more automatically solves money problems.

In reality, higher income often creates new spending habits instead of greater financial security.

This is why some professionals earning hundreds of thousands of dollars still live paycheck to paycheck.

Lifestyle Inflation Happens Quietly

The moment income increases, spending often increases too.

A promotion arrives.

Soon afterward:

- A larger house feels necessary.

- A luxury vehicle replaces the old one.

- Dining out becomes routine.

- Vacations become more expensive.

- Monthly subscriptions multiply.

Instead of building wealth, every raise gets absorbed by a more expensive lifestyle.

This pattern is called lifestyle inflation, and it’s one of the biggest obstacles to long-term wealth.

Bigger Homes Mean Bigger Bills

A larger home isn’t just a higher mortgage.

It often brings: Income vs Wealth

- Higher utility bills

- More furniture purchases

- Increased maintenance costs

- Property taxes

- Landscaping expenses

- Home improvement projects

The monthly cost grows far beyond the purchase price.

Luxury Vehicles Can Drain Cash Flow

Expensive vehicles often come with:

- Higher loan payments

- Increased insurance costs

- Costlier repairs

- Faster depreciation

While they may provide enjoyment, they can also reduce the money available for building assets.

Status Spending Never Ends

Many purchases aren’t made because they’re needed.

They’re made to impress others.

Status spending often includes:

- Premium gadgets

- Luxury watches

- Designer clothing

- High-end furniture

- Frequent upgrades

The challenge is that there’s always another upgrade waiting.

The Quiet Habits of People Who Actually Build Wealth

If you ask ten financially successful people how they built wealth, you’ll probably hear ten different stories. One may have started a business, another may have climbed the corporate ladder, and another may have built wealth through steady investing over decades.

Although their paths are different, their daily habits are surprisingly similar.

People who build lasting wealth rarely depend on luck or sudden windfalls. Instead, they consistently make financial decisions that strengthen their future, even when those decisions don’t provide immediate rewards.

Let’s explore the habits that quietly separate true wealth builders from people who simply earn high incomes.

They Live Below Their Means

Living below your means doesn’t require living a deprived life. It simply means spending less than you earn so that part of your income can build your future instead of disappearing each month.

Many people increase their spending every time their salary increases. Wealth builders often do the opposite. They enjoy some lifestyle improvements but direct a significant portion of every raise toward savings, investments, or building assets.

For example, imagine two coworkers who each receive a $12,000 annual raise.

The first immediately upgrades to a larger home, leases a luxury vehicle, and increases vacation spending. Within a few months, nearly every extra dollar has been committed to new monthly expenses.

The second keeps their current lifestyle largely unchanged. They invest part of the raise, increase emergency savings, and pay down existing debt. Five or ten years later, the financial gap between these two people can become enormous, even though they earned the same salary.

Living below your means creates flexibility. It gives you options during emergencies, career changes, and economic downturns while allowing your wealth to grow steadily.

They Invest Consistently Instead of Waiting for the Perfect Time

One of the biggest mistakes people make is believing they need perfect timing before they begin investing.

Successful wealth builders understand that consistency usually matters far more than perfection.

Rather than trying to predict markets or waiting until they “have more money,” they invest regularly over many years. Small contributions made consistently often outperform irregular large investments because they benefit from long-term compounding.

Think of investing like planting a tree.

The best time to plant it was years ago. The second-best time is today.

Every month that money remains invested gives it another opportunity to grow. Waiting for the “perfect moment” often means losing valuable time that can never be recovered.

They Buy Assets Before Buying Luxuries

One of the defining characteristics of financially successful people is that they prioritize ownership over appearance.

Instead of immediately spending additional income on luxury items, they first look for opportunities to purchase assets that strengthen their financial future.

Assets may include:

- Investment accounts

- Business ownership

- Real estate that builds equity

- Retirement savings

- Valuable skills that increase earning potential

- Intellectual property or income-producing projects

This doesn’t mean wealthy people never enjoy luxury purchases.

