Hook Introduction

Imagine earning a good income, paying your bills regularly, and feeling financially responsible—only to have your personal loan application rejected within minutes. Credit Score 2026

It happens more often than people realize.

Many consumers assume that income alone determines whether they qualify for loans, credit cards, or favorable interest rates. In reality, lenders often pay closer attention to a different number: your credit score.

A credit score has become one of the most powerful financial indicators in modern life. It can influence whether you get approved for a mortgage, how much interest you pay on a car loan, whether you qualify for premium credit cards, and even the financial products available to you.

In 2026, credit scores matter more than ever.

Digital lending platforms now process applications within minutes. Artificial intelligence helps lenders evaluate risk faster. Financial institutions increasingly rely on automated decision-making systems that analyze credit profiles before a human ever reviews an application.

As a result, a strong credit score can open doors.

A poor credit score can quietly close them.

The challenge is that many beginners do not fully understand how credit scores work. They may make small mistakes without realizing those actions can affect their financial future for years.

The good news is that improving your credit score is not about secret tricks or complicated financial strategies.

It starts with understanding how the system works.

Once you understand the factors that influence your score, you can make smarter decisions, avoid common mistakes, and build a stronger financial foundation.

This guide explains everything beginners need to know about credit scores in 2026, including how scores are calculated, why they matter, common mistakes to avoid, and practical strategies to improve your credit profile over time.

How will credit scores change in 2026?

Key Credit Score Changes in 2026

1. More Focus on Long-Term Behavior

Newer scoring models such as FICO 10T use “trended data,” meaning they analyze up to 24 months of credit behavior rather than a single snapshot. Consistently reducing debt may help your score, while carrying high balances for long periods may hurt it.

2. Buy Now, Pay Later (BNPL) Activity Matters More

Some newer scoring systems can incorporate BNPL payment history. Making BNPL payments on time may have little or slightly positive effects, while missed payments could negatively impact creditworthiness.

3. Alternative Payment Data Gains Importance

Rent, utility, telecom, and similar recurring payments are increasingly being considered by certain lenders and scoring models. This can benefit people with limited traditional credit histories.

4. More Credit Score Models in Use

Lenders are beginning to use a broader range of scoring models, including newer FICO and VantageScore versions. This means you may see slightly different scores depending on which model a lender uses.

What Still Hurts Your Score Most

- Late or missed payments

- High credit card utilization

- Loan defaults

- Collections and charge-offs

- Too many new credit applications in a short period

Payment history remains the most influential factor in most credit scoring systems.

How to Prepare for 2026

- Pay all bills on time.

- Keep credit card balances low.

- Monitor your credit reports regularly.

- Avoid unnecessary loan or card applications.

- If available, report rent and utility payments to credit bureaus.

- Gradually pay down existing debt rather than only making minimum payments.

Bottom Line

The biggest trend in 2026 is that credit scoring is becoming more holistic. Lenders are looking beyond a single month’s credit report and paying closer attention to long-term financial habits, rent payments, and alternative credit data. Consumers who consistently manage debt and make payments on time are likely to benefit most from these changes

What Is a Credit Score?

A credit score is a numerical representation of your creditworthiness.

In simple terms, it helps lenders estimate how likely you are to repay borrowed money on time.

Think of your credit score as a financial reputation score.

Just as employers review resumes before offering jobs, lenders review credit scores before approving loans and credit products.

Your score is generated using information from your credit history, including: Credit Score 2026

- Payment history

- Credit card usage

- Existing loans

- Length of credit history

- New credit applications

- Types of credit accounts

The score provides lenders with a quick snapshot of your financial behavior.

A higher score generally indicates lower risk.

A lower score suggests higher risk.

Why Lenders Use Credit Scores

Financial institutions face risk whenever they lend money.

A lender wants confidence that borrowers will make payments as agreed.

Credit scores help lenders:

- Assess risk quickly

- Standardize approval decisions

- Determine loan eligibility

- Set interest rates

- Reduce default losses

Rather than manually reviewing every financial detail, lenders can use credit scores as a starting point for evaluating applicants.

