Introduction

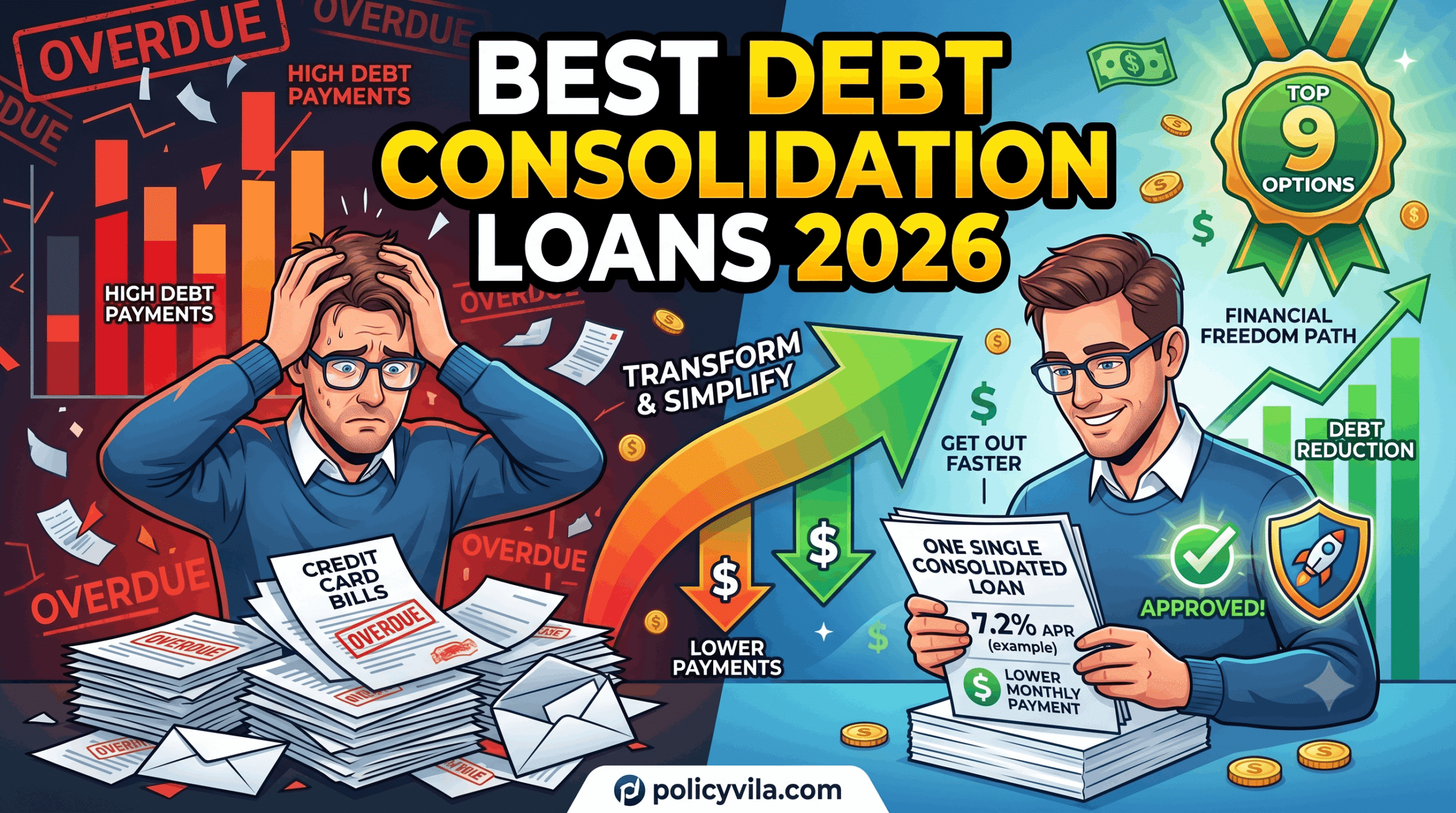

Best Debt Consolidation Loans in 2026: Imagine checking your bank account and realizing that you have five separate debt payments due in the next two weeks.