The difference is timing.

They often allow their assets to grow first and let those assets help fund future lifestyle choices.

People who focus only on consumption often work continuously to support their spending. Those who focus on assets gradually create financial independence.

They Avoid Unnecessary Debt

Debt itself isn’t automatically good or bad.

The real question is whether the debt helps improve your long-term financial position or simply finances short-term consumption.

Many high earners fall into the trap of financing expensive lifestyles. Monthly payments become normal, and before long, much of their income is committed before each paycheck even arrives.

Examples include financing luxury vacations, carrying high credit card balances, purchasing expensive electronics on installment plans, or upgrading vehicles long before necessary.

Every unnecessary monthly payment reduces future cash flow.

That means less money is available for investing, saving, or purchasing assets.

Financially successful people understand that reducing unnecessary debt increases financial freedom.

They Think in Decades, Not Months

Many financial decisions look very different when viewed over twenty years instead of twenty days.

People focused only on short-term satisfaction often ask questions like:

- Can I afford this monthly payment?

- Will this make me happy today?

- Can I buy it right now?

Wealth builders ask different questions:

- Will this decision improve my future?

- How will this affect my net worth ten years from now?

- Is today’s purchase worth delaying tomorrow’s freedom?

Long-term thinking changes everyday behavior.

It encourages patience, smarter spending, and better financial planning.

They Practice Delayed Gratification

Delayed gratification is one of the strongest predictors of long-term financial success.

It means choosing a larger future reward instead of a smaller immediate reward.

For example, after receiving a work bonus, one person may immediately spend it on luxury shopping or expensive entertainment.

Another person may use the same bonus to increase investments, build an emergency fund, reduce debt, or purchase an appreciating asset.

Neither choice is necessarily wrong.

However, repeated over many years, delayed gratification allows wealth to compound while impulsive spending often leaves little to show for higher income.

The ability to wait is one of the greatest financial advantages anyone can develop.

They Continuously Improve Their Financial Knowledge

Building wealth requires more than earning money.

It also requires making informed financial decisions.

Financially successful people continue learning throughout their lives.

They regularly improve their understanding of topics such as:

- Personal finance

- Financial planning

- Tax basics

- Investing principles

- Business management

- Behavioral finance

- Risk management

This doesn’t require becoming a financial expert.

Small improvements in financial knowledge often lead to better decisions, fewer costly mistakes, and greater confidence over time.

They Track Their Financial Progress

Many people know exactly how much income they earn each year.

Far fewer know their current net worth.

Wealth builders regularly review their financial position because what gets measured often improves.

Instead of focusing only on income, they monitor:

- Net worth

- Savings rate

- Debt balances

- Investment growth

- Cash flow

- Emergency fund progress

Tracking these numbers provides motivation and helps identify problems before they become serious.

A growing net worth is often a much stronger sign of financial progress than a growing salary alone.

They Value Financial Freedom More Than Financial Status

Perhaps the biggest difference between high earners and wealth builders is what motivates their financial decisions.

Status-focused spending is designed to impress other people.

Wealth-focused spending is designed to improve future freedom.

Financial freedom means having choices.

It means being able to change careers, start a business, spend more time with family, retire comfortably, or handle unexpected expenses without constant financial stress.

People who build wealth understand that true success isn’t measured by expensive possessions.

It’s measured by the ability to live life on your own terms.

The Common Thread Among Wealth Builders

The habits discussed above are not complicated.

Most people already know they should spend less than they earn, avoid unnecessary debt, save consistently, and think long term.

The challenge is applying these habits consistently over many years.

Building wealth is rarely about making one brilliant financial decision.

It’s about making hundreds of ordinary decisions that steadily improve your financial future.

The Psychology of Wealth

Many people believe building wealth is mainly about earning more money. While income certainly matters, research in behavioral finance shows that human behavior often has a greater impact on long-term financial success than income alone.

