Personal Loan vs Credit Card: Managing money effectively has become increasingly important in 2026. Whether individuals need funds for emergencies, medical expenses, travel costs, home improvements, debt consolidation, or large purchases, two common borrowing options often appear: personal loans and credit cards.

Both options provide access to money, but they operate differently and serve different financial purposes.

Many people ask:

- Is a personal loan better than a credit card?

- Which option has lower interest rates?

- Which helps build credit?

- Which works better for large expenses?

- Which option saves more money?

Understanding the differences between a personal loan and a credit card can help people make better financial decisions.

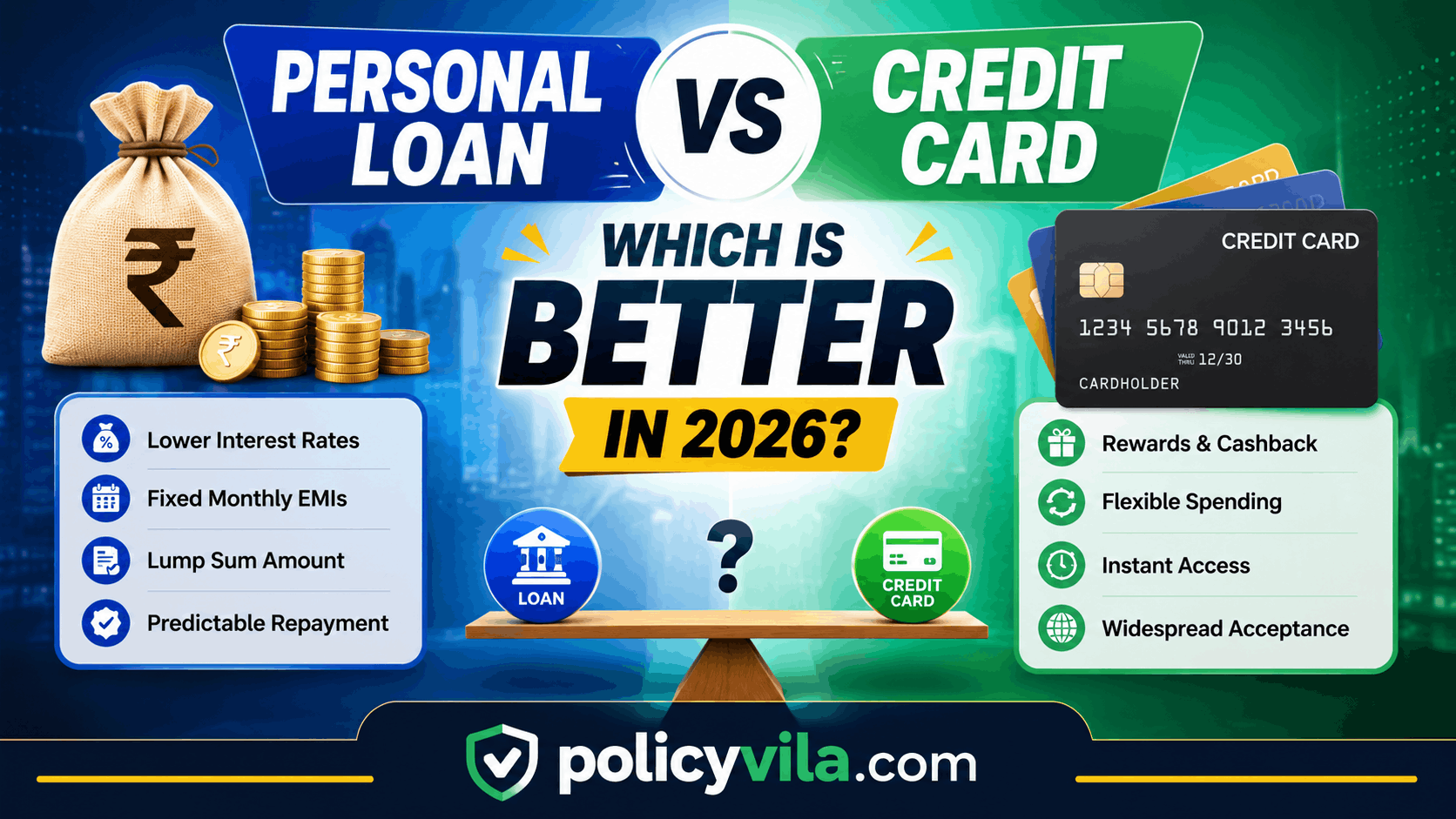

What Is a Personal Loan?