There’s a credit card bill with a 27% interest rate, a personal loan payment, a store financing account, and maybe even a medical payment plan. Every month feels like a magic bullet, and despite making regular payments, the balance never goes down as quickly as you’d hope.

For millions of Americans, this scenario will continue to be a reality in 2026.

The rising cost of living, high interest rates, unexpected emergencies, and rising household expenses continue to strain family budgets. Even financially responsible consumers can find themselves carrying multiple debts that become difficult to manage.

This is where debt consolidation loans enter the conversation.

Debt consolidation loans allow borrowers to combine multiple debts into a single loan with one monthly payment. In many cases, borrowers can qualify for lower interest rates, simplifying their finances and creating a clear path toward becoming debt-free.

In this guide, you’ll learn how debt consolidation works, who should consider it, how to compare loan options, and the best debt consolidation loans in 2026 for different financial situations.

What Is a Debt Consolidation Loan?

A debt consolidation loan is a type of loan that is used to combine multiple debts into one new loan.

Instead of making multiple payments to different creditors, you use the new loan to pay off existing debts and then make one monthly payment to one lender.

A Simple Example

Let’s say Sarah has:

- Credit Card A: $4,000 at 26% APR

- Credit Card B: $3,000 at 24% APR

- Personal Loan: $5,000 at 15% APR

Total debt: $12,000

Instead of managing three separate payments, Sarah gets a $12,000 debt consolidation loan at 10% APR.

The new loan pays off her existing balance, giving her one payment, one due date, and potentially lower interest costs.

For many borrowers, this simplification is one of the biggest benefits of a debt consolidation loan.

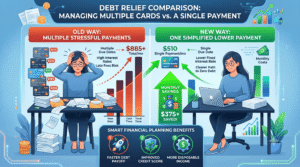

How Debt Consolidation Can Lower Monthly Payments

One reason debt consolidation remains popular is its ability to reduce monthly payment pressure.

Lower Interest Rates

Many borrowers use debt consolidation to replace high-interest credit card balances with lower-interest personal loans.

For example:

- Credit card APR: 25%

- Consolidation loan APR: 10%

The difference can significantly reduce interest charges over time.

Longer Repayment Terms

Some consolidation loans offer repayment terms ranging from two to seven years.

Spreading payments over a longer period of time can reduce monthly obligations.

However, borrowers should remember that increasing payments can increase the total interest paid over the life of the loan.

Easier Budgeting

Managing one payment is often simpler than tracking several due dates.

This can reduce missed payments and make monthly cash flow easier to manage.

Reduced Financial Stress

Many people report feeling more in control once multiple debts are consolidated into a single repayment plan.

While debt consolidation isn’t a magic solution, it can provide valuable breathing room for borrowers committed to paying down debt.

Benefits of Debt Consolidation Loans

Simplified Payments

Perhaps the most obvious benefit is convenience.

Instead of having to remember multiple due dates and payment amounts, borrowers make one payment each month.

This reduces administrative headaches and reduces the risk of accidentally missing a payment.

Potential Interest Savings

If the new loan carries a lower interest rate than existing debts, borrowers may save money over time.

This is particularly important for consumers carrying high-interest credit card balances.

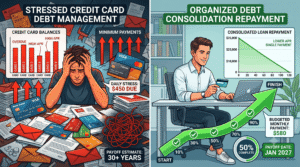

Faster Debt Repayment

Many lenders provide structured repayment schedules.

Having a clear payoff date can help borrowers stay motivated and focused on becoming debt-free.

Improved Financial Organization

Debt consolidation can provide a clearer picture of overall debt obligations.

Instead of tracking several balances, borrowers focus on one loan with one payoff goal.

