Introduction

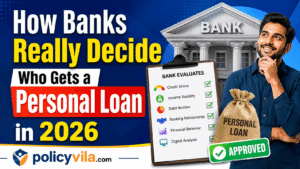

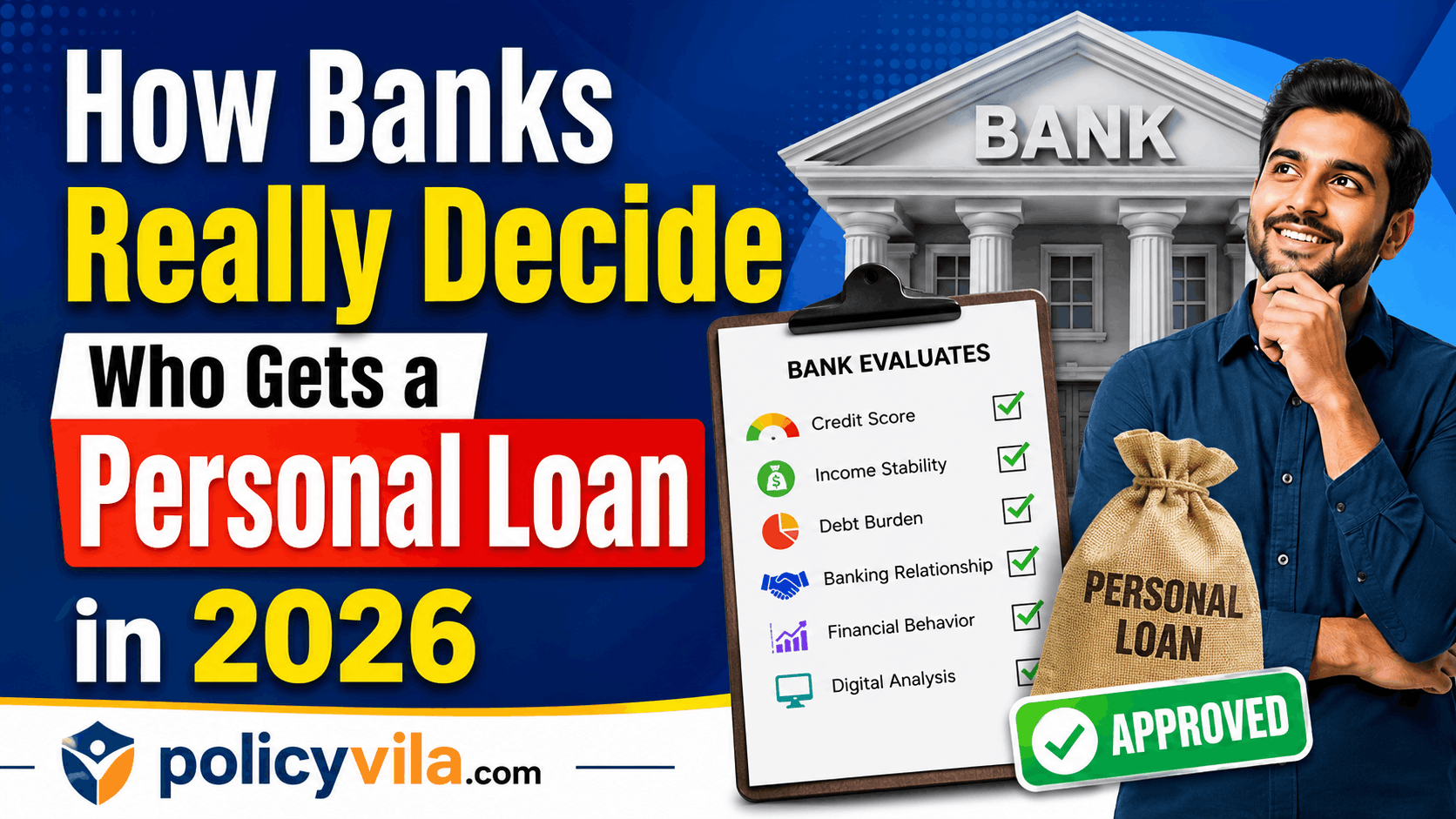

How Banks Really Decide Who Gets a Personal Loan in 2026 Applying for a personal loan in 2026 is easier than ever before. Most banks now offer digital applications, instant document uploads, and faster approval decisions. However, many borrowers are surprised when their loan application is rejected despite having a decent income and a good financial background.

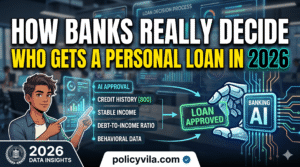

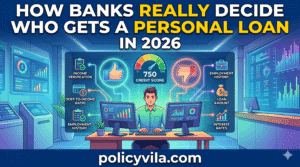

The reason is simple: banks do not approve personal loans based on income alone. Instead, lenders use sophisticated risk assessment systems, behavioral analysis tools, and financial scoring models to determine whether an applicant qualifies for credit.

While advertisements often focus on quick approvals and simple applications, the actual decision-making process is much more detailed. Banks evaluate dozens of factors before deciding whether an applicant represents a low-risk or high-risk borrower.

Understanding how banks make these decisions can significantly improve your chances of approval. Moreover, it can help you build a stronger financial profile and qualify for better borrowing terms in the future.

This guide explains how banks really decide who gets a personal loan in 2026, including the hidden factors, approval criteria, and financial behaviors that influence lending decisions.

Understanding Personal Loan Approval in 2026

The First Thing Banks Check: Credit Score

Why Credit Behavior Matters More Than Credit Score

Many borrowers believe that a high credit score automatically guarantees personal loan approval. While a strong credit score is certainly important, banks in 2026 often place even greater emphasis on credit behavior. This is because a credit score provides only a snapshot of your financial profile, whereas credit behavior reveals how you manage debt and financial responsibilities over time.

Modern lenders want to understand not only your current score but also the habits that helped create it. As a result, they carefully review your borrowing patterns, repayment consistency, and overall financial discipline before making a decision.

Some of the key credit behavior factors banks analyze include:

- Timely repayment of loans and credit card bills

- Frequency of missed or late payments

- Credit card utilization levels

- Length of credit history

- Number of recent loan or credit applications

- Consistency in managing financial obligations

For example, two borrowers may have similar credit scores, but their approval chances can differ significantly. One applicant may have a long history of on-time payments and responsible credit usage, while the other may have recently improved their score after previous financial difficulties. In such cases, lenders often view the first borrower as less risky.

Furthermore, banks use advanced risk assessment systems that can identify patterns in financial behavior. Frequent late payments, excessive borrowing, or sudden increases in debt may raise concerns, even if the overall credit score appears acceptable.

Therefore, maintaining responsible financial habits is just as important as achieving a good credit score. Consistent repayment behavior, careful debt management, and disciplined credit usage help build trust with lenders and improve personal loan approval chances in 2026.

Income Stability Is More Important Than Income Size

Many people assume that earning a high income automatically increases their chances of getting a personal loan approved. However, banks in 2026 often place greater importance on income stability rather than the total amount of money you earn. This is because lenders want confidence that you will be able to make regular loan payments throughout the repayment period.

A stable income demonstrates financial reliability and reduces the risk of missed payments. Therefore, banks carefully evaluate not only how much you earn but also how consistently that income is received.

When reviewing income stability, lenders typically consider:

- Length of employment with the current employer

- Consistency of salary deposits or business income

- Employment type (permanent, contract, or self-employed)

- History of job changes

- Regularity of monthly earnings

- Supporting income documentation

For example, an applicant earning a moderate but steady salary may sometimes have a stronger approval profile than someone with a higher yet unpredictable income. Similarly, self-employed individuals may need to provide additional records to demonstrate long-term business stability and consistent earnings.

In addition, banks often review bank statements and income history over several months or years. Frequent income fluctuations, employment gaps, or irregular deposits may raise concerns about repayment capacity.

As a result, maintaining a reliable and predictable income stream can significantly improve personal loan approval chances. While income size remains important, lenders generally prefer borrowers who demonstrate long-term financial consistency and stability.

How Banks Measure Debt Burden

One of the most important factors banks evaluate during the personal loan approval process is your debt burden. In simple terms, debt burden refers to the amount of your income that is already being used to repay existing financial obligations. Before approving a new loan, lenders want to ensure that you can comfortably handle additional monthly payments without creating financial stress.

To assess this, banks commonly use a calculation known as the Debt-to-Income (DTI) Ratio. This ratio compares your total monthly debt payments to your monthly income and helps lenders determine your repayment capacity.

What Banks Typically Review

When calculating debt burden, lenders usually consider:

- Existing personal loan EMIs

- Home loan repayments

- Vehicle loan installments

- Credit card minimum payments

- Education loan obligations

- Other recurring debt commitments

In addition, banks compare these obligations against your regular monthly income to understand how much financial flexibility you have left after meeting existing commitments.