Two people can earn the same salary, live in the same city, and have similar expenses, yet end up with completely different financial futures. The difference often comes down to how they think about money and the decisions they make every day.

Understanding the psychology behind financial choices can help you avoid costly mistakes and develop habits that support lasting wealth.

Your Wealth Mindset Shapes Your Financial Future

Your mindset is the collection of beliefs you have about money, success, and financial security.

These beliefs often develop during childhood through family experiences, education, culture, and personal successes or setbacks. Over time, they influence almost every financial decision you make.

Someone with a healthy wealth mindset believes that financial success is built gradually through consistent habits and smart planning. They understand that setbacks are temporary and that improving financial knowledge can lead to better outcomes.

On the other hand, someone with a limiting mindset may believe that wealth is only for the lucky, that investing is too risky, or that they will never have enough money to get ahead. These beliefs can prevent them from taking positive financial action, even when opportunities exist.

Changing your mindset doesn’t instantly increase your bank balance, but it can change the decisions that determine your financial future.

Emotional Spending Can Quietly Destroy Wealth

Not every purchase is based on logic.

Many spending decisions are driven by emotions rather than genuine needs.

People commonly spend money when they feel: Income vs Wealth

- Stressed after a difficult day

- Bored during free time

- Excited about a promotion

- Lonely or discouraged

- Under pressure to fit in

- Motivated by social media trends

This behavior is often called emotional spending.

The purchase may provide temporary happiness, but the feeling usually fades quickly while the financial cost remains.

Before making a significant purchase, ask yourself a simple question:

“Am I buying this because I truly need it, or because I’m trying to change how I feel?”

Taking a few minutes to reflect can prevent many impulse purchases and help you make more intentional financial decisions.

Instant Gratification vs. Delayed Gratification

Modern technology has made it easier than ever to satisfy our desires instantly.

Food can be delivered in minutes.

Shopping takes only a few clicks.

Entertainment is available around the clock.

While convenience has many benefits, it also encourages instant gratification—the desire to receive rewards immediately.

Unfortunately, building wealth rarely happens instantly.

Financial success usually rewards patience, consistency, and long-term thinking rather than quick decisions.

Delayed gratification means willingly postponing today’s pleasure to achieve a greater benefit tomorrow.

For example:

- Saving for a future goal instead of making an impulse purchase.

- Investing part of a bonus instead of spending it immediately.

- Keeping a reliable car for several more years instead of upgrading to a luxury model.

Small decisions like these may not feel exciting today, but over many years they can dramatically improve your financial future.

The Power of Compounding Rewards

One reason delayed gratification works so well is the power of compounding.

Imagine planting a small seed.

For months, it may appear that very little is happening.

Then, over time, the tree grows stronger, larger, and more valuable.

Wealth grows in a similar way.

Consistent saving, investing, and smart financial decisions often produce slow progress in the beginning. As time passes, however, growth can accelerate because your money begins generating additional growth on its own.

This is why patience is one of the greatest advantages any wealth builder can have.

Scarcity Mindset vs. Abundance Mindset

Behavioral finance often discusses two common ways people think about money: the scarcity mindset and the abundance mindset.

The difference isn’t about how much money someone currently has. It’s about how they view opportunities and challenges.

| Scarcity Mindset | Abundance Mindset |

|---|---|

| Believes there is never enough | Believes opportunities can be created |

| Focuses on fear of losing money | Focuses on long-term growth |

| Avoids learning new financial skills | Continuously improves financial knowledge |

| Sees setbacks as permanent | Views setbacks as learning experiences |

| Makes decisions based on fear | Makes decisions based on planning |

An abundance mindset doesn’t ignore financial risks or difficulties.

Instead, it focuses on developing skills, improving habits, and finding practical solutions instead of assuming success is impossible.

Why People Compare Their Finances to Others

Humans naturally compare themselves to people around them.

This tendency becomes even stronger in the age of social media, where people often share only the highlights of their lives.