A personal loan is an installment-based borrowing option where a lender provides a fixed amount of money that must be repaid over a specific period.

Personal loans usually include:

- Fixed loan amount

- Monthly payments

- Interest charges

- Defined repayment periods

People commonly use personal loans for:

- Home improvements

- Medical expenses

- Debt consolidation

- Weddings

- Education expenses

- Emergency situations

What Is a Credit Card?

A credit card provides revolving credit that allows users to borrow money repeatedly up to a certain limit.

Unlike personal loans, credit cards remain available after repayments are made.

People commonly use credit cards for:

- Shopping

- Travel expenses

- Utility payments

- Emergency spending

- Online purchases

Personal Loan vs Credit Card Eligibility Requirements in 2026

Several important differences exist between these financial products.

Personal Loan vs Credit Card Interest Rates

Interest rates significantly affect total borrowing costs.

Personal loans often offer:

- Fixed interest rates

- Lower borrowing costs for qualified borrowers

- Predictable payment structures

Credit cards may include:

- Variable interest rates

- Higher borrowing costs

- Penalty rates in certain situations

Borrowers with stronger credit histories may qualify for more favorable terms.

Personal Loan vs Credit Card Monthly Payments

Payment structures differ significantly.

Personal loans typically provide:

- Fixed monthly payments

- Predictable repayment schedules

- Defined payoff periods

Credit cards usually provide:

- Minimum payment options

- Flexible payments

- Variable balances

Personal Loan vs Credit Card Repayment Terms

Personal loans often include repayment periods such as:

- One year

- Three years

- Five years

- Seven years

Credit cards usually continue indefinitely unless balances are fully paid.

Personal Loan vs Credit Card Approval Process

Approval requirements vary.

Lenders commonly review:

- Credit scores

- Income levels

- Employment history

- Existing debt

Some credit cards may have simpler application processes.

Personal Loan vs Credit Card: Benefits of Personal Loans

Personal loans provide several advantages.

Why Personal Loans Can Be Better for Large Expenses

Personal loans frequently work well for major financial needs.

Examples include:

- Medical bills

- Home renovations

- Vehicle repairs

- Education costs

Fixed payments can simplify budgeting.

Personal Loan Benefits for Debt Consolidation

Many borrowers combine multiple debts into a single loan.

Potential advantages include:

- One monthly payment

- Lower interest costs

- Better organization

- Easier financial management

Personal Loan vs Credit Card: Benefits of Credit Cards

Credit cards also provide useful benefits.

Credit Card Rewards and Cashback Benefits

Some credit cards offer rewards programs.

Examples include:

- Cashback rewards

- Travel points

- Airline miles

- Shopping benefits

Credit Card Flexibility for Everyday Spending

Credit cards allow ongoing spending flexibility.

Common uses include:

- Groceries

- Fuel expenses

- Online shopping

- Daily purchases

Personal Loan vs Credit Card for Emergencies

Unexpected expenses can happen at any time.

Examples include:

- Medical emergencies

- Home repairs

- Car maintenance

- Travel disruptions

Credit cards may provide immediate access to funds.

Personal loans may offer lower borrowing costs for larger expenses.

Personal Loan vs Credit Card for Medical Expenses

Healthcare costs sometimes create financial pressure.

Personal loans may work well for:

- Scheduled procedures

- Large medical expenses

Credit cards may provide faster payment access.

Personal Loan vs Credit Card for Travel Expenses

Travel costs may include:

- Flights

- Hotels

- Transportation

- Emergency expenses

Many travel credit cards provide additional benefits.

Personal Loan vs Credit Card for Credit Score Impact

Borrowing decisions may influence credit scores.

Important factors include:

- Payment history

- Credit utilization

- Debt balances

- Account age

Making payments on time remains important for maintaining healthy credit profiles.

Personal Loan vs Credit Card for Debt Consolidation

Debt consolidation remains a common reason for borrowing.

Possible benefits include:

- Simplified payments

- Lower stress

- Better organization

- Potential interest savings

Many individuals use personal loans for debt consolidation purposes.

Personal Loan vs Credit Card: Common Borrowing Mistakes

Financial mistakes can increase costs.