Potential Credit Score Benefits

Responsible use of debt consolidation may positively affect credit scores over time.

Benefits may include:

- Lower credit utilization

- Consistent payment history

- Reduced risk of missed payments

However, borrowers should avoid accumulating new debt after consolidation.

Who Should Consider Debt Consolidation?

Debt consolidation isn’t the right solution for everyone.

However, it may be beneficial for several types of borrowers.

People With Multiple Credit Card Balances

Managing multiple high-interest credit cards can become expensive.

Consolidation may simplify repayment and potentially lower interest costs.

Borrowers With High-Interest Debt

Consumers paying 20% or more on revolving debt may benefit from lower-rate consolidation loans.

Families Managing Household Expenses

Families balancing childcare, housing, transportation, and debt payments often appreciate the simplicity of a single monthly payment.

Consumers With Stable Income

Lenders generally prefer borrowers with reliable income sources.

A stable income can also make repayment more manageable.

Individuals Committed to Avoiding New Debt

Consolidation works best when borrowers stop adding new debt after paying off existing balances.

When Consolidation May Not Be Ideal

Debt consolidation may not be the best option if:

- Your credit score is too low to qualify for favorable rates.

- You have minimal debt.

- You continue overspending after consolidation.

- Fees outweigh potential savings.

In these situations, alternative debt management solutions may be worth exploring.

read also: Term Life Insurance vs Whole Life Insurance in 2026: The Truth Most Insurance Agents Won’t Tell You

1. Online Personal Loan Lenders

Overview

Online lenders continue to dominate the debt consolidation market due to convenience and competitive rates.

Best For

Borrowers seeking fast approval and digital applications.

Key Benefits

- Quick applications

- Fast funding

- Competitive interest rates

- Flexible loan amounts

Potential Drawbacks

- Rates vary significantly based on credit score

- Some lenders charge origination fees

Typical Borrower Profile

Consumers with fair to excellent credit seeking convenience and speed.

2. Credit Union Debt Consolidation Loans

Overview

Credit unions often offer member-focused lending programs with competitive rates.

Best For

Borrowers seeking personalized service and lower borrowing costs.

Key Benefits

- Competitive rates

- Community-focused lending

- Flexible qualification standards

Potential Drawbacks

- Membership requirements

- Limited branch availability in some areas

Typical Borrower Profile

Borrowers who value customer service and long-term banking relationships.

3. Traditional Bank Personal Loans

Overview

Banks remain a common source of debt consolidation financing.

Best For

Existing banking customers seeking familiar institutions.

Key Benefits

- Established reputation

- In-person support

- Relationship discounts may be available

Potential Drawbacks

- Stricter approval standards

- Slower funding in some cases

Typical Borrower Profile

Consumers with strong credit histories and established banking relationships.

4. Fixed-Rate Consolidation Loans

Overview

Fixed-rate consolidation loans offer predictable monthly payments throughout the entire repayment period.

Best For

Borrowers who value stability and want to avoid surprises.

Key Benefits

- Consistent monthly payments

- Easier budgeting

- Protection from interest rate increases

Potential Drawbacks

- May not offer the lowest initial rates

- Qualification standards vary

Typical Borrower Profile

Consumers who prefer financial predictability and long-term planning.

5. Loans for Excellent Credit Borrowers

Overview

Borrowers with strong credit profiles often qualify for the most competitive rates.

Best For

Consumers with excellent credit scores and strong financial histories.

Key Benefits

- Lowest available APRs

- Higher borrowing limits

- Better loan terms

Potential Drawbacks

- Requires strong credit

- Competitive approval process

Typical Borrower Profile

Individuals with excellent payment history and low credit utilization.

6. Debt Consolidation Loans for Fair Credit

Overview

Many lenders now offer programs designed for borrowers with fair credit scores.

Best For

Consumers working to improve their financial situation.

