Introduction

Secured vs Unsecured Loans in 2026: Imagine your car suddenly breaks down, your home needs an unexpected repair, or you want to consolidate several high-interest credit card balances into a single payment. Like millions of Americans in 2026, you may find yourself looking for financing options to cover a major expense.

As you begin researching lenders, you’ll quickly discover two primary borrowing choices: secured loans and unsecured loans.

At first glance, both options provide access to money. However, the way they work, the risks involved, the interest rates offered, and the approval requirements can be dramatically different.

With interest rates remaining an important consideration for consumers and household budgets under pressure from rising living costs, choosing the wrong type of loan can lead to unnecessary expenses or financial stress. On the other hand, selecting the right borrowing solution may help you save money, improve cash flow, and achieve your financial goals more efficiently.

In this guide, we’ll break down everything you need to know about secured vs unsecured loans in 2026, including how they work, their advantages and disadvantages, hidden risks many borrowers overlook, and practical tips for making smarter borrowing decisions.

What Is a Loan?

A loan is money borrowed from a lender that must be repaid over time, usually with interest.

When a lender provides a loan, they are taking a financial risk. Because there is always a chance that the borrower may not repay the debt, lenders charge interest as compensation for that risk.

People borrow money for many reasons, including:

- Purchasing a home

- Buying a vehicle

- Paying for education

- Covering medical expenses

- Funding home improvements

- Consolidating debt

- Managing emergency expenses

Before approving a loan, lenders typically evaluate a borrower’s creditworthiness. This includes factors such as:

- Credit score

- Income

- Employment history

- Existing debt obligations

- Payment history

The stronger your financial profile, the better your chances of qualifying for favorable loan terms.