Borrowing More Than Necessary

Higher borrowing amounts increase repayment obligations.

Ignoring Total Interest Costs

Borrowers sometimes focus only on monthly payments instead of total costs.

Missing Payment Deadlines

Late payments may create:

- Extra fees

- Credit score impact

- Increased financial stress

Not Reviewing Terms Carefully

Borrowers should review:

- Interest rates

- Fees

- Conditions

- Repayment requirements

Personal Loan vs Credit Card: Which Is Better in 2026?

The answer depends on financial goals.

A personal loan may work better for:

- Large planned expenses

- Debt consolidation

- Fixed repayment schedules

A credit card may work better for:

- Small purchases

- Flexible spending

- Reward opportunities

- Short-term expenses

Personal Loan vs Credit Card: Cost Comparison in 2026

Understanding the total borrowing cost is important before choosing between a personal loan and a credit card. Many borrowers focus only on monthly payments and ignore overall repayment amounts.

Several factors influence total costs:

- Interest rates

- Processing fees

- Late payment fees

- Annual charges

- Repayment periods

Even a small difference in interest rates may significantly affect long-term costs.

Personal Loan vs Credit Card Processing Fees

Personal loans sometimes include fees such as:

- Origination fees

- Processing fees

- Late payment charges

- Prepayment fees in some cases

Credit cards may include:

- Annual fees

- Cash advance fees

- Foreign transaction fees

- Late payment fees

Borrowers should review all charges before applying.

Personal Loan vs Credit Card for Short-Term Borrowing

Short-term borrowing usually involves smaller expenses that can be repaid quickly.

Examples include:

- Emergency purchases

- Travel bookings

- Small repairs

- Temporary cash needs

Credit cards may work well for short-term borrowing because of flexibility and rewards programs.

Some users pay the full balance monthly to avoid additional interest charges.

Personal Loan vs Credit Card for Long-Term Borrowing

Long-term borrowing generally involves larger amounts.

Examples include:

- Home renovation projects

- Debt consolidation

- Medical expenses

- Education costs

Personal loans often provide:

- Fixed repayment schedules

- Structured monthly payments

- Defined loan periods

Many borrowers prefer predictable payment structures.

Personal Loan vs Credit Card for Building Credit History

Credit history remains important for future financial opportunities.

Examples include:

- Mortgage applications

- Vehicle financing

- Future loans

- Rental applications

Responsible borrowing behavior may help improve credit profiles.

Good practices include:

- Making payments on time

- Maintaining manageable debt levels

- Avoiding excessive borrowing

- Monitoring credit activity

Personal Loan vs Credit Card and Financial Discipline

Financial behavior influences borrowing outcomes.

Personal loans may encourage discipline because:

- Payments are fixed

- Loan amounts are limited

- Repayment timelines are clear

Credit cards may require stronger self-control because spending remains continuously available.

Some individuals find ongoing credit access challenging to manage.

Personal Loan vs Credit Card for Online Shopping

Online shopping continues increasing in popularity.

Credit cards often provide benefits such as:

- Fraud protection

- Rewards programs

- Purchase security

- Convenience

Personal loans generally are not commonly used for small online purchases.

Personal Loan vs Credit Card for Home Improvements

Home projects can become expensive.

Examples include:

- Furniture purchases

- Kitchen renovations

- Appliance upgrades

- Repair work

Personal loans may provide structured financing for larger projects.

Personal Loan vs Credit Card for Unexpected Expenses

Unexpected expenses can occur without warning.

Examples include:

- Emergency medical situations

- Vehicle repairs

- Urgent travel needs

- Household repairs

Choosing the right option often depends on:

- Amount needed

- Urgency

- Repayment ability

- Interest costs

Future Trends in Personal Loans and Credit Cards

Financial services continue evolving rapidly in 2026.

Emerging trends include:

AI-Based Lending Systems

Artificial intelligence increasingly helps lenders:

- Evaluate risk

- Improve approval speed

- Personalize offers

Digital Banking Expansion

Digital platforms continue simplifying financial services.

Benefits may include:

- Faster applications

- Online account management

- Instant notifications

- Mobile accessibility

Increased Personalization

Financial products increasingly adapt to user behavior and preferences.

Eligibility Requirements for Borrowing in 2026

Approval requirements can vary among lenders and financial institutions. Understanding these requirements before submitting an application may increase approval chances.