Key Benefits

- Broader approval opportunities

- Potentially lower rates than credit cards

- Structured repayment plans

Potential Drawbacks

- Higher APRs than prime borrowers

- Additional qualification requirements

Typical Borrower Profile

Borrowers rebuilding credit while seeking manageable monthly payments.

7. Loans with Fast Funding

Overview

Fast-funding lenders can sometimes approve and fund loans within one or two business days.

Best For

Consumers facing urgent debt situations.

Key Benefits

- Quick access to funds

- Convenient online application process

- Immediate debt payoff opportunities

Potential Drawbacks

- Rates may be higher

- Loan options can be more limited

Typical Borrower Profile

Individuals needing immediate financial restructuring.

8. Low-Fee Consolidation Loans

Overview

Some lenders focus on minimizing fees rather than simply advertising low rates.

Best For

Cost-conscious borrowers.

Key Benefits

- Lower origination fees

- Fewer hidden charges

- Better transparency

Potential Drawbacks

- APR may not always be the lowest

- Qualification standards vary

Typical Borrower Profile

Borrowers focused on minimizing total borrowing costs.

9. Family-Friendly Budget Consolidation Loans

Overview

These loan options prioritize affordability and manageable repayment structures.

Best For

Families balancing multiple financial obligations.

Key Benefits

- Flexible repayment terms

- Predictable payments

- Budget-friendly structures

Potential Drawbacks

- Longer repayment periods

- Potentially higher total interest costs

Typical Borrower Profile

Households managing childcare expenses, mortgages, and multiple debt obligations.

How to Compare Debt Consolidation Loans

Not all debt consolidation loans are created equal. Comparing offers carefully can save hundreds or even thousands of dollars.

Interest Rates

The Annual Percentage Rate (APR) reflects the total cost of borrowing.

Even a small rate difference can significantly impact long-term costs.

Loan Terms

Shorter terms:

- Higher monthly payments

- Lower total interest

Longer terms:

- Lower monthly payments

- Higher total interest

Monthly Payment Amount

Choose a payment you can realistically afford while still making meaningful progress toward debt reduction.

Fees

Look for:

- Origination fees

- Late fees

- Prepayment penalties

- Administrative charges

Funding Speed

Some borrowers need funds quickly to address urgent debt situations.

Customer Support

Responsive customer service becomes especially important during financial challenges.

Debt Consolidation Loan vs. Balance Transfer Credit Card

Many consumers wonder whether a debt consolidation loan or balance transfer card is the better option. Best Debt Consolidation Loans in 2026

| Feature | Debt Consolidation Loan | Balance Transfer Card |

|---|---|---|

| Fixed Payment | Yes | Usually No |

| Fixed Payoff Date | Yes | Varies |

| Interest Rate Stability | High | Introductory Offers May Expire |

| Best For Large Debt | Yes | Sometimes |

| Credit Requirements | Moderate to High | Often Higher |

| Simplicity | Very High | Moderate |

When a Consolidation Loan May Be Better

- Large balances

- Multiple debts

- Desire for structured repayment

When a Balance Transfer May Be Better

- Smaller balances

- Ability to pay debt quickly

- Excellent credit profile

Common Debt Consolidation Mistakes to Avoid

Consolidating Without Changing Spending Habits

A new loan does not solve overspending.

Ignoring Fees

Always calculate total borrowing costs.

Choosing the Longest Term Available

Lower payments may increase total interest significantly.

Missing Payments

One missed payment can damage credit and trigger penalties.

Applying to Too Many Lenders

Multiple applications can temporarily affect credit scores.

Failing to Compare Offers

Even small APR differences matter.

Closing Credit Accounts Immediately

This can sometimes affect credit utilization ratios.

Borrowing More Than Needed

Only consolidate existing debt.

Not Creating a Budget

A repayment plan should be supported by realistic spending habits.

