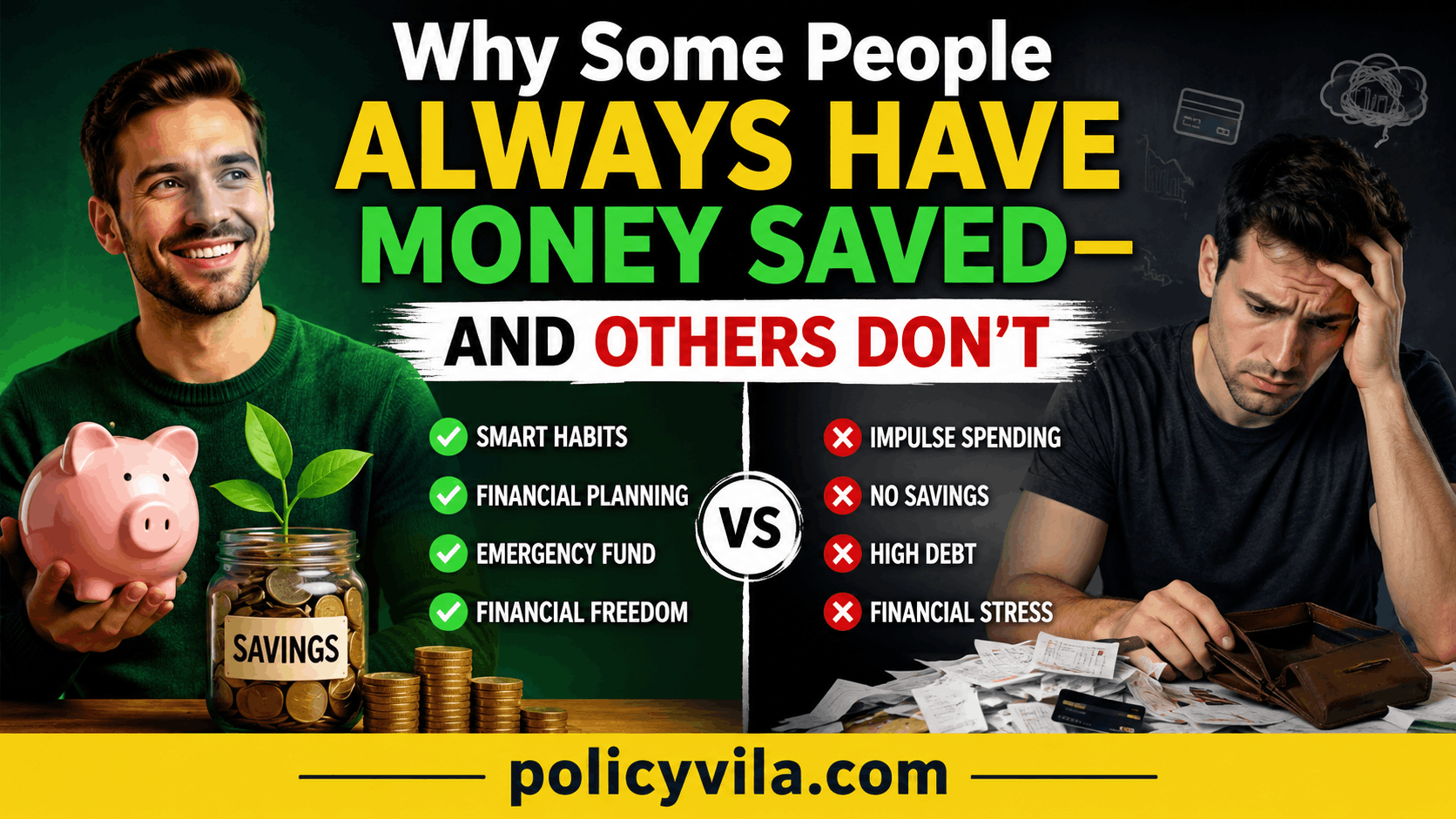

Hook Introduction

Have you ever noticed that some people always seem financially prepared? why some people always have money saved

Their car breaks down, and they pay for repairs without panic. An unexpected medical bill arrives, and they handle it without borrowing money. They take vacations, invest regularly, and appear surprisingly calm when financial challenges arise.

Meanwhile, others earn similar incomes but constantly feel short on cash. Every unexpected expense becomes a crisis. Savings accounts remain empty, credit card balances grow, and financial stress becomes a regular part of life.

At first glance, it may seem like income is the difference.

However, income alone rarely explains why some people consistently save money while others struggle.

Many high-income earners live paycheck to paycheck. