Hook Introduction

Term Life Insurance vs Whole Life Insurance: Imagine you’re a parent with two young children. You know life insurance is important, so you decide to get coverage to protect your family. After speaking with two insurance agents, you receive two completely different recommendations.

The first agent suggests a term life insurance policy that costs less than a monthly streaming subscription. The second recommends a whole life insurance policy with much higher premiums but promises lifelong coverage and cash value growth.

Now you’re confused.

If both policies provide a death benefit, why is one dramatically more expensive? More importantly, which option is actually right for your family?

This is where many consumers get stuck.

Whether you’re focused on protecting your income, paying off a mortgage, building wealth, or leaving an inheritance, the type of life insurance you choose can have a lasting impact on your financial future.

Why Life Insurance Still Matters in 2026

Some people believe life insurance is only necessary for older adults or wealthy families. In reality, life insurance remains a critical financial tool for millions of Americans.

Rising Living Costs

The cost of housing, healthcare, education, and everyday essentials continues to increase. If a family’s primary income earner passes away unexpectedly, replacing that lost income can become extremely difficult.

Life insurance helps provide a financial safety net during one of life’s most challenging situations.

Family Financial Obligations

Many households rely on multiple financial commitments, including:

- Mortgage payments

- Car loans

- Credit card balances

- Childcare expenses

- College savings goals

Without life insurance, surviving family members may struggle to maintain their standard of living.

Mortgage Protection

For many families, a home is their largest financial asset.

A life insurance policy can help ensure loved ones can continue making mortgage payments or even pay off the home entirely after the insured person’s death.

Income Replacement

One of the primary purposes of life insurance is income replacement.

For example, if a 35-year-old parent earns $80,000 annually and passes away unexpectedly, their family could lose hundreds of thousands of dollars in future income. Life insurance can help bridge that financial gap.

Estate Planning

Life insurance also plays a valuable role in estate planning.

Policy benefits can provide heirs with immediate financial support, help cover estate-related expenses, and create a tax-efficient transfer of wealth in certain situations.

What Is Term Life Insurance?

Term life insurance is often considered the simplest and most affordable type of life insurance available.

How Term Life Insurance Works

A term life insurance policy provides coverage for a specific period, known as the policy term.

If the insured person dies during that term, the insurance company pays a death benefit to the designated beneficiaries.

If the term expires and the policyholder is still living, coverage typically ends unless the policy is renewed or converted.

Common Coverage Lengths

Most insurers offer term life insurance policies with coverage periods such as:

- 10 years

- 15 years

- 20 years

- 25 years

- 30 years

Many families choose a term that aligns with major financial obligations, such as raising children or paying off a mortgage.

Who Typically Buys Term Insurance?

Term life insurance is popular among:

- Young families

- First-time parents

- Homeowners

- Individuals with limited budgets

- People seeking maximum coverage for the lowest cost

For example, a healthy 30-year-old may be able to purchase hundreds of thousands of dollars in coverage for a relatively low monthly premium.

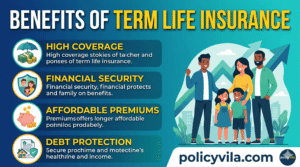

Main Advantages

Term life insurance offers several key benefits:

Affordable Premiums

The biggest advantage is cost.

Because coverage lasts for a limited period, premiums are generally much lower than whole life insurance.

Simple Structure

Term policies are easy to understand.

You pay premiums, maintain coverage during the term, and beneficiaries receive a death benefit if a covered loss occurs.

High Coverage Amounts

Many families can afford larger death benefits through term insurance compared to permanent policies.

What Is Whole Life Insurance?

Whole life insurance is a form of permanent life insurance designed to provide coverage for an individual’s entire lifetime.

Unlike term insurance, whole life policies do not expire as long as premiums are paid according to policy requirements.

How Whole Life Insurance Works

A whole life insurance policy combines two components:

- Death benefit protection

- Cash value accumulation

Part of each premium helps fund the death benefit, while another portion contributes to the policy’s cash value account.