Common factors lenders often review include:

- Credit score

- Income level

- Employment status

- Existing financial obligations

- Borrowing history

Applicants with stronger credit profiles may sometimes qualify for more favorable terms and lower interest rates.

Financing Options for Self-Employed Individuals

Self-employed individuals may experience a different application process because income can vary from month to month.

Common documents requested may include:

- Tax returns

- Income statements

- Bank records

- Business-related documents

Installment loans sometimes require more extensive verification, while certain card applications may involve a simpler review process.

Financial Solutions for Students

Students often seek financial support for expenses such as:

- Education materials

- Daily living costs

- Transportation expenses

- Unexpected situations

Student-focused credit products sometimes include lower limits and educational tools that help build responsible financial habits.

Loan opportunities may also be available depending on eligibility requirements.

Borrowing Considerations for Families

Families often manage multiple financial responsibilities.

Common household expenses may include:

- Healthcare costs

- Children’s education

- Utility bills

- Home maintenance expenses

Choosing the right financing method often depends on the amount needed and repayment preferences.

Managing Business-Related Expenses

Small business owners occasionally use financial products for operational needs.

Examples include:

- Equipment purchases

- Marketing activities

- Inventory management

- Day-to-day expenses

Flexible payment options may work for recurring expenses, while larger funding needs sometimes require structured repayment solutions.

Financial Planning and Responsible Borrowing

Long-term financial planning becomes easier when individuals understand future repayment responsibilities.

Important considerations include:

Monthly Budget Planning

Monthly obligations should fit comfortably within available income.

Emergency Savings Goals

Savings may reduce dependence on borrowed funds during unexpected situations.

Debt Management Strategy

Maintaining manageable debt levels may support long-term financial health.

Future Financial Objectives

Examples may include:

- Purchasing a home

- Starting a business

- Funding education

- Retirement preparation

Financial decisions made today can influence future opportunities.

Common Mistakes First-Time Borrowers Make

People applying for financing for the first time sometimes make avoidable mistakes.

Submitting Too Many Applications

Applying for several products at once may create unnecessary complications.

Ignoring Repayment Ability

Borrowing more than can comfortably be repaid may increase financial stress.

Using Borrowed Funds Unnecessarily

Borrowed money should ideally be used carefully and for important needs.

Missing Additional Costs

Some individuals focus only on interest rates while overlooking fees and other charges.

Smart Tips Before Choosing a Financing Option

People can improve financial decisions through responsible practices.

Compare Multiple Offers

Different lenders and providers may offer different terms.

Understand the Full Agreement

Review:

- Interest rates

- Fees

- Repayment schedules

- Terms and conditions

Maintain Healthy Credit Habits

Responsible financial behavior may help support future borrowing opportunities.

Borrow Only What You Need

Limiting unnecessary debt may help reduce financial pressure over time.

Comparing Short-Term and Long-Term Borrowing Needs

Choosing the right financing option often depends on how long the money is needed and the amount being borrowed.

Short-term borrowing commonly includes:

- Emergency purchases

- Travel costs

- Monthly expenses

- Temporary cash needs

Long-term borrowing may include:

- Home improvement projects

- Education expenses

- Medical procedures

- Debt consolidation plans

Short-term expenses often require flexibility, while larger long-term costs may benefit from structured repayment plans.

Factors That Affect Approval Chances

Approval decisions vary among financial institutions, but several common factors usually influence the process.

Credit History

Credit history shows previous borrowing behavior and payment patterns.

Lenders may review:

- On-time payment history

- Existing debt levels

- Credit utilization

- Account history

Maintaining responsible financial habits may improve approval opportunities.

Income Stability

Stable income often provides confidence regarding repayment ability.

Examples of income sources include:

- Employment salary

- Business income

- Freelance earnings

- Additional income sources

Existing Financial Commitments

Current obligations may affect borrowing eligibility.

Examples include:

- Home loans

- Vehicle loans

- Existing balances

- Monthly obligations

Lower debt levels may improve financial flexibility.

Benefits of Responsible Financial Management

Good financial habits may create long-term advantages.

Potential benefits include:

- Better credit opportunities

- Lower borrowing costs

- Improved financial stability

- Easier future approvals

- Reduced financial stress

Small financial decisions made consistently over time may have a significant impact.

Building Better Money Habits

Healthy financial practices often support long-term success.