Why Consumers Should Care

Many people only think about credit scores when applying for a loan.

However, credit scores can affect numerous financial opportunities, including:

- Personal loans

- Auto loans

- Mortgage approvals

- Credit card applications

- Credit limits

- Interest rates

- Insurance pricing in some markets

A strong credit score can save thousands of dollars over time by helping borrowers qualify for lower interest rates and better financial products.

For beginners, understanding credit scores is one of the most important steps toward long-term financial success.

What is a good credit score in 2026?

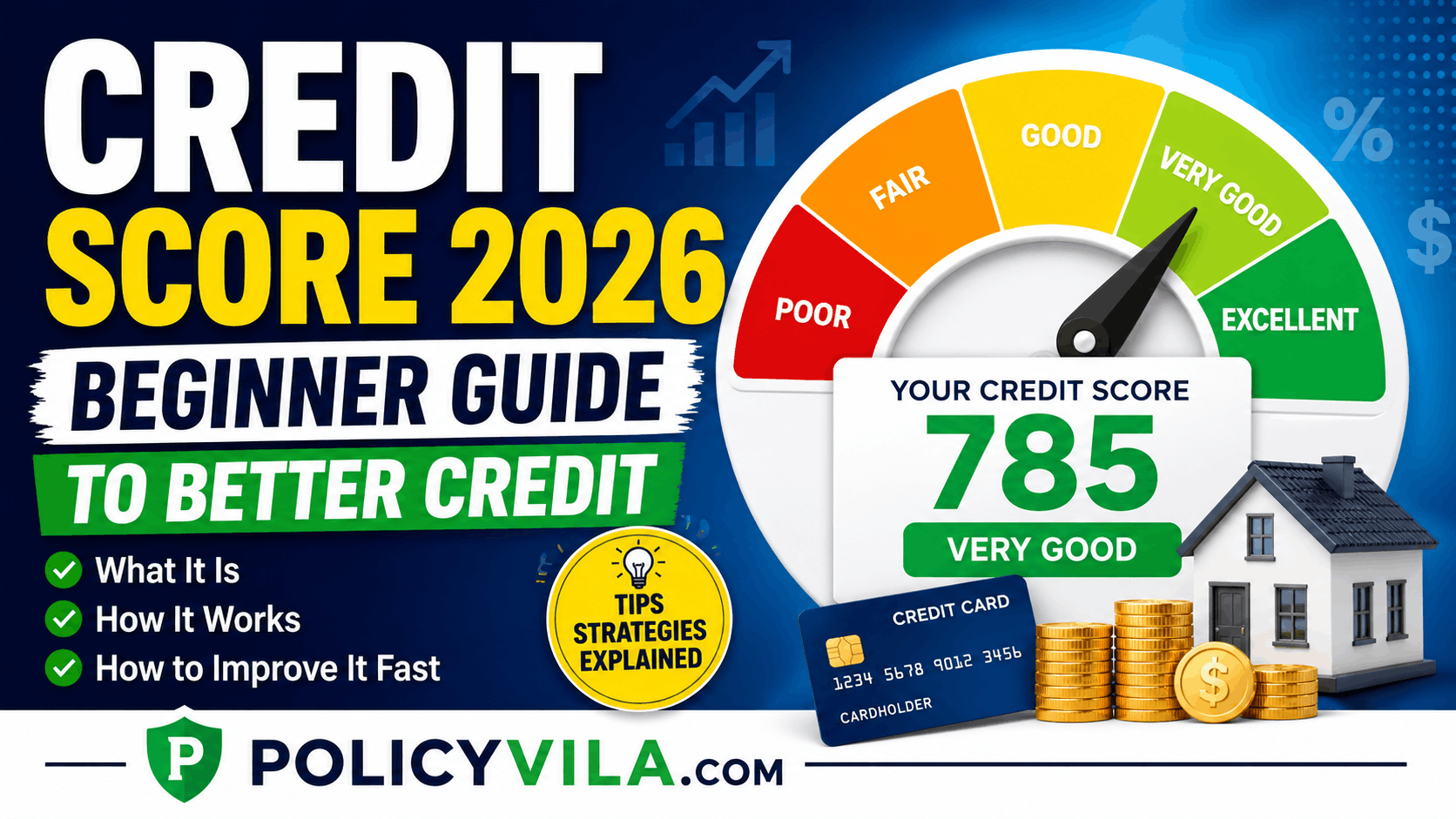

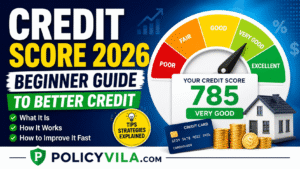

Common Credit Score Ranges

| Credit Score | Rating |

|---|---|

| 300–579 | Poor |

| 580–669 | Fair |

| 670–739 | Good |

| 740–799 | Very Good |

| 800–850 | Excellent |

What Is Considered a Good Score?

For most lenders in 2026:

- 670 or higher is generally considered good.

- 740 or higher often qualifies for better loan and credit card offers.

- 800+ is typically considered excellent and may help secure the most competitive interest rates.

Why a Good Credit Score Matters

A strong credit score can help you:

- Qualify for loans more easily

- Receive lower interest rates

- Get approved for premium credit cards

- Improve chances of rental approval

- Access higher credit limits

Factors That Influence Your Credit Score

The most important factors include:

- Payment history

- Credit utilization (how much credit you use)

- Length of credit history

- Credit mix

- New credit applications

Tips to Maintain a Good Score in 2026

- Pay all bills on time.

- Keep credit card balances low.

- Avoid applying for multiple loans or cards at once.

- Review your credit report regularly for errors.

- Maintain older credit accounts when possible.

Bottom Line

In 2026, a credit score of 670+ is generally considered good, while 740+ is very good and 800+ is excellent. Consistent on-time payments and responsible credit usage remain the most effective ways to build and maintain a strong credit profile.

Why Credit Scores Matter More in 2026

The financial landscape continues to evolve rapidly.

Traditional lending processes that once took days or weeks can now happen in minutes.

Several trends are making credit scores increasingly important.

Digital Lending Growth