Over time, the cash value grows and may become a financial asset for the policyholder.

Permanent Coverage

One of the biggest selling points of whole life insurance is lifelong protection.

As long as policy requirements are met, beneficiaries are generally guaranteed to receive a death benefit regardless of when the insured person passes away.

This feature appeals to people who want certainty and permanent coverage.

Cash Value Component

The cash value feature distinguishes whole life insurance from term life insurance.

Over time, policyholders build cash value that can potentially be:

- Borrowed against

- Used for emergencies

- Accessed through policy loans

- Incorporated into long-term financial planning

However, cash value growth is typically gradual and should be evaluated carefully against other investment opportunities.

Main Advantages

Whole life insurance offers several potential benefits:

Lifetime Coverage

Protection remains in force for life rather than a limited term.

Predictable Premiums

Many policies lock in premium amounts, creating predictable long-term costs.

Cash Value Growth

Policyholders accumulate cash value that can provide additional financial flexibility.

Estate Planning Benefits

Whole life insurance is often used as part of broader estate and wealth transfer strategies.

For individuals seeking lifelong protection and a guaranteed death benefit, whole life insurance can be an attractive option despite its higher cost.

Key Differences Between Term Life Insurance vs Whole Life Insurance

At first glance, both term life insurance and whole life insurance provide the same core benefit: a death benefit that helps protect your loved ones financially after your death.

However, the similarities end there.

Understanding the differences between these two policy types is critical because the wrong choice can affect your long-term financial goals, monthly budget, and overall insurance strategy.

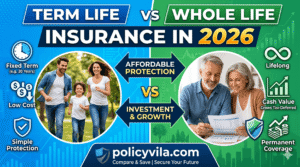

Coverage Duration

The biggest difference is how long coverage lasts.

Term life insurance provides protection for a specific period, such as 10, 20, or 30 years. Once the term expires, coverage generally ends unless you renew or convert the policy.

Whole life insurance is designed to provide lifelong coverage. As long as premiums are paid, the policy remains active for the insured person’s entire life.

Premium Costs

Premium costs are often the deciding factor for many families.

Term life insurance is usually far more affordable because coverage is temporary and does not include a cash value component.

Whole life insurance costs significantly more because it combines permanent protection with cash value accumulation.

In many cases, a whole life policy can cost five to fifteen times more than a comparable term policy.

This difference often surprises first-time buyers.

Cash Value Growth

Term life insurance focuses solely on protection.

If the policy expires and no claim is filed, there is generally no cash value or savings component.

Whole life insurance includes a cash value account that grows over time.

Part of each premium contributes to this cash value, which may be accessed through policy loans or withdrawals depending on the policy terms.

While this feature can be useful, it’s important to understand that cash value growth is often slower than many people expect during the early years of a policy.

Investment Features

Some insurance agents market whole life insurance as both protection and an investment.

While whole life policies do offer cash value growth, they should not automatically be viewed as a replacement for traditional investment accounts.

Term life insurance has no investment component.

Instead, many financial experts recommend purchasing affordable term coverage and investing the premium savings separately through retirement accounts or other investment vehicles.

This approach is often called “buy term and invest the difference.”

Flexibility

Term life insurance offers flexibility because policyholders can choose coverage periods that match their financial responsibilities.

For example:

- Mortgage payoff timeline

- Children’s education years

- Business loan obligations

- Income replacement needs

Whole life insurance offers less flexibility because it is designed as a permanent solution.

Policyholders generally commit to much higher premiums for decades.

Death Benefits

Both policy types provide a death benefit.

The primary difference is how long that protection remains available.

Term insurance pays a death benefit only if the insured dies during the coverage period.

Whole life insurance generally guarantees a death benefit as long as premiums remain current.

For families focused on temporary protection needs, term insurance may be sufficient.

For those seeking permanent coverage and estate planning benefits, whole life may offer advantages.

When Term Life Insurance Makes More Sense

For many Americans, term life insurance is the most practical solution.

Young Families

Parents with young children often need maximum coverage while managing tight budgets.

Term insurance allows them to secure substantial protection without sacrificing other financial priorities.

Mortgage Protection

Many homeowners purchase term policies that align with their mortgage repayment schedule.

For example, a 30-year mortgage often pairs naturally with a 30-year term policy.

Income Replacement

If your primary goal is replacing lost income during your working years, term insurance usually provides the most cost-effective solution.

Debt Protection

Families with:

- Student loans

- Personal loans

- Business debts

- Credit obligations

often benefit from affordable term coverage.

Building Wealth Through Investments

Some individuals prefer buying inexpensive term insurance and investing the savings elsewhere.

For example, if a whole life policy costs $300 more per month than a comparable term policy, that difference could potentially be invested in retirement accounts, index funds, or other long-term assets.

Budget-Conscious Households

Many households simply need protection without the added complexity of cash value features.

Term insurance provides straightforward coverage that is easy to understand and manage.

For these reasons, term life insurance remains the most commonly recommended option for young families, first-time insurance buyers, and individuals focused on maximizing protection while minimizing costs.

When Whole Life Insurance Makes More Sense

Although term life insurance is often the best choice for many families, there are situations where whole life insurance may provide unique advantages.

The key is understanding whether those advantages align with your personal financial goals.

Lifetime Dependents

Some individuals have dependents who may require financial support for their entire lives.

Examples include: Term Life Insurance vs Whole Life Insurance

- Children with special needs

- Family members with disabilities

- Dependents requiring long-term care

In these situations, a policy that expires after 20 or 30 years may not provide adequate protection.

Whole life insurance offers permanent coverage that remains in force regardless of when the insured person dies.

For families with lifelong financial responsibilities, this can provide valuable peace of mind.

Estate Planning

Whole life insurance is commonly used as part of estate planning strategies.

A death benefit can help:

- Cover estate taxes

- Preserve family assets

- Equalize inheritances among heirs

- Provide immediate liquidity

For example, a family business owner may use a whole life policy to ensure heirs receive financial support without needing to sell business assets.

High Net Worth Families

Wealthy individuals often have different insurance needs than average households.

For some high-net-worth families, whole life insurance can serve as a tool for:

- Wealth preservation

- Legacy planning

- Charitable giving

- Asset transfer strategies

These situations are typically more complex and often involve professional financial and legal guidance.

Long-Term Wealth Strategies

Some people value the predictable nature of whole life insurance.

Because policies can accumulate cash value over time, they may become part of a broader financial strategy.

Supporters of whole life insurance often appreciate:

- Guaranteed death benefits

- Fixed premiums

- Tax-advantaged cash value growth

- Long-term stability

However, it’s important to evaluate these benefits carefully against the higher costs involved.

Whole life insurance is not automatically a superior financial product—it simply serves a different purpose than term insurance.

The Hidden Costs Most Agents Don’t Mention

Many life insurance buyers focus exclusively on premiums and death benefits.

Unfortunately, some of the most important costs are rarely discussed during the sales process.

Understanding these hidden costs can help you make a more informed decision.

Policy Fees

Whole life insurance policies often include various administrative and policy-related costs.

These expenses may impact:

- Cash value growth

- Early surrender value

- Overall policy performance

Many buyers don’t fully understand these costs until years after purchasing coverage.

Reading policy documents carefully is essential.

Opportunity Costs

Opportunity cost is one of the most overlooked financial concepts in insurance planning.

For example:

If a whole life policy costs $350 more per month than a comparable term policy, that’s $4,200 per year.

Over decades, those funds could potentially be invested elsewhere.

This doesn’t automatically make term insurance superior.

However, buyers should compare what those dollars might achieve through:

- Retirement accounts

- Index funds

- Emergency savings

- Other investments

Underperforming Cash Value Growth

Many buyers assume cash value will grow rapidly.

In reality, growth is often slow during the early years of a policy.