Helpful habits may include:

Tracking Monthly Spending

Understanding spending patterns may help identify unnecessary expenses.

Creating a Budget Plan

Budgeting can help individuals:

- Manage expenses

- Increase savings

- Reduce debt pressure

- Improve financial control

Building Emergency Funds

Emergency savings may help reduce dependence on borrowing during unexpected situations.

Financial experts often recommend maintaining emergency funds for unexpected expenses.

Paying Bills on Time

Timely payments may support healthy financial records and reduce additional charges.

Future Trends in Consumer Finance in 2026

Financial technology continues changing rapidly.

Emerging trends may include:

AI-Powered Financial Services

Artificial intelligence increasingly assists with:

- Personalized recommendations

- Risk assessment

- faster application reviews

- financial management tools

Digital Banking Growth

Digital platforms continue expanding because of convenience and accessibility.

Potential benefits include:

- Faster approval processes

- Mobile account access

- Instant notifications

- Improved customer experiences

Personalized Financial Products

Financial institutions increasingly tailor products based on individual user behavior and needs.

Understanding Financial Needs Before Borrowing

Before applying for any type of financing, understanding the actual purpose behind borrowing money is important. Many people apply for financial products without fully evaluating whether the expense is essential, temporary, or long-term.

Questions that may help before making a decision include:

- Why is the money needed?

- How much money is actually required?

- How quickly can repayment happen?

- Will monthly payments fit comfortably within the budget?

- Are there alternative funding options available?

Answering these questions may reduce unnecessary borrowing and support better financial decisions.

read also: Best Travel Insurance Cancellation Policy 2026

Creating a Long-Term Financial Strategy

Financial products should not only solve immediate problems but should also align with future goals.

Long-term financial planning may involve:

- Building savings accounts

- Reducing debt levels

- Improving credit history

- Planning retirement goals

- Preparing for education expenses

- Investing for future growth

Many individuals focus only on immediate needs and overlook long-term consequences.

A structured financial strategy may create stronger financial stability over time.

Understanding Interest and Total Borrowing Costs

Many borrowers pay attention only to monthly payment amounts. However, understanding total borrowing cost may be equally important.

Total repayment amounts may include:

- Interest charges

- Processing fees

- Annual fees

- Late payment penalties

- Additional service charges

For example, two financial products may appear similar because they offer comparable monthly payments. However, one option may result in significantly higher total repayment costs over several years.

Carefully reviewing the complete cost structure before applying can help avoid unexpected financial pressure.

Why Financial Discipline Matters

Access to borrowing can be helpful, but financial discipline often determines whether borrowing becomes useful or problematic.

Strong financial habits may include:

- Spending according to a budget

- Avoiding impulse purchases

- Paying obligations on time

- Reviewing account activity regularly

- Saving money consistently

Without financial discipline, borrowing may gradually create larger financial challenges.

Developing healthy money habits often supports long-term financial success.

Understanding Debt-to-Income Ratio

Debt-to-income ratio is commonly used by lenders when evaluating applications.

This ratio compares:

Monthly debt obligations ÷ Monthly income

Lower ratios often indicate:

- Better financial balance

- Lower borrowing risk

- Greater repayment capacity

Higher ratios sometimes indicate:

- Increased financial pressure

- Higher risk levels

- Limited repayment flexibility

Managing existing obligations carefully may help maintain healthier financial profiles.

Building Strong Financial Habits for Future Success

Financial success often results from consistent habits rather than one major decision.

Helpful habits may include:

Regular Expense Tracking

Monitoring spending may reveal areas where money can be managed more efficiently.

Tracking may include:

- Daily spending

- Household expenses

- Subscription costs

- Transportation expenses

- Entertainment spending

Setting Financial Goals

Goals help create direction and motivation.

Examples include:

- Saving for a house

- Starting a business

- Paying off debt

- Creating emergency savings

- Investing for retirement

Clear goals often improve financial decision-making.

Maintaining Emergency Savings

Unexpected situations can occur without warning.

Examples include:

- Medical emergencies

- Vehicle repairs

- Job changes

- Household repairs

- Family emergencies

Emergency savings may reduce dependence on borrowing during difficult situations.

Reviewing Financial Progress

Regular reviews may help identify:

- Spending patterns

- Debt changes

- Savings growth

- Financial opportunities

Small adjustments over time may create meaningful long-term improvements.