You might see friends posting about:

- New luxury vehicles

- Expensive vacations

- Designer clothing

- Large homes

- Fine dining experiences

What you rarely see are:

- Credit card balances

- Loan payments

- Financial stress

- Emergency fund shortages

- Retirement savings

Comparing your financial life to someone else’s public image can encourage unnecessary spending and create unrealistic expectations.

Instead of measuring your progress against others, compare yourself to where you were one year ago.

If your savings are growing, your debt is decreasing, and your net worth is improving, you’re moving in the right direction.

Fear and Greed Influence Financial Decisions

Two of the strongest emotions affecting money decisions are fear and greed.

Fear may cause someone to avoid saving or investing because they’re worried about making mistakes.

Greed may encourage someone to chase unrealistic returns or spend beyond their means to appear successful.

Neither emotion leads to sound financial decisions.

Successful wealth builders rely on planning rather than emotions.

They understand that temporary market changes, economic uncertainty, or short-term trends shouldn’t completely change a well-thought-out long-term strategy.

Financial Discipline Is More Valuable Than Financial Intelligence

Many people assume wealthy individuals possess extraordinary financial knowledge.

In reality, discipline often matters more than intelligence.

A person with average financial knowledge who consistently follows good habits is likely to build more wealth than someone with extensive knowledge who never takes action.

Financial discipline includes habits such as:

- Spending less than you earn

- Saving consistently

- Investing regularly

- Avoiding unnecessary debt

- Tracking your net worth

- Reviewing financial goals

- Making thoughtful purchasing decisions

These habits may seem simple, but repeating them year after year produces remarkable long-term results.

Build Habits, Not Just Motivation

Motivation comes and goes.

Some days you’ll feel excited about improving your finances, while other days you may not think about money at all.

That’s why successful wealth builders rely on habits instead of temporary motivation.

For example: Income vs Wealth

- Automatically saving part of every paycheck.

- Reviewing monthly expenses on the same day each month.

- Tracking net worth every quarter.

- Setting long-term financial goals and revisiting them regularly.

When good financial behaviors become habits, they require less willpower and become part of your everyday routine.

The Psychology Behind Lasting Wealth

Building wealth isn’t just about making more money.

It’s about making better decisions with the money you already earn.

People who develop a healthy wealth mindset, control emotional spending, practice delayed gratification, avoid unnecessary comparisons, and build consistent financial habits are often the ones who achieve lasting financial success.

The greatest financial advantage isn’t having the highest income.

It’s having the mindset and discipline to turn today’s income into tomorrow’s wealth.

Assets vs Liabilities: The Wealth-Building Formula

One of the simplest yet most powerful lessons in Income vs Wealth is understanding the difference between assets and liabilities.

Many people believe wealth is built by earning more money. In reality, wealth grows because of what you choose to own and what you choose to owe.

Every financial decision you make either moves you closer to financial freedom or further away from it.

That’s why financially successful people don’t just ask, “Can I afford this?” They ask, “Will this improve my financial future?”

Understanding this difference can completely change the way you spend, save, and build long-term wealth.

What Is an Asset?

An asset is something that adds value to your financial life.

In general, an asset does one or more of the following:

- Increases in value over time

- Produces income

- Improves your net worth

- Strengthens your financial security

Assets are the building blocks of wealth because they have the potential to create future financial benefits.

Common examples of assets include:

- Cash savings

- Retirement accounts

- Diversified investments

- Home equity

- A profitable business

- Rental real estate

- Intellectual property

- Valuable professional skills that increase earning power

Not every asset immediately produces cash flow, but many contribute to long-term financial growth.

For example, improving your education or learning a valuable professional skill may increase your earning potential for years to come. While it isn’t a traditional financial asset, it can significantly improve your ability to build wealth.

What Is a Liability?

A liability is something you owe that requires future payments.

Liabilities reduce your available cash flow because they create ongoing financial obligations.