Online lenders continue expanding their services.

Consumers can now apply for loans, credit cards, and financing directly from mobile devices.

Because these applications are processed digitally, credit scores often play a central role in approval decisions.

Why Credit Scores Matter More in 2026 (Continued)

AI-Based Risk Assessment

Artificial intelligence is transforming how lenders evaluate borrowers.

Instead of relying solely on manual reviews, many financial institutions now use sophisticated algorithms that analyze credit-related data within seconds.

These systems evaluate:

- Credit history

- Existing debt levels

- Payment behavior

- Credit utilization

- Recent applications

Because automated systems process information quickly, maintaining a healthy credit profile has become even more important.

Faster Loan Approvals

Modern lending platforms can provide approval decisions within minutes.

While this convenience benefits consumers, it also means lenders depend heavily on credit data.

A strong credit score may help borrowers:

- Receive faster approvals

- Access larger loan amounts

- Qualify for lower interest rates

- Gain access to premium financial products

A weak score may produce the opposite result.

Increased Reliance on Credit Profiles

As digital finance expands, credit profiles continue becoming a key factor in financial decision-making.

Consumers with strong credit histories often enjoy more flexibility and better financial opportunities.

Those with poor credit histories may face higher borrowing costs and limited options.

For this reason, understanding your credit score is no longer optional. It is an essential part of modern financial management.

How Credit Scores Are Calculated

Many beginners assume credit scores are mysterious numbers generated randomly.

In reality, credit scores are based on specific financial behaviors.

Understanding these factors can help you focus on actions that positively influence your score.

Payment History

Payment history is often the most important factor affecting a credit score.

Lenders want evidence that borrowers pay obligations on time.

Positive payment history includes:

- On-time credit card payments

- Consistent loan payments

- Timely account management

Negative payment history includes:

- Late payments

- Missed payments

- Loan defaults

- Collection accounts

Even a single missed payment can affect a credit profile.