Expecting Instant Results

Debt consolidation is a tool, not a quick fix.

read also: Progressive Insurance Review 2026: Rates, Coverage, Discounts & Hidden Benefits Most Drivers Miss

How to Qualify for a Best Debt Consolidation Loans in 2026

Lenders evaluate several factors.

Credit Score

Higher scores generally qualify for better rates.

Income

Stable income demonstrates repayment ability.

Employment Stability

Consistent employment can improve approval odds.

Existing Debt Levels

Lenders examine overall debt obligations.

Debt-to-Income Ratio

This measures monthly debt payments relative to income.

Tips to Improve Approval Chances

- Pay bills on time

- Reduce credit card balances

- Review credit reports for errors

- Avoid unnecessary credit applications

- Increase income when possible

Step-by-Step Process for Applying

Step 1: Review Current Debts

List every balance, rate, and monthly payment.

Step 2: Check Credit Reports

Understand your credit standing before applying.

Step 3: Compare Multiple Loan Offers

Never accept the first offer without comparison.

Step 4: Calculate Total Costs

Look beyond monthly payments.

Step 5: Submit an Application

Provide accurate financial information.

Step 6: Pay Off Existing Debts

Use consolidation funds responsibly.

Step 7: Follow a Debt Repayment Plan

Stay disciplined and avoid accumulating new debt.

Debt Consolidation Trends in 2026

Increased Online Lending

Digital lenders continue expanding consumer access.

AI-Powered Loan Matching

Technology helps borrowers find suitable loan options faster.

Faster Approvals

Many lenders now offer near-instant decisions.

Financial Wellness Programs

Lenders increasingly provide budgeting and education resources.

Improved Consumer Education

Borrowers have greater access to financial tools and resources than ever before.

read also: Health Insurance Deductibles Explained: What Every Family Must Know in 2026

Frequently Asked Questions

Does debt consolidation hurt your credit score?

Initially, a new loan application may cause a small temporary decline. Over time, responsible repayment can help improve credit profiles.

Can debt consolidation save money?

Yes, if the new loan has a lower interest rate and reasonable fees.

Is debt consolidation better than debt settlement?

Debt consolidation repays debts in full, while debt settlement involves negotiating reduced balances. Each has different risks and benefits.

What credit score is needed?

Requirements vary by lender, but higher scores generally receive better rates.

How long does approval take?

Some lenders approve applications within minutes, while others take several days.

Can I consolidate credit card debt only?

Yes. Many borrowers use consolidation loans specifically to consolidate credit card debt.

Are secured loans better than unsecured loans?

Secured loans may offer lower rates but require collateral.

Will debt consolidation eliminate my debt?

No. It reorganizes debt into a more manageable structure.

Can I pay off a consolidation loan early?

Many lenders allow early repayment, though borrowers should verify terms.

Is debt consolidation right for everyone?

No. It works best for borrowers committed to long-term financial discipline.

Final Verdict

The best debt consolidation loans in 2026 can help simplify finances, reduce financial stress, and create a structured path to becoming debt-free.

Some of the biggest benefits include:

One monthly payment

Potentially lower interest rates

Easier budgeting

Better financial organization

However, consolidation is not a cure-all. Borrowers who continue to accumulate debt or fail to carefully compare loan offers may not achieve the results they expect.

Conclusion

Debt can feel overwhelming, especially when multiple balances, interest rates, and payment dates compete for your attention every month. Fortunately, Best Debt Consolidation Loans in 2026 remain one of the most effective debt management solutions available in 2026.

When used responsibly, a personal loan for debt consolidation can simplify repayment, reduce financial stress, and help borrowers regain control of their finances. The key is choosing the right loan, understanding the true cost of borrowing, and committing to a realistic debt payoff strategy.

Before making a decision, compare multiple offers, evaluate fees carefully, and consider how each option fits your long-term financial goals. With the right approach, consolidating Best Debt Consolidation Loans in 2026can become an important step toward financial freedom and a stronger financial future.