Examples include: Income vs Wealth

- Credit card balances

- Personal loans

- Auto loans

- Student loans

- Mortgages

- Buy-now-pay-later balances

- Unpaid taxes

- Other outstanding debts

Not every liability is harmful.

For example, borrowing money to purchase a reasonably priced home or to invest in education may support long-term financial goals when managed responsibly.

The key is ensuring that liabilities don’t grow faster than your assets. Income vs Wealth

Assets vs Liabilities: What’s the Difference?

The easiest way to understand the difference is to look at how each affects your financial future.

| Assets | Liabilities |

|---|---|

| Increase your net worth | Reduce your net worth |

| May appreciate over time | Often require regular payments |

| Can produce income | Usually create ongoing expenses |

| Improve financial security | Increase financial obligations |

| Support long-term wealth | Can reduce future cash flow |

| Help build financial independence | Can delay financial freedom |

This simple comparison explains why two people with identical incomes can have completely different financial outcomes.

One consistently buys assets.

The other continually adds liabilities.

After ten or twenty years, the difference can be remarkable.

The Wealth-Building Formula

Building wealth doesn’t require complicated financial strategies.

It often follows a straightforward pattern.

Income

↓

Spend Wisely

↓

Save Consistently

↓

Purchase Assets

↓

Allow Time for Growth

↓

Increase Net Worth

↓

Achieve Financial Freedom

Notice that earning a high salary is only the first step.

Without converting income into assets, wealth rarely grows.

How Everyday Purchases Affect Your Wealth

Every purchase has a financial consequence.

Some purchases improve your future.

Others create long-term expenses.

Consider these everyday examples.

| Purchase | Primarily Builds an Asset or Liability? | Why |

|---|---|---|

| Building an emergency fund | Asset | Improves financial security and flexibility |

| Paying down high-interest debt | Asset-building decision | Frees future cash flow |

| Investing in professional education | Asset | Can increase future earning potential |

| Buying another luxury watch on credit | Liability | Creates debt without increasing financial value |

| Financing an expensive vacation | Liability | Creates payments after the experience ends |

| Maintaining necessary home improvements | Can support an asset | Helps preserve property value |

The goal isn’t to avoid spending altogether.

The goal is to make sure your spending supports your long-term financial goals.

Cash Flow Is the Bridge Between Income and Wealth

Many people focus only on how much they earn.

Successful wealth builders pay equal attention to where that money goes.

Imagine your income as water flowing into a bucket.

If the bucket has several holes, much of that water leaks out before it can be stored.

Those “holes” may include:

- High-interest debt

- Impulse purchases

- Excessive subscriptions

- Frequent luxury upgrades

- Poor financial planning

When unnecessary leaks are reduced, more cash remains available to build assets.

Positive cash flow creates opportunities to save, invest, and steadily increase net worth.

Why Wealth Builders Focus on Ownership

People who build lasting wealth often shift their thinking from consumption to ownership.

Instead of asking, “What can I buy?” they ask, “What can I own that will strengthen my future?”

Ownership creates lasting value.

Whether it’s owning part of a business, building retirement savings, increasing home equity, or developing valuable professional skills, ownership often provides benefits that continue long after the initial investment of time or money.

This mindset encourages decisions that generate long-term financial stability instead of temporary satisfaction. Income vs Wealth

Small Asset Purchases Can Lead to Big Results

Many people believe they need a large amount of money before they can start building wealth.

In reality, wealth often begins with small, consistent actions.

For example:

- Setting aside money each month for future opportunities.

- Paying off one debt at a time.

- Regularly contributing to long-term investments.

- Building an emergency fund before increasing lifestyle spending.

- Investing in education that improves career opportunities.

None of these actions seem dramatic on their own.

However, repeated over many years, they can produce significant improvements in financial security.

Small decisions, consistently repeated, often outperform occasional large financial moves.

Avoid Confusing Expensive With Valuable

One of the biggest financial mistakes is assuming that expensive automatically means valuable.