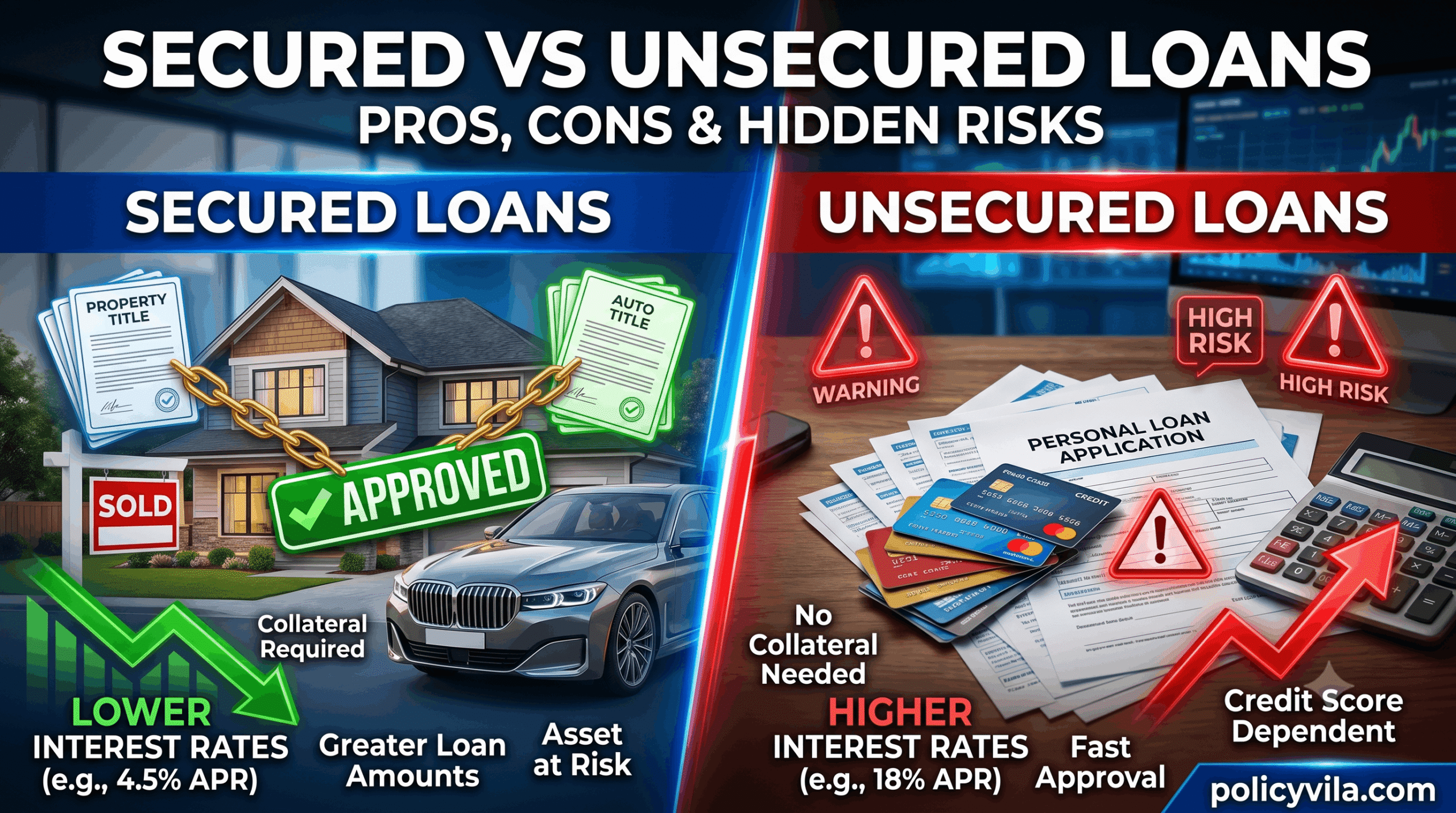

What Is a Secured Loan?

A secured loan is a loan backed by collateral.

Collateral is an asset that the borrower pledges to the lender as security for the loan. If the borrower fails to make payments according to the agreement, the lender may have the legal right to seize the collateral to recover losses.

Because collateral reduces the lender’s risk, secured loans often offer lower interest rates and larger borrowing amounts than unsecured loans.

Common Examples of Secured Loans

Mortgages

A mortgage is one of the most common secured loans. The home itself serves as collateral.

Auto Loans

Vehicle financing is another secured borrowing option. If payments stop, the lender may repossess the vehicle.

Home Equity Loans

Homeowners may borrow against accumulated home equity, using the property as collateral.

Secured Personal Loans

Some lenders allow borrowers to pledge savings accounts, certificates of deposit, or other assets as collateral.

How Collateral Protects Lenders

Suppose a borrower obtains a $30,000 auto loan. If the borrower stops making payments, the lender may repossess and sell the vehicle to recover some or all of the remaining balance.

This protection allows lenders to offer more favorable terms because their financial risk is lower. Secured vs Unsecured Loans in 2026

Advantages of Secured Loans

Lower Interest Rates

One of the biggest advantages of secured loans is lower interest rates.

Because collateral reduces risk, lenders are often willing to charge significantly less interest.

For example:

- A secured loan might carry a 6% APR.

- An unsecured personal loan could carry a 12% APR or higher.

Over several years, that difference can save thousands of dollars.

Higher Borrowing Limits

Secured loans frequently provide access to larger loan amounts.

A borrower using home equity may qualify for substantially more financing than they could obtain through an unsecured personal loan.

This makes secured loans attractive for major expenses such as:

- Home renovations

- Large debt consolidation projects

- Real estate purchases

Easier Approval for Some Borrowers

Borrowers with less-than-perfect credit may find it easier to qualify for a secured loan because the collateral provides additional protection to the lender.

While approval is never guaranteed, collateral can improve borrowing opportunities.

Longer Repayment Terms

Many secured loans offer longer repayment periods.

For example:

- Mortgages often extend 15–30 years.

- Home equity loans may run 5–20 years.

- Auto loans commonly range from 3–7 years.

Longer terms can help reduce monthly payment amounts.

Risks of Secured Loans

Risk of Losing Collateral

The most obvious risk is losing the asset used as collateral.