This is why setting up automatic payments can be beneficial.

Credit Utilization

Credit utilization measures how much available credit you are currently using.

Example:

Credit card limit: $10,000

Current balance: $2,000

Credit utilization: 20%

Lower utilization generally signals responsible credit management.

Many experts recommend keeping utilization below 30%.

Lower percentages often produce stronger results.

Length of Credit History

Lenders value long-term financial responsibility.

The longer your credit history, the more information lenders have available.

Factors include:

- Age of oldest account

- Average account age

- Length of active credit usage

Closing old accounts unnecessarily can sometimes reduce the average age of your credit history.

Credit Mix

Credit mix refers to the variety of credit accounts you manage.

Examples include:

- Credit cards

- Auto loans

- Student loans

- Personal loans

- Mortgages

A diverse credit profile can demonstrate an ability to manage different financial obligations responsibly.

However, opening accounts solely to improve credit mix is usually not recommended.

New Credit Applications

Every time you apply for new credit, lenders may review your credit report.

Multiple applications within a short period can indicate financial stress.

As a result, frequent applications may temporarily affect your score.

Before applying for new credit products, consider whether the application is truly necessary.

Credit Score Ranges Explained

Understanding score ranges helps consumers evaluate their financial position.

| Credit Score Range | Rating | Financial Impact |

|---|---|---|

| 300–579 | Poor | Higher rejection risk and higher interest rates |

| 580–669 | Fair | Limited borrowing options |

| 670–739 | Good | Access to many financial products |

| 740–799 | Very Good | Better approval odds and competitive rates |

| 800–850 | Excellent | Access to premium rates and offers |

Poor Credit Scores

Borrowers in this range may face:

- Loan rejections

- High interest rates

- Lower credit limits

Improving payment behavior becomes especially important.

Fair Credit Scores

This range often represents an opportunity for improvement.

Borrowers may qualify for some products but often pay higher borrowing costs.

Good Credit Scores

Good scores generally provide access to favorable financial opportunities.

Many lenders consider this range low-risk.

Very Good Credit Scores

Borrowers often receive:

- Better loan terms

- Lower interest rates

- Stronger approval chances

Excellent Credit Scores

This range represents outstanding credit management.

While perfection is unnecessary, maintaining excellent credit can produce significant long-term savings.

Common Credit Score Mistakes

Many credit problems are self-inflicted.

The encouraging reality is that most mistakes can be avoided.

Mistake #1: Making Late Payments

Late payments can damage credit profiles quickly.

Solution:

- Use automatic payments

- Set reminders

- Monitor due dates

Mistake #2: Maxing Out Credit Cards

High balances can increase utilization ratios.

Solution:

- Keep balances low

- Pay down debt regularly

Mistake #3: Applying for Too Many Credit Accounts

Frequent applications may raise concerns for lenders.

Solution:

Apply only when necessary.

Mistake #4: Ignoring Credit Reports

Errors occasionally occur.

Solution:

Review reports regularly.

Mistake #5: Closing Old Accounts Too Quickly

Older accounts contribute to credit history length.

Solution:

Evaluate carefully before closing accounts.

Mistake #6: Missing Small Payments

Even small overlooked balances can become collection accounts.

Mistake #7: Co-Signing Without Understanding Risk

Co-signers may become responsible for unpaid debt.

Mistake #8: Carrying High Revolving Balances

Large balances increase utilization and financial risk.

Mistake #9: Ignoring Financial Planning

Poor budgeting often leads to credit problems.

Mistake #10: Assuming Income Determines Credit Scores

Credit scores measure borrowing behavior, not salary levels.

A high-income individual can still have poor credit.

The Hidden Credit Score Traps Most Beginners Never Notice

Some credit risks receive very little attention.

Yet these issues can affect financial outcomes significantly.

Buy Now, Pay Later Services

BNPL services can create multiple repayment obligations.

Missed payments may affect credit profiles depending on the provider.