A costly purchase isn’t necessarily an asset.

Likewise, an affordable purchase isn’t automatically a liability.

For example:

- A luxury car may cost a great deal but lose value over time while creating ongoing expenses.

- Learning a new professional skill may cost far less yet significantly increase your earning potential for years.

Before making a major purchase, consider asking yourself these questions:

- Will this increase my net worth?

- Will it improve my future cash flow?

- Will it reduce financial stress?

- Will it still provide value five years from now?

These questions help shift your focus from immediate gratification to long-term financial success. Income vs Wealth

Wealth Is Built by Owning More Than You Owe

At its core, wealth building is surprisingly simple.

As your assets grow and your liabilities shrink, your net worth increases.

This doesn’t happen overnight.

It happens through hundreds of thoughtful financial decisions made over many years.

You don’t need to earn the highest salary to build wealth.

You need to consistently direct part of your income toward assets that strengthen your financial future while carefully managing the liabilities that reduce it.

When your assets begin growing faster than your debts, you’re no longer just earning money—you are steadily building lasting wealth.

Lifestyle Inflation: The Silent Wealth Killer

Getting a raise feels exciting.

A promotion, a successful business year, or a better-paying job often brings a sense of achievement. Naturally, many people want to reward themselves for their hard work.

There’s nothing wrong with enjoying the benefits of earning more.

The problem begins when every increase in income is matched by an equal or even larger increase in spending.

This is known as lifestyle inflation, and it’s one of the biggest reasons many high-income earners struggle to build lasting wealth.

Lifestyle inflation doesn’t happen overnight. It creeps into your life one upgrade at a time until your larger paycheck no longer feels larger at all.

What Is Lifestyle Inflation?

Lifestyle inflation happens when your standard of living rises every time your income increases.

Instead of using extra income to build wealth, you gradually increase your monthly expenses.

It often starts with small changes.

You receive a raise, so you decide to:

- Move into a larger home.

- Lease a more expensive vehicle.

- Eat at restaurants more often.

- Buy premium brands instead of everyday products.

- Upgrade your phone every year.

- Add more entertainment subscriptions.

- Take more luxurious vacations.

None of these decisions may seem significant on their own.

However, together they create a lifestyle that becomes increasingly expensive to maintain.

Soon, your higher salary simply supports a higher cost of living instead of increasing your financial security.

Why Lifestyle Inflation Feels Normal

Lifestyle inflation often doesn’t feel like overspending because each upgrade seems reasonable at the time.

You might tell yourself: Income vs Wealth

- “I’ve worked hard for this.”

- “I deserve something nicer.”

- “Everyone at my job drives a newer car.”

- “I can easily afford the monthly payment.”

These thoughts are understandable.

The challenge is that financial decisions based on emotions or social expectations often lead to long-term financial commitments.

A single monthly payment may seem manageable.

Several new monthly payments can quietly consume most of your income.

The Lifestyle Inflation Cycle

Many people unknowingly repeat the same financial pattern throughout their careers.

It looks something like this:

Higher Income

↓

Lifestyle Upgrade

↓

Higher Monthly Expenses

↓

Less Money Available to Save

↓

Slower Wealth Growth

↓

Need for Even More Income

↓

Another Lifestyle Upgrade

The cycle continues with every promotion or salary increase.

Eventually, a person earning $250,000 per year may feel almost as financially stressed as someone earning much less because their expenses have risen just as quickly. Income vs Wealth

The Hidden Costs of Lifestyle Upgrades

When people think about major purchases, they often focus only on the purchase price.

The ongoing costs receive much less attention.

For example, buying a larger home doesn’t simply increase your mortgage.

It may also increase:

- Property taxes

- Home insurance

- Utility bills

- Furniture purchases

- Maintenance costs

- Landscaping expenses

- Repair costs

Similarly, upgrading to a luxury vehicle doesn’t only mean a higher monthly payment.