How Technology Is Changing Consumer Finance

Technology continues transforming financial services in 2026.

Several innovations are becoming increasingly common.

Artificial Intelligence in Lending

AI systems increasingly assist financial institutions with:

- Application reviews

- Risk assessment

- Personalized recommendations

- Fraud detection

- Customer support

These systems may improve speed and efficiency.

Mobile Banking Growth

Mobile banking continues expanding globally.

Advantages may include:

- Instant account access

- Payment management

- Spending alerts

- Financial tracking tools

- Digital applications

Consumers increasingly prefer managing finances directly through smartphones.

Improved Security Systems

Financial institutions continue investing in security technologies.

Examples include:

- Biometric authentication

- Fraud monitoring systems

- Multi-factor verification

- Real-time transaction alerts

Security improvements may help protect users from financial risks.

Financial Mistakes That Can Affect Long-Term Stability

Certain financial mistakes may create long-term challenges.

Common examples include:

Spending Beyond Income Levels

Consistently spending more than earned may create financial stress.

Ignoring Savings Goals

Savings often provide protection during unexpected situations.

Missing Payment Deadlines

Late payments may sometimes result in:

- Additional charges

- Reduced financial flexibility

- Lower credit strength

How Financial Decisions Affect Future Opportunities

Many people think borrowing decisions only affect current expenses. However, financial choices made today can influence opportunities for years.

Financial behavior may affect:

- Future loan approvals

- Housing opportunities

- Business financing options

- Investment capabilities

- Credit access

- Overall financial flexibility

Responsible financial management often creates greater opportunities in the future.

For example, maintaining healthy financial records and making timely payments may improve access to better financial products later.

Understanding the Psychology of Spending

Money decisions are not always based entirely on logic. Emotions and behavior frequently influence spending patterns.

Common spending triggers include:

- Stress spending

- Impulse buying

- Social influence

- Lifestyle pressure

- Seasonal shopping habits

Recognizing these patterns may help individuals make better financial decisions.

For example, some people make large purchases because of temporary emotions rather than actual needs.

Understanding personal spending behavior may reduce unnecessary expenses.

The Importance of Emergency Financial Planning

Unexpected situations can happen without warning.

Examples include:

- Sudden medical expenses

- Job changes

- Vehicle breakdowns

- Home repairs

- Family emergencies

Emergency planning may reduce financial stress during difficult periods.

Steps that may help include:

Creating an Emergency Fund

Many people gradually build savings over time.

Savings goals vary among individuals, but consistent contributions may create financial security.

Reducing Unnecessary Expenses

Identifying avoidable spending areas may improve financial flexibility.

Examples may include:

- Unused subscriptions

- Excessive entertainment spending

- Unplanned purchases

Maintaining Financial Records

Keeping organized financial information may simplify planning.

Examples include:

- Income details

- Expense tracking

- Account information

- Payment schedules

Financial Education and Long-Term Success

Financial knowledge plays an important role in making informed decisions.

Areas that people frequently learn about include:

- Budget planning

- Debt management

- Savings strategies

- Investment basics

- Financial risk awareness

Greater understanding often improves confidence and decision-making.

Developing Better Budgeting Habits

Budgeting does not necessarily mean eliminating all spending. Instead, budgeting helps create awareness and control.

Basic budgeting approaches may include:

Fixed Expense Planning

Examples include:

- Rent or housing costs

- Utility payments

- Insurance expenses

- Transportation costs

Variable Expense Management

Examples include:

- Entertainment spending

- Dining expenses

- Shopping purchases

- Travel costs

Savings Allocation

Many people reserve a portion of income for:

- Emergency savings

- Future goals

- Investments

- Retirement planning

Building Financial Confidence Over Time

Financial confidence often develops gradually.

Helpful actions may include:

- Tracking financial progress

- Learning new financial concepts

- Reviewing spending habits

- Setting realistic goals

- Making informed decisions

Small improvements made consistently over time may create meaningful long-term results.

read also: Best Group Life Insurance Policies Are Generally Written As 2026

Final Thoughts on

Choosing between a personal loan and a credit card in 2026 requires understanding financial goals, spending habits, and repayment abilities.

Personal loans generally offer predictable payments and structured borrowing, while credit cards provide flexibility and convenience.

Evaluating interest rates, fees, repayment periods, and long-term costs can help borrowers choose the option that best fits their financial situation and supports better money management decisions.