If payments are missed and the account becomes delinquent, the lender may begin legal proceedings to seize the property.

Foreclosure or Repossession

Homeowners may face foreclosure.

Vehicle owners may experience repossession.

These events can have serious financial and emotional consequences.

Potential Long-Term Debt Burden

Long repayment terms may reduce monthly payments, but they can also increase total interest costs over time.

Borrowers should focus on overall repayment costs, not just monthly affordability.

Over-Borrowing Risks

Because secured loans often provide access to larger amounts of money, borrowers may be tempted to borrow more than they actually need.

Higher balances create larger financial obligations and increase long-term risk.

What Is an Unsecured Loan?

An unsecured loan does not require collateral.

Instead of relying on assets, lenders evaluate a borrower’s financial profile to determine approval.

Approval decisions often depend on:

- Credit score

- Income

- Debt-to-income ratio

- Employment stability

- Payment history

Since lenders assume more risk, unsecured loans generally have higher interest rates.

Common Examples of Unsecured Loans

- Personal loans

- Credit cards

- Student loans

- Medical financing

- Certain debt consolidation loans

Unlike secured loans, borrowers do not risk losing a specific asset if financial hardship occurs.

However, missed payments can still damage credit scores and lead to collection activity.

Advantages of Unsecured Loans

No Asset Risk

The biggest advantage is that no collateral is required.

Borrowers do not place their homes, vehicles, or savings at direct risk when obtaining financing.

Faster Application Process

Many online lenders now offer approvals within minutes and funding within days.

Without collateral evaluations or property appraisals, the process is often quicker.

Greater Flexibility

Borrowers frequently use unsecured personal loans for:

- Debt consolidation

- Emergency expenses

- Medical bills

- Wedding costs

- Home improvements

The funds can often be used for a wide variety of purposes.

Useful for Short-Term Financing Needs

For smaller borrowing needs, unsecured loans can be more practical than pledging valuable assets.

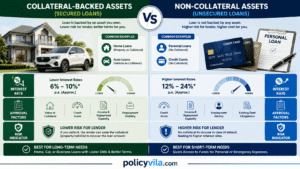

Secured vs Unsecured Loans: Side-by-Side Comparison

When comparing secured loans and unsecured loans, it helps to look beyond interest rates and understand the complete borrowing picture.

| Feature | Secured Loans | Unsecured Loans |

|---|---|---|

| Collateral | Required | Not Required |

| Interest Rates | Usually Lower | Usually Higher |

| Approval Requirements | Often More Flexible | More Credit-Dependent |

| Credit Score Impact | Important | Very Important |

| Loan Amounts | Typically Higher | Typically Lower |

| Repayment Terms | Longer Terms Available | Usually Shorter Terms |

| Funding Speed | May Take Longer | Often Faster |

| Risk to Borrower | Asset Loss Risk | Credit Damage Risk |

| Best For | Large Purchases | Smaller or Short-Term Needs |

Best Use Cases for Secured Loans

Secured loans often work best for:

- Buying a home

- Purchasing a vehicle

- Large home improvements

- Major debt consolidation projects

- Borrowers seeking lower rates

Best Use Cases for Unsecured Loans

Unsecured loans may be better for:

- Medical expenses

- Emergency repairs

- Credit card consolidation

- Small business expenses

- Short-term financing needs

Hidden Risks Most Borrowers Miss

Many borrowers focus only on monthly payments and interest rates. However, several hidden risks can significantly affect the true cost of borrowing.

Variable Interest Rates

Not all loans have fixed rates.

Some lenders offer variable-rate loans where interest rates can change over time.

A loan that seems affordable today could become much more expensive if rates increase.

Example

A borrower starts with a 7% rate. Two years later, the rate adjusts to 11%, increasing monthly payments significantly.

Loan Fees and Charges

Many borrowers overlook fees hidden in loan agreements.

Common fees include:

- Origination fees

- Processing fees

- Application fees

- Late payment penalties

- Returned payment charges

Always review the Annual Percentage Rate (APR), which reflects both interest and many loan-related costs.

Early Repayment Penalties

Some lenders charge penalties when borrowers pay off loans ahead of schedule.

This may seem surprising because paying early sounds responsible, but some lenders lose expected interest income and impose fees.

Before signing any agreement, check whether prepayment penalties apply.

Loan Scams

Financial scams continue evolving in 2026.

Warning signs include:

- Guaranteed approvals

- Requests for upfront fees

- Pressure to act immediately

- No credit check claims

- Unprofessional websites

Legitimate lenders typically evaluate financial information before approving loans.

Predatory Lending Practices

Predatory lenders target financially vulnerable consumers.

Common tactics include:

- Excessive fees

- Extremely high interest rates

- Misleading contract language

- Aggressive collection practices

Always compare multiple lenders before committing.

Impact on Future Borrowing Ability

Taking on additional debt can affect future financial opportunities.

Higher debt levels may reduce your ability to qualify for:

- Mortgages

- Auto financing

- Business loans

- Additional credit lines

Borrowers should think about long-term financial goals before accepting new debt.

Debt Cycle Risks

One of the biggest hidden dangers occurs when borrowers use new loans to repeatedly pay off old loans.

Without addressing spending habits or budgeting issues, debt consolidation can become a temporary solution rather than a permanent fix.

How Credit Scores Affect Loan Approval

Credit scores remain one of the most important factors in loan approval decisions.

Lenders use credit scores to estimate the likelihood that borrowers will repay their obligations.

Higher Credit Scores Often Mean:

- Better approval odds

- Lower interest rates

- Higher borrowing limits

- More lender options

Lower Credit Scores Often Mean:

- Higher interest rates

- Lower loan amounts

- Additional documentation requirements

- Possible loan denials

Tips for Improving Approval Odds

Pay Bills on Time

Payment history remains one of the strongest credit score factors.

Reduce Existing Debt

Lower credit utilization often improves scores.

Review Credit Reports

Check for errors that could negatively affect approval.

Maintain Stable Income

Consistent income improves lender confidence.

Avoid Multiple Applications

Too many applications within a short period may temporarily impact credit scores.

Which Loan Type Is Better for Debt Consolidation?

Debt consolidation loans remain popular in 2026 because they can simplify multiple payments into one manageable loan.

However, both secured and unsecured options have advantages.

Secured Debt Consolidation Loans

Advantages

- Lower interest rates

- Larger loan amounts

- Potentially lower monthly payments

Disadvantages

- Requires collateral

- Risk of losing assets

- Longer repayment periods

Unsecured Debt Consolidation Loans

Advantages

- No collateral required

- Faster approval process

- Less risk to personal assets

Disadvantages

- Higher interest rates

- Lower borrowing limits

- Stronger credit requirements

The right choice depends on your financial situation, credit profile, and comfort with risk.

How to Choose the Right Loan in 2026

Step 1: Evaluate Your Financial Situation

Review:

- Income

- Expenses

- Existing debts

- Savings

Understand your current financial position before borrowing.

Step 2: Determine How Much You Need

Borrow only what is necessary.

Larger loans create larger repayment obligations.

Step 3: Assess Your Risk Tolerance

Ask yourself:

“Am I comfortable using my home, vehicle, or savings as collateral?”

Your answer may help determine whether secured or unsecured borrowing is more appropriate.

Step 4: Compare Multiple Lenders

Never accept the first offer.

Compare:

- Interest rates

- APRs

- Fees

- Repayment terms

- Customer reviews

Step 5: Review Loan Terms Carefully

Read every detail.

Pay attention to:

- Interest rates

- Fees

- Penalties

- Repayment schedules

- Default provisions

Step 6: Calculate Total Borrowing Costs

Focus on total repayment costs, not just monthly payments.

A lower monthly payment may result in significantly more interest over time.

Step 7: Avoid Borrowing More Than Necessary

Borrowing extra money often increases financial pressure later.

Only finance what supports genuine needs or important goals.

Common Borrowing Mistakes to Avoid

Many borrowers make avoidable mistakes that increase borrowing costs.

Ignoring the APR

APR provides a more complete view of loan costs than interest rate alone.

Focusing Only on Monthly Payments

Lower payments may extend repayment and increase total interest.

Borrowing Without a Repayment Plan

Always know how you will repay borrowed funds before accepting a loan.

Missing Important Loan Terms

Review every fee, condition, and requirement carefully.

Applying With Multiple Lenders Simultaneously

Excessive applications can affect credit scores.

Using Loans for Unnecessary Spending

Loans should support important financial goals, not impulse purchases.

Hidden Risks Most Borrowers Miss

Many borrowers focus only on monthly payments and interest rates. However, some of the most expensive loan problems are hidden in the fine print. Understanding these risks can save you thousands of dollars and prevent future financial stress.

Variable Interest Rates

Some loans come with variable interest rates instead of fixed rates. While the initial rate may appear attractive, it can increase over time.

For example, a borrower may start with a 6% rate and later find that it rises to 9% or 10% as market conditions change. This can significantly increase monthly payments and total borrowing costs.

Before signing any loan agreement, ask whether the rate is fixed or variable and understand how future changes may affect repayment.

Loan Fees and Charges

Interest is not the only cost associated with borrowing money.

Some lenders charge:

- Origination fees

- Application fees

- Late payment fees

- Processing fees

- Annual fees

A loan with a slightly lower interest rate may actually cost more if it includes substantial fees.

Always compare the Annual Percentage Rate (APR), which includes both interest and many loan-related charges.

Early Repayment Penalties

Most borrowers assume paying off a loan early is always beneficial.

Unfortunately, some lenders impose prepayment penalties that charge borrowers for paying off debt ahead of schedule.

These penalties can reduce or eliminate the savings gained from early repayment.

Review the loan agreement carefully to determine whether early payoff restrictions apply.

Loan Scams

Financial scams continue to evolve in 2026.

Common warning signs include:

- Guaranteed approval promises

- Requests for upfront fees

- Pressure to act immediately

- Unsolicited loan offers

- Requests for sensitive personal information

Legitimate lenders evaluate creditworthiness and never guarantee approval without reviewing your financial profile.

Predatory Lending Practices

Predatory lenders often target consumers who are struggling financially.

Red flags include:

- Extremely high interest rates

- Hidden fees

- Misleading marketing

- Aggressive collection practices

- Complex loan terms

Borrowers should carefully review all documentation and compare multiple offers before making a decision.

Impact on Future Borrowing Ability

Taking on new debt can affect your ability to qualify for future financing.

Lenders evaluate factors such as:

- Debt-to-income ratio

- Existing loan balances

- Payment history

- Credit utilization

Even if you make payments on time, excessive debt may limit future borrowing opportunities.

Debt Cycle Risks

One of the biggest hidden dangers is becoming trapped in a cycle of debt.

This often occurs when borrowers:

- Use new loans to pay old loans

- Continuously carry credit card balances

- Borrow without addressing spending habits

- Depend on debt for routine expenses

Breaking the debt cycle requires budgeting, financial planning, and disciplined repayment habits.

How Credit Scores Affect Loan Approval

Your credit score plays a major role in determining whether you qualify for a loan and what interest rate you receive.

Lenders use credit scores to estimate the likelihood that borrowers will repay their debts responsibly.

Why Credit Scores Matter

Higher credit scores typically result in:

- Better approval odds

- Lower interest rates

- Higher borrowing limits

- More favorable loan terms

Lower scores may lead to:

- Higher interest rates

- Additional documentation requirements

- Lower loan amounts

- Potential loan denials

Typical Approval Considerations

While every lender has different standards, most evaluate:

- Credit score

- Income stability

- Employment history

- Existing debt obligations

- Payment history

A strong overall financial profile can sometimes offset a less-than-perfect credit score.