A large portion of initial premiums may be allocated toward:

- Insurance costs

- Administrative expenses

- Commissions

As a result, policyholders may discover that cash value accumulation takes longer than expected.

Understanding realistic growth expectations is critical before purchasing any permanent life insurance policy.

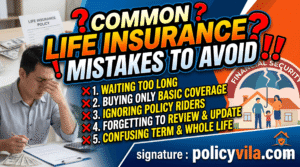

Common Life Insurance Mistakes

Life insurance can be an extremely effective financial tool, but mistakes are surprisingly common.

1. Waiting Too Long to Buy Coverage

Why It Happens

People assume they can purchase coverage later.

Consequences

Premiums increase with age.

Health problems may also limit eligibility.

Better Alternative

Buy coverage while you’re young and healthy.

2. Choosing Coverage Based Only on Price

Why It Happens

Consumers naturally want to save money.

Consequences

Coverage may be insufficient.

Better Alternative

Balance affordability with adequate protection.

3. Buying Too Little Coverage

Why It Happens

People underestimate future financial needs.

Consequences

Beneficiaries may face financial hardship.

Better Alternative

Calculate realistic income replacement needs.

4. Ignoring Inflation

Why It Happens

Current expenses seem manageable.

Consequences

Future benefits may be inadequate.

Better Alternative

Review coverage regularly.

5. Not Comparing Multiple Quotes

Why It Happens

Consumers accept the first offer.

Consequences

Higher premiums.

Better Alternative

Compare several insurers before purchasing.

6. Naming Outdated Beneficiaries

Why It Happens

Life circumstances change.

Consequences

Benefits may go to unintended recipients.

Better Alternative

Review beneficiary designations periodically.

7. Assuming Employer Coverage Is Enough

Why It Happens

Employer policies seem convenient.

Consequences

Coverage may disappear if employment ends.

Better Alternative

Maintain personal coverage as well.

8. Buying a Complex Policy Without Understanding It

Why It Happens

Insurance terminology can be confusing.

Consequences

Unexpected costs and disappointment.

Better Alternative

Ask questions until every feature is clear.

9. Failing to Review Policies Over Time

Why It Happens

Insurance is often forgotten after purchase.

Consequences

Coverage may no longer fit current needs.

Better Alternative

Review policies every few years.

10. Treating Insurance as an Investment First

Why It Happens

Marketing often emphasizes cash value.

Consequences

Protection needs may become secondary.

Better Alternative

Prioritize family protection first and investment goals second.

Term Life Insurance vs Whole Life Insurance Comparison Table

Choosing between term life insurance and whole life insurance becomes easier when you compare their core features side by side.

| Feature | Term Life Insurance | Whole Life Insurance |

|---|---|---|

| Cost | Lower premiums | Higher premiums |

| Coverage Duration | Fixed term (10–30 years typically) | Lifetime coverage |

| Death Benefit | Paid if death occurs during policy term | Guaranteed as long as premiums are paid |

| Cash Value | No cash value | Builds cash value over time |

| Investment Component | None | Includes cash value accumulation |

| Premium Stability | Usually fixed during the term | Generally fixed for life |

| Flexibility | Can choose specific coverage periods | Designed for permanent protection |

| Complexity | Simple and easy to understand | More complex |

| Best For | Families, income protection, mortgage coverage | Estate planning, lifelong dependents, wealth transfer |

| Affordability | Highly affordable | Significantly more expensive |

| Long-Term Value | Strong protection-to-cost ratio | Combines insurance and savings features |

| Popularity | Most common choice for families | More specialized financial tool |

Key Takeaway

For most households, term life insurance provides significantly more coverage for every dollar spent.

Whole life insurance can make sense in specific situations, but its higher costs require careful evaluation.

Life Insurance Myths vs Facts

Many consumers make decisions based on misinformation rather than facts.