Why Debt Burden Matters

A high debt burden can signal increased financial risk. Even if an applicant has a good income and credit score, excessive existing debt may reduce approval chances.

For example, if a large percentage of your income is already allocated to loan repayments, banks may conclude that taking on additional debt could make repayment difficult. As a result, they may:

- Reduce the approved loan amount

- Offer different loan terms

- Request additional verification

- Decline the application in some cases

How to Improve Your Debt Profile

Borrowers can strengthen their loan applications by managing existing obligations responsibly.

Helpful strategies include:

- Paying down outstanding balances

- Avoiding unnecessary new debt before applying

- Reducing credit card utilization

- Consolidating high-interest debt where appropriate

- Maintaining a healthy repayment history

Banking Relationship History and Trust

A strong banking relationship can play a surprisingly important role in personal loan approval decisions. While many borrowers focus on income and credit scores, banks also evaluate how you have managed your accounts and financial activities over time. In 2026, trust remains a key factor in lending, and a positive banking history can help strengthen your overall borrower profile.

Banks prefer to lend money to individuals who have demonstrated responsible financial behavior. Therefore, your relationship with a financial institution can influence how your application is assessed.

What Banks Review in Your Banking History

When evaluating trust and banking relationships, lenders often consider:

- Length of time you have maintained an account

- Consistency of deposits and withdrawals

- Average account balance

- Salary or business income deposits

- Previous loan repayment history

- Credit card management with the same bank

- Overall account activity patterns

In addition, long-term customers who maintain active accounts often provide banks with more financial data, making risk assessment easier and more accurate.

Why Banking Trust Matters

Banks use trust as an additional layer of risk evaluation. If you have a history of managing your finances responsibly, lenders may view you as a lower-risk borrower.

For example, a customer who consistently receives salary deposits, maintains healthy account balances, and has a strong repayment history may receive a more favorable evaluation than a new applicant with limited banking history.

Furthermore, existing customers sometimes benefit from:

- Faster loan processing

- Simplified verification procedures

- Pre-approved loan offers

- Better communication with the lender

Building a Strong Banking Relationship

Developing trust with a bank is a long-term process, but it can improve borrowing opportunities in the future.

Helpful practices include:

- Maintaining regular account activity

- Avoiding cheque bounces or negative balances

- Keeping personal information updated

- Managing loans and credit cards responsibly

- Building a consistent financial record over time

The Rise of Digital Financial Analysis

The personal loan approval process has changed dramatically in recent years, and digital financial analysis is now one of the biggest factors influencing lending decisions in 2026. Instead of relying solely on traditional documents and manual reviews, banks use advanced technology to evaluate an applicant’s financial behavior more accurately and efficiently.

As digital banking continues to grow, financial institutions have access to a much larger amount of data than ever before. Consequently, lenders can build a more complete picture of a borrower’s financial habits, risk profile, and repayment potential.

What Is Digital Financial Analysis?

Digital financial analysis refers to the use of technology, artificial intelligence, and automated systems to review financial information and identify patterns that may affect loan approval decisions.

Rather than focusing only on income and credit scores, banks may also analyze:

- Banking transaction history

- Spending behavior and patterns

- Savings habits

- Cash flow consistency

- Income deposits and withdrawals

- Existing financial commitments

- Digital payment activity

As a result, lenders can assess financial discipline more effectively.

How Banks Use Digital Data

Modern lending systems process large amounts of financial information within seconds. These systems help banks identify potential risks and make faster decisions.

For example, banks may evaluate:

- Whether income is received regularly

- How often large withdrawals occur

- Spending consistency over time

- Overall money management habits

In addition, AI-powered systems can detect unusual financial activity that may require further review.

Benefits of Digital Financial Analysis

The adoption of digital analysis provides advantages for both lenders and borrowers.

Some benefits include:

- Faster loan approval decisions

- More accurate risk assessment

- Reduced paperwork requirements

- Improved fraud detection

- Better customer experience

Consequently, borrowers with strong financial habits may benefit from quicker and smoother approval processes.

Why Financial Behavior Matters More Than Ever

Because banks can now review detailed financial patterns, responsible money management has become increasingly important.

Positive financial behaviors include:

- Regular savings contributions

- Consistent bill payments

- Controlled spending habits

- Stable account activity

- Responsible credit usage

On the other hand, irregular financial activity may affect how lenders evaluate risk.