Improving Approval Odds

Before applying for a loan:

- Pay bills on time

- Reduce credit card balances

- Review credit reports for errors

- Avoid unnecessary credit applications

- Build emergency savings

Even small improvements can increase approval chances and lower borrowing costs.

Building a Stronger Credit Profile

Good credit habits include:

- Consistent on-time payments

- Responsible credit utilization

- Maintaining older credit accounts

- Diversifying credit types responsibly

Strong credit can save thousands of dollars over a lifetime through lower loan interest rates.

Which Loan Type Is Better for Debt Consolidation?

Debt consolidation loans help combine multiple debts into a single monthly payment.

Both Secured vs Unsecured Loans in 2026 can be used for debt consolidation, but each offers different advantages and disadvantages.

Secured Debt Consolidation Loans

Secured consolidation loans use collateral such as:

- Home equity

- Savings accounts

- Other valuable assets

Potential benefits include:

- Lower interest rates

- Higher loan amounts

- Longer repayment periods

Potential drawbacks include:

- Risk of losing collateral

- Longer debt repayment timeline

- Increased financial exposure

Unsecured Debt Consolidation Loans

Unsecured debt consolidation loans do not require collateral.

Benefits include:

- No asset risk

- Faster approval process

- Simplified borrowing

Drawbacks include:

- Higher interest rates

- Lower borrowing limits

- Greater reliance on credit scores

Which Option Works Best?

The right choice depends on:

- Credit profile

- Debt amount

- Financial stability

- Risk tolerance

- Long-term goals

Borrowers should calculate total repayment costs rather than focusing only on monthly payments.

How to Choose the Right Loan in 2026

Choosing between secured loans and unsecured loans requires careful evaluation.

Evaluate Your Financial Situation

Review:

- Income

- Expenses

- Existing debts

- Emergency savings

Understanding your finances helps determine what loan fits your needs.

Determine How Much You Need

Borrow only what is necessary.

Excessive borrowing increases interest costs and repayment risk.

Assess Your Risk Tolerance

Ask yourself:

“Am I comfortable putting an asset at risk for a lower interest rate?”

The answer can help determine whether a secured loan is appropriate.

Compare Multiple Lenders

Never accept the first offer.

Compare:

- APRs

- Fees

- Repayment terms

- Customer reviews

- Funding speed

Review Loan Terms Carefully

Read all disclosures before signing.

Pay attention to:

- Interest rate structure

- Fees

- Penalties

- Payment schedules

Calculate Total Borrowing Costs

The cheapest monthly payment is not always the most affordable loan.

Consider:

- Total interest paid

- Fees

- Repayment length

Avoid Borrowing More Than Necessary

Borrowing beyond your actual needs can create unnecessary financial pressure.

A smaller loan is often easier to manage and repay.

Common Borrowing Mistakes to Avoid

Many financial problems begin with avoidable borrowing mistakes.

Ignoring the APR

APR provides a more complete picture of loan costs than interest rate alone.

Focusing Only on Monthly Payments

Lower monthly payments often mean longer repayment periods and higher total interest costs.

Borrowing Without a Repayment Plan

Every loan should have a clear repayment strategy before funds are borrowed.

Missing Loan Terms

Important details such as fees and penalties are often overlooked.

Applying With Multiple Lenders at Once

Too many applications within a short period may affect credit scores.

Using Loans for Unnecessary Spending

Loans should support important financial goals, not impulse purchases.

Loan Trends to Watch in 2026

The lending industry continues to evolve rapidly.

Digital Lending Platforms

Online lenders now provide faster approvals and simplified applications.

AI-Powered Loan Approvals

Artificial intelligence helps lenders evaluate borrowers more efficiently.

Faster Online Applications

Many applicants can now complete the process within minutes.

Increased Financial Transparency

Consumers increasingly demand clear pricing and simplified disclosures.

