Health Insurance Deductibles Explained: Health insurance can seem confusing, especially when you’re trying to compare plans and protect your family’s finances. In 2026, understanding how Health Insurance Deductibles Explained works is more important than ever. Medical costs continue to rise, families have more coverage options to choose from, and many consumers are still unsure about one of the most important parts of a health plan: the deductible.

The deductible can have a significant impact on how much you pay for health care throughout the year. Yet many people focus only on the monthly premium and ignore how the deductible affects their total health care costs.

If you’ve ever wondered why two health insurance plans have very different prices or why some medical bills seem higher than expected, understanding the deductible can help you make smarter decisions.

This guide explains everything families need to know about health insurance deductibles in simple, practical language.

What Is a Health Insurance Deductible?

A health insurance deductible is the amount you have to pay for covered healthcare services before the insurance company starts sharing the cost.

Think of it as your contribution to medical expenses each year.

For example, if your Health Insurance Deductibles Explained plan has a $2,000 deductible, you are typically required to pay the first $2,000 of eligible medical expenses before your insurance starts paying a portion of your costs.

Many families confuse deductibles with premiums, but they are not the same thing.

- Premium: The monthly amount you pay to keep your insurance active.

- Deductible: The amount you pay for healthcare services before insurance cost-sharing begins.

A Simple Family Example

Imagine a family purchases a health insurance plan with a $3,000 deductible.

During the year:

- A child needs urgent care treatment costing $500.

- One parent visits specialists and receives tests costing $1,000.

- Another family member requires outpatient surgery costing $2,000.

The family pays the first $3,000 for these covered services. After the deductible is met, the insurance company begins to cover its portion according to the plan’s rules.

This system helps insurers manage risk while encouraging consumers to use healthcare services responsibly.

Why Deductibles Matter More in 2026

Health care decisions are becoming increasingly complex.

Several trends make deductibles especially important for families today.

Rising Medical Costs

Health care costs have steadily increased over time. Hospital visits, diagnostic tests, specialist visits, and prescription drugs can add up quickly.

What seemed like a deductible a few years ago looks very different today.

Family Budget Pressures

Many families are balancing high housing costs, child care costs, transportation costs, and inflation-related expenses.

Unexpected healthcare bills can put a significant strain on a family budget.

More Insurance Choices

Consumers can now take advantage of a variety of Health Insurance Deductibles Explained plans.

While more options can be beneficial, they can also create confusion when comparing deductibles, premiums, and coverage levels.

Emergency Healthcare Risks

No family expects a medical emergency, but accidents and unexpected illnesses happen.

An incorrectly chosen deductible amount can lead to large expenses in difficult situations.

Increased Focus on Preventive Care

Many plans encourage preventive care services, but it’s important to understand what’s covered before you hit the deductible.

Choosing the wrong deductible isn’t just an insurance mistake—it can be a financial challenge that affects your entire year.

How Health Insurance Deductibles Work

Let’s walk through the process step by step.

Step 1: Healthcare Services Are Received

A family member visits a doctor, receives treatment, or undergoes testing.

Step 2: Bills Apply Toward the Deductible

If the service is subject to the deductible, the family pays the negotiated insurance rate until the deductible is reached.

Step 3: Deductible Is Met

Once total eligible healthcare expenses equal the deductible amount, the plan enters the next phase.

Step 4: Insurance Begins Sharing Costs

After meeting the deductible, the insurance company usually pays a portion of covered expenses while the patient pays coinsurance or copayments.

Step 5: Out-of-Pocket Maximum Protection

Eventually, if expenses continue to rise, the family may reach the plan’s out-of-pocket maximum.

At that point, the insurance company generally covers most or all remaining covered costs for the year.

Real-Life Example

Consider a family with a $4,000 deductible.

During the year:

- Doctor visits: $600

- Diagnostic tests: $1,200

- Emergency room visit: $2,200

Total expenses reach $4,000.

After reaching that threshold, insurance begins paying according to the plan’s cost-sharing rules.

Without understanding the deductible beforehand, those expenses could come as an unpleasant surprise.

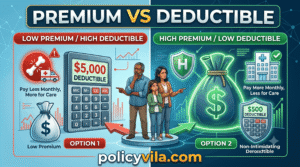

Deductible vs Premium: Understanding the Difference

One of the most common insurance questions involves understanding the relationship between premiums and deductibles.

What Is a Premium?

A premium is the monthly payment you make to maintain Health Insurance Deductibles Explained coverage.

Whether you use healthcare services or not, you must pay the premium.

What Is a Deductible?

A deductible is the amount you pay for covered healthcare services before insurance starts sharing costs.

Lower Premium, Higher Deductible

Some plans offer lower monthly premiums but require higher deductibles.

Example:

- Monthly premium: $300

- Deductible: $6,000

These plans may work well for healthy individuals who rarely need medical care.

Higher Premium, Lower Deductible

Other plans charge higher monthly premiums but reduce out-of-pocket costs when care is needed.

Example:

- Monthly premium: $650

- Deductible: $1,000

These plans may benefit families expecting regular healthcare expenses.

Which Is Better?

There is no universal answer.

The best choice depends on:

- Health conditions

- Family size

- Medical history

- Budget

- Emergency savings

Looking only at monthly premiums can lead to costly mistakes.

Individual vs Family Deductibles

Family Health Insurance Deductibles Explained plans often contain both individual and family deductibles.

Individual Deductible

This applies to each covered person separately.

When one family member reaches their individual deductible, insurance begins sharing costs for that person.

Family Deductible

This applies to the combined medical expenses of everyone covered under the plan.

Once the family deductible is reached, insurance begins sharing costs for all covered family members.

Example

A family of four has:

- Individual deductible: $2,000

- Family deductible: $6,000

One parent incurs a medical expense of $2,000 and reaches the individual deductible.

Insurance begins to share the cost for that parent.

The entire family continues to accumulate costs until the total reaches $6,000.

Understanding this distinction can avoid confusion when multiple family members receive care during the same year.

Common Health Insurance Terms Related to Deductibles

Copayment (Copay)

A fixed amount paid for certain services.

Examples:

- $25 doctor visit

- $50 specialist visit

Coinsurance

The percentage of costs you pay after meeting your deductible.

Example:

- Insurance pays 80%

- You pay 20%

Out-of-Pocket Maximum

The highest amount you’ll pay for covered healthcare services during the year.

After reaching this limit, insurance generally covers most additional costs.

Network Providers

Doctors, hospitals, and specialists contracted with your insurance company.

Using in-network providers often reduces costs.

Preventive Care Benefits

Many preventive services may be covered without requiring you to meet the deductible first.

Examples include:

- Annual wellness exams

- Vaccinations

- Certain screenings

These benefits encourage early detection and preventive healthcare.

High-Deductible Health Plans: Pros and Cons

High-deductible health plans have become increasingly common.

Advantages

Lower Monthly Premiums

Families often pay less each month for coverage.

Potential Savings

Healthy families who rarely need medical care may spend less overall.

Access to Health Savings Opportunities

Some plans allow additional tax-advantaged healthcare savings options.

Disadvantages

Higher Upfront Costs

Unexpected medical events can result in large bills before insurance begins sharing expenses.

Greater Financial Risk

A serious illness or accident may quickly create significant out-of-pocket spending.

Budget Challenges

Families without emergency savings may struggle to handle large deductibles.

Who Might Benefit?

High deductible plans may work well for the following people:

Healthy adults

Families with strong emergency funds

People who rarely need medical care

They may be less suitable for:

Families with chronic health problems

Individuals who need frequent care

Families with limited savings

How Families Can Choose the Right Deductible

Selecting the right deductible requires balancing risk and affordability.

Consider these factors:

Family Size

Larger families generally use more healthcare services.

Medical History

Review healthcare usage from previous years.

Prescription Medication Needs

Regular prescriptions can significantly influence healthcare spending.

Emergency Savings

Can your family comfortably handle a large deductible if needed?

Doctor Visits

Frequent appointments may favor lower-deductible plans.

Planned Procedures

Expected surgeries or treatment plan choices influence the choice.

Rather than focusing solely on premiums, estimate your total annual healthcare costs under different scenarios.

Common Deductible Mistakes Families Make

Many consumers make avoidable mistakes when selecting coverage.

Choosing Based Only on Premiums

A cheap premium can hide expensive out-of-pocket costs.

Ignoring Total Annual Expenses

Evaluate overall healthcare spending, not just monthly costs.

Underestimating Healthcare Usage

Families often use more medical services than expected.

Misunderstanding Coinsurance

Meeting the deductible does not always mean healthcare becomes free.

Forgetting Plan Reviews

Health needs change from year to year.

Review your coverage annually during the enrollment period.

Avoiding these mistakes can save you significant money and reduce stress.

Questions to Ask Before Choosing a Health Insurance Plan

Use this checklist when comparing options:

What is the deductible?

What services are covered before the deductible is met?

What is the maximum out-of-pocket cost?

Are my preferred doctors in-network?

What prescription drug costs should I expect?

How much does an emergency room visit cost?

What are the costs of a specialist visit?

How much can I realistically spend during a difficult medical year?

Does this plan meet my family’s healthcare needs?

What preventive services are covered?

These questions can reveal differences that aren’t obvious at first glance.

Health Insurance Trends Families Should Watch in 2026

Healthcare is constantly evolving.

Digital Healthcare Services

Virtual healthcare options continue to expand.

Telehealth Growth

Many families now rely on telehealth for convenience and accessibility.

Preventive Care Initiatives

Insurance companies are increasingly emphasizing preventive health programs.

Healthcare Cost Transparency

Consumers have more tools available to compare costs before seeking treatment.

Customer-Focused Technology

Insurance apps and online tools help families track costs, deductibles, and claims more easily.

Staying informed about these developments can improve healthcare decision-making.

read also: Credit Score Secrets Banks Don’t Want You to Know in 2026

Conclusion

One of the most important steps families can take when choosing coverage in 2026 is understanding health insurance deductibles.

While deductibles may seem confusing at first, they play a key role in determining how much you’ll ultimately spend on health care throughout the year.

The smartest approach is to look beyond the monthly premium and consider your family’s overall health care needs, financial situation, and potential medical expenses. The plan with the lowest premium is not always the cheapest option when it comes to health care services.

By carefully comparing plans, understanding key insurance terms, and realistically assessing health care costs, families can make confident decisions that provide both financial security and peace of mind. Taking the time to understand deductibles today can help prevent costly surprises tomorrow.