Subscription Payment Problems

Expired cards and failed automatic payments can create unexpected issues.

Missed Auto-Payments

Automation helps, but monitoring remains important.

Bank account changes or insufficient funds can cause missed payments.

Small Collection Accounts

A forgotten utility bill or medical invoice may eventually reach collections.

Small balances can create surprisingly large credit consequences.

Identity Theft Risks

Unauthorized accounts can damage credit if not addressed promptly.

Monitoring financial accounts regularly helps reduce risk.

How to Improve Your Credit Score Faster

Improving a credit score takes time, but certain strategies can produce meaningful results faster than others. The key is focusing on actions that directly impact the factors used in credit scoring models.

Pay Every Bill on Time

If there is one habit that can have the biggest impact on your credit score, it is making payments on time.

Payment history is often the largest component of a credit score.

Simple ways to avoid late payments include:

- Setting automatic payments

- Using calendar reminders

- Scheduling payments immediately after payday

- Monitoring due dates regularly

Even one missed payment can remain on a credit report for years.

read also: The Simple Budgeting Mistake That Costs People Thousands Every Year

Lower Credit Card Balances

Reducing credit utilization can improve credit scores relatively quickly.

Example:

- Credit limit: $10,000

- Current balance: $8,000

- Utilization: 80%

Reducing the balance to $2,000 lowers utilization to 20%, which generally looks much better to lenders.

Many consumers see score improvements after lowering revolving debt balances.

Avoid Applying for Unnecessary Credit

Each new application may trigger a credit inquiry.

Multiple inquiries within a short period can negatively affect scores.

Before applying, ask yourself:

- Do I actually need this account?

- Will this application improve my financial situation?

- Am I likely to be approved?

Being selective helps protect your credit profile.

Review Credit Reports Regularly

Errors occur more often than many people realize.

Examples include:

- Incorrect balances

- Duplicate accounts

- Identity theft activity

- Outdated negative information

Checking reports regularly allows consumers to identify and dispute inaccuracies quickly.

Keep Old Accounts Open

Older accounts contribute to credit history length.

Closing accounts unnecessarily can sometimes reduce average account age and increase utilization percentages.

Before closing an account, evaluate the potential impact carefully.

Become an Authorized User

In some situations, being added as an authorized user on a well-managed credit card account can help build credit history.

The primary cardholder should have:

- Excellent payment history

- Low utilization

- Responsible account management

This strategy may help beginners establish stronger credit profiles.

Build Positive Credit History Consistently

There are no permanent shortcuts to excellent credit.

The most effective long-term strategy remains:

- Consistent payments

- Responsible borrowing

- Low utilization

- Patience

Strong credit scores are built through repeated positive financial behavior.

Credit Score Myths vs Facts

| Myth | Fact |

|---|---|

| Checking your own credit score hurts your score | Personal credit checks generally do not affect scores |

| High income guarantees excellent credit | Credit scores are based on behavior, not salary |

| Carrying a balance improves credit | Paying balances responsibly is usually better |

| Closing old accounts always helps | It can sometimes hurt credit history length |

| One missed payment doesn’t matter | Even one late payment can affect credit |

| You need debt to build wealth | Responsible credit use matters more than debt itself |

| Credit repair companies can instantly fix bad credit | Legitimate improvements require time |

| Student loans automatically ruin credit | Properly managed loans can help build history |

| Credit scores only matter for loans | They affect many financial opportunities |

| Excellent credit happens quickly | Strong scores typically require years of good habits |

Why These Myths Persist

Financial misinformation spreads easily.

Many consumers receive advice from:

- Friends

- Social media

- Online forums

- Marketing advertisements

Unfortunately, not all advice is accurate.

Understanding facts helps consumers make better financial decisions.

Credit Score and Loan Approval

Credit scores play a major role in lending decisions.

Although income, employment, and debt levels matter, lenders often use credit scores as a primary screening tool.