Alternative Credit Scoring Methods

Some lenders evaluate additional factors beyond traditional credit scores, helping more borrowers access financing.

read also: Personal Financial Statement Guide 2026: The Smartest Way to Track Wealth, Assets & Net Worth

Frequently Asked Questions (FAQs)

Is a secured loan better than an unsecured loan?

Neither option is automatically better. Secured loans generally offer lower interest rates and larger borrowing limits because collateral reduces lender risk. Unsecured loans, however, do not require assets as security, making them attractive for borrowers who want to avoid risking personal property.

The best choice depends on your financial situation, credit profile, borrowing needs, and risk tolerance.

Can I get a loan with poor credit?

Yes, it is possible to obtain a loan with poor credit, but options may be more limited.

Borrowers with lower credit scores often face:

- Higher interest rates

- Lower loan limits

- Additional documentation requirements

- Stricter approval standards

Some secured loans may be easier to qualify for because collateral reduces lender risk.

What happens if I miss loan payments?

Missing payments can lead to several consequences:

- Late fees

- Negative credit reporting

- Increased borrowing costs

- Collection activity

For secured loans, repeated missed payments may eventually result in foreclosure, repossession, or loss of collateral.

For unsecured loans, lenders may pursue collection efforts and legal remedies depending on the circumstances.

Which loan type usually has lower interest rates?

Secured vs Unsecured Loans in 2026 typically offer lower interest rates because collateral protects lenders against losses.

Examples include:

- Mortgages

- Auto loans

- Home equity loans

- Secured personal loans

Unsecured loans generally have higher rates because lenders assume greater risk.

Do unsecured loans require collateral?

No. Unsecured loans do not require collateral.

Approval is based primarily on:

- Credit score

- Income

- Debt-to-income ratio

- Employment stability

- Overall creditworthiness

This makes unsecured loans convenient, but they often come with higher interest rates.

Can debt consolidation loans improve my finances?

Debt consolidation loans can simplify repayment by combining multiple debts into a single monthly payment.

Potential benefits include:

- Easier budgeting

- Lower interest rates (in some cases)

- Reduced financial stress

However, consolidation works best when combined with responsible spending habits and a clear debt repayment plan.

How long does loan approval usually take?

Approval times vary by lender.

Traditional banks may require several days or weeks.

Many online lenders now offer:

- Same-day decisions

- Next-day funding

- Fully digital applications

Borrowers should compare funding speed if they need money quickly.

Final Verdict: Secured vs Unsecured Loans in 2026

Understanding the differences between secured loans and unsecured loans is one of the most important financial decisions borrowers can make.

Secured loans offer:

- Lower interest rates

- Higher borrowing limits

- Longer repayment periods

But they also carry the risk of losing valuable assets if payments are not made.

Unsecured loans provide:

- No collateral requirements

- Faster approval processes

- Greater flexibility

However, they often come with higher interest rates and stricter approval standards.

When evaluating a personal loan comparison, borrowers should focus on:

- Total borrowing costs

- Interest rates

- Fees

- Repayment terms

- Financial goals

- Risk exposure

There is no universal winner. The right choice depends on your unique financial situation.

Conclusion: Secured vs Unsecured Loans in 2026

Choosing between Secured vs Unsecured Loans in 2026 requires more than simply comparing interest rates.

A loan can be a valuable financial tool when used responsibly, but it can also create long-term financial challenges if borrowers fail to understand the risks involved.

Before borrowing money, take time to:

- Compare multiple lenders

- Review loan terms carefully

- Understand all fees and charges

- Calculate total repayment costs

- Evaluate your ability to repay the debt

- Consider the impact on your long-term financial goals

Remember that the best loan is not necessarily the largest loan, the fastest loan, or even the easiest loan to obtain. The best loan is the one that fits your financial situation, supports your objectives, and can be repaid comfortably without creating unnecessary stress.

Whether you choose Secured vs Unsecured Loans in 2026, unsecured loans, or debt consolidation loans, informed decision-making remains your strongest financial advantage in 2026 and beyond.