It often comes with:

- Higher insurance premiums

- More expensive repairs

- Increased registration fees

- Faster depreciation

- Higher fuel costs

The true cost of a lifestyle upgrade is usually much greater than it first appears.

Lifestyle Inflation and Social Comparison

One of the biggest drivers of lifestyle inflation is comparison.

People naturally compare themselves with coworkers, neighbors, friends, and even strangers online.

Social media makes this even more challenging.

Every day, you may see people sharing: Income vs Wealth

- Luxury vacations

- Designer clothing

- Expensive restaurants

- New vehicles

- Beautiful homes

- High-end electronics

What you rarely see are:

- Loan balances

- Credit card debt

- Financial stress

- Missed savings goals

- Budget struggles

Comparing your everyday life to someone else’s highlight reel can lead to spending decisions that don’t actually improve your happiness or financial future.

Why More Spending Doesn’t Always Mean More Happiness

Many people believe that upgrading their lifestyle will make them permanently happier.

In reality, happiness often follows a different pattern.

Imagine buying your dream car.

During the first few weeks, every drive feels exciting.

After several months, however, the excitement begins to fade.

The car becomes your new normal.

Soon, another upgrade seems necessary to recreate that feeling.

Psychologists call this hedonic adaptation.

People naturally become accustomed to improvements in their lifestyle, which means today’s luxury often becomes tomorrow’s expectation.

As a result, constantly increasing spending rarely leads to lasting satisfaction. Income vs Wealth

Financial security, on the other hand, often provides peace of mind that lasts much longer than the excitement of a new purchase.

How Lifestyle Inflation Slows Wealth Building

Every additional dollar spent today is one less dollar available for tomorrow’s wealth.

For example, imagine someone receives a $15,000 annual raise.

They have two choices.

Option A: Lifestyle Upgrade

- Move into a more expensive apartment

- Upgrade to a luxury vehicle

- Increase entertainment spending

- Take more expensive vacations

Within a year, nearly the entire raise is gone.

Their lifestyle improves, but their financial position changes very little.

Option B: Wealth Building

- Continue living comfortably within their current budget

- Increase savings

- Invest consistently

- Reduce existing debt

- Build additional assets

Their lifestyle changes only slightly, but their net worth grows year after year.

The difference isn’t income.

It’s how the extra income is used.

Enjoy Success Without Letting Expenses Take Control

Avoiding lifestyle inflation doesn’t mean you should never enjoy your achievements.

Celebrating milestones is an important part of life.

The key is balance.

When your income increases, consider dividing the additional money wisely.

For example: Income vs Wealth

- Use part of the raise to improve your lifestyle.

- Save a portion for future goals.

- Increase investments.

- Pay down debt.

- Build additional assets.

This approach allows you to enjoy today’s success while protecting tomorrow’s financial freedom.

Practical Ways to Prevent Lifestyle Inflation

You don’t need to avoid every luxury purchase.

Instead, build habits that keep spending under control as your income grows.

Here are several practical strategies:

- Increase your savings whenever your income increases.

- Invest part of every raise before adjusting your lifestyle.

- Wait at least 30 days before making major purchases.

- Focus on long-term financial goals instead of short-term rewards.

- Review recurring monthly expenses regularly.

- Avoid upgrading simply because friends or coworkers do.

- Track your net worth instead of measuring success by possessions.

- Celebrate financial milestones, not just spending milestones.

Small habits like these help ensure that future raises improve your financial position instead of simply increasing your cost of living.

Choose Financial Freedom Over Lifestyle Inflation

A growing income should create more opportunities, not more financial pressure.

The purpose of earning more isn’t simply to buiny more things.

It’s to create greater security, more choices, and increased financial independence.

Lifestyle inflation quietly convinces people that every raise should lead to a more expensive lifestyle.

Wealth builders think differently.

They allow part of their income to improve their lives today while allowing another part to build the freedom they’ll enjoy tomorrow.