Personal Loans

Personal loan lenders frequently evaluate:

- Credit score

- Debt-to-income ratio

- Income stability

- Payment history

Higher scores often lead to:

- Better approval odds

- Larger loan amounts

- Lower interest rates

Auto Loans

Vehicle financing terms often depend heavily on credit quality.

A borrower with excellent credit may receive significantly lower rates than someone with poor credit.

Over several years, this difference can save thousands of dollars.

Home Loans

Mortgage lenders generally perform extensive credit reviews.

Strong credit may help borrowers:

- Qualify for larger mortgages

- Receive lower interest rates

- Reduce borrowing costs

Even small interest rate differences can dramatically affect long-term mortgage expenses.

Credit Cards

Credit card issuers frequently use credit scores to determine:

- Approval decisions

- Credit limits

- Interest rates

- Reward program eligibility

Premium credit cards often require stronger credit profiles.

Credit Score and Financial Freedom

Many people view credit scores only as borrowing tools.

However, healthy credit contributes to broader financial freedom.

Lower Borrowing Costs

Better credit often means:

- Lower interest rates

- Reduced financing costs

- Greater purchasing power

Saving money on interest leaves more resources available for investing and wealth building.

Increased Financial Flexibility

Strong credit creates options.

Consumers may gain access to:

- Emergency financing

- Better credit products

- Favorable loan terms

Having options can reduce financial stress during difficult situations.

Wealth Building Opportunities

Money saved through lower borrowing costs can be redirected toward:

- Investments

- Retirement accounts

- Emergency funds

- Business opportunities

Over decades, these advantages can compound significantly.

Financial Confidence

People with healthy credit profiles often feel more confident making major financial decisions.

Examples include: Credit Score 2026

- Purchasing a home

- Starting a business

- Financing education

- Relocating for career opportunities

Strong credit supports long-term financial growth.

read also: Top 10 Life Insurance Policies for Young Professionals in 2026

Expert Tips for Beginners

1. Never Miss a Due Date

Payment history remains the foundation of good credit.

2. Keep Utilization Below 30%

Lower utilization generally supports stronger scores.

3. Track Spending Monthly

Financial awareness improves decision-making.

4. Create an Emergency Fund

Unexpected expenses often trigger missed payments.

5. Avoid Emotional Borrowing

Borrow based on needs, not emotions.

6. Use Automatic Payments

Automation reduces mistakes.

7. Review Credit Reports Annually

Regular monitoring identifies issues early.

8. Maintain Older Accounts

Credit history length matters.

9. Limit New Applications

Avoid unnecessary inquiries.

10. Budget Before Borrowing

Good budgeting reduces credit problems.

11. Pay More Than Minimum Payments

Debt decreases faster.

12. Monitor Subscription Charges

Small recurring payments can create issues.

13. Protect Personal Information

Identity theft can damage credit.

14. Learn Basic Financial Skills

Financial education supports long-term success.

15. Think Long Term

Excellent credit is built over years, not weeks.

30-Day Credit Score Improvement Challenge

Improving a credit score does not require complicated financial strategies. In many cases, consistent actions performed over a single month can create a strong foundation for long-term improvement.

This 30-day challenge is designed specifically for beginners who want to take control of their credit health.

Week 1: Understand Your Current Credit Situation

The first step is awareness.

Many people try to improve their credit score without knowing where they currently stand.

Tasks

✅ Check your credit score

✅ Review your credit report

✅ Verify account balances

✅ Identify late payments

✅ List all debts

Goal

Gain a complete understanding of your current credit profile.

What You’ll Learn

By the end of Week 1, you should know:

- Your current credit score

- Total debt amount

- Credit utilization percentage

- Existing payment history issues

- Areas needing improvement

Knowledge creates the foundation for better decisions.

Week 2: Fix Financial Leaks

Many credit problems stem from poor money management rather than income limitations.

This week focuses on preventing future mistakes.

Tasks

✅ Set up automatic payments

✅ Create payment reminders

✅ Reduce unnecessary spending

✅ Build a basic budget

✅ Avoid new credit applications

Goal

Prevent new negative information from appearing on your credit report.