Let’s separate common myths from reality.

| Myth | Fact |

| Life insurance is only for older people. | Buying younger often results in lower premiums. |

| Single people never need life insurance. | Some singles use coverage for debts, parents, or future planning. |

| Employer coverage is always enough. | Employer coverage may be limited and can disappear when you leave your job. |

| Whole life insurance is always better. | The best option depends on your financial goals and situation. |

| Term insurance is a waste of money. | Term insurance provides valuable protection during critical years. |

| Life insurance is too expensive. | Many healthy adults can obtain affordable coverage. |

| Stay-at-home parents don’t need insurance. | Replacing childcare and household services can be costly. |

| Young adults should wait before buying coverage. | Waiting often results in higher premiums later. |

| Cash value growth makes whole life a great investment. | Cash value growth should be evaluated against other financial alternatives. |

| Once you buy insurance, you never need to review it. | Life changes may require policy updates and coverage adjustments. |

Why These Myths Matter

Believing the wrong information can lead to: Term Life Insurance vs Whole Life Insurance

- Underinsurance

- Overpaying for coverage

- Delayed financial planning

- Increased risk for loved ones

Making decisions based on facts rather than sales pitches is one of the smartest moves any insurance buyer can make.

Which Policy Is Best for Different Age Groups?

There is no universal answer to the term life vs whole life insurance debate.

The best choice often depends on your stage of life, financial obligations, and long-term objectives.

Ages 20–30

People in their twenties and early thirties are often:

- Starting careers

- Paying student loans

- Buying first homes

- Starting families

At this stage, affordability usually matters most.

Recommended Option

Term Life Insurance

Reasons:

- Lower premiums

- Maximum coverage for minimal cost

- Ability to lock in low rates while healthy

- Greater financial flexibility

For example, a healthy 28-year-old may secure substantial coverage at a fraction of the cost of a whole life policy.

Ages 30–40

This period is often associated with peak family responsibilities.

Common obligations include:

- Raising children

- Mortgage payments

- Income replacement needs

- College savings goals

Recommended Option

Term Life Insurance for Most Families

Many financial professionals recommend coverage that lasts until:

- Children become financially independent

- Major debts are paid off

- Retirement savings become established

However, some individuals with advanced estate planning goals may begin exploring permanent coverage options during this stage.

Ages 40–50

Financial situations become more diverse during these years.

Some people are:

- Nearing retirement planning

- Growing investment portfolios

- Building business assets

- Considering wealth transfer strategies

Recommended Option

Depends on Financial Goals

Term insurance may still make sense for:

- Income replacement

- Remaining mortgage obligations

- Family protection

Whole life insurance may become more attractive for:

- Estate planning

- Long-term legacy objectives

- Individuals seeking permanent coverage

This is often the age range where a personalized analysis becomes particularly important.

Final Thoughts

The debate between term life insurance and whole life insurance has been going on for decades, but the truth is that there is no one-size-fits-all answer.

The right choice depends on your financial situation, family responsibilities, long-term goals, and budget.

For most families in 2026, term life insurance remains the most practical and cost-effective option. It provides substantial coverage at an affordable price, allowing parents, homeowners, and working professionals to protect their loved ones without straining their finances.

One of the biggest mistakes people make is buying a policy they don’t fully understand. Life insurance is too important to purchase based solely on marketing promises, sales presentations, or recommendations from friends and family.

Instead, focus on the questions that matter most: Term Life Insurance vs Whole Life Insurance

- Who depends on your income?

- How much debt would your family inherit?

- How long would your loved ones need financial support?

- What are your long-term financial goals?

- Can you comfortably afford the premiums for decades?

The best life insurance policy is not necessarily the most expensive one or the one with the most features. It is the policy that provides the right amount of protection at a price that fits your financial plan.

Before making a decision, compare multiple quotes, review policy details carefully, and consider speaking with an independent financial professional who can explain your options objectively. Term Life Insurance vs Whole Life Insurance

A few hours of research today could save your family thousands of dollars and provide decades of peace of mind. Choose wisely, review your coverage regularly, and make sure your life insurance strategy continues to support your financial goals as your life evolves.