Why This Matters

Every month without late payments strengthens your credit profile.

Consistency is often more important than dramatic changes.

Week 3: Lower Credit Utilization

Credit utilization can have a significant impact on scores.

This week focuses on reducing outstanding balances.

Tasks

✅ Pay down credit card balances

✅ Make extra debt payments

✅ Avoid new revolving debt

✅ Track utilization percentages

✅ Prioritize high-interest balances

Example

Credit Limit: $5,000

Balance: $4,000

Utilization: 80%

After Paying $2,500:

Balance: $1,500

Utilization: 30%

This improvement can positively affect credit scoring models.

Goal

Move utilization below 30% whenever possible.

read also: Best Family Insurance Policies 2026: Compare Costs, Coverage & Hidden Benefits

Week 4: Build Long-Term Credit Habits

Strong credit is built through habits rather than quick fixes.

This week focuses on creating systems that continue beyond the challenge.

Tasks

✅ Create a savings plan

✅ Build emergency fund goals

✅ Review financial goals

✅ Schedule monthly credit reviews

✅ Commit to responsible borrowing

Goal

Develop sustainable habits that support long-term credit health.

Long-Term Benefits

These habits can help:

- Improve credit scores

- Reduce financial stress

- Lower borrowing costs

- Increase financial confidence

- Support wealth building

Frequently Asked Questions (FAQs)

1. What is considered a good credit score in 2026?

Generally, scores above 670 are considered good by many lenders.

Higher scores often provide access to better loan terms and lower interest rates.

2. How long does it take to improve a credit score?

The timeline varies.

Some improvements may appear within a few months, while major credit rebuilding efforts may require a year or longer.

Consistency matters most.

3. Can checking my own credit score lower it?

No.

Checking your own credit score is typically considered a soft inquiry and does not negatively impact your score.

4. How often should I review my credit report?

Reviewing your report several times each year is a smart practice.

Regular reviews help identify errors and potential fraud quickly.

5. Does paying off a loan automatically increase my credit score?

Not always immediately.

However, reducing debt generally improves overall financial health and may benefit your credit profile over time.

6. Can small financial habits really make a difference?

Absolutely.

Small daily decisions repeated over months and years often determine financial outcomes more than occasional major decisions.

Consistency creates powerful results.

7. Is investing more important than saving?

Both are important.

Savings provide short-term security.

Investments help build long-term wealth.

A healthy financial plan typically includes both.

8. What is the biggest mistake people make with money?

One of the most common mistakes is spending first and saving later.

Successful savers typically reverse this process by saving first and spending what remains.

9. Can a low credit score prevent loan approval?

Yes.

Many lenders use credit scores as a major factor when evaluating applications.

A low score may reduce approval chances or increase borrowing costs.

10. What is the fastest legitimate way to improve a credit score?

The most effective strategies include:

- Paying bills on time

- Lowering credit utilization

- Avoiding unnecessary applications

- Monitoring credit reports

- Maintaining responsible credit habits

There are no instant fixes, but consistent action can produce meaningful improvement.

read also: The Hidden Money Habits That Are Quietly Costing You Thousands in 2026

Final Thoughts

Credit Score 2026 is far more than a number on a financial report.

It influences borrowing opportunities, interest rates, financial flexibility, and long-term wealth-building potential.

The encouraging news is that excellent credit is not reserved for wealthy individuals or financial experts.

Strong credit is typically the result of simple habits practiced consistently:

- Paying bills on time

- Managing debt responsibly

- Monitoring credit reports

- Keeping utilization low

- Planning ahead financially

Every positive financial decision contributes to a stronger credit profile.

Whether your current score is poor, fair, good, or excellent, the principles remain the same.

Focus on progress rather than perfection.

Build systems that support good financial behavior.

Stay consistent.

A year from now, the small actions you take today could be the reason you qualify for better loans, save thousands in interest, and enjoy greater financial freedom.

Your credit score is not just a reflection of your past financial behavior—it is also a tool that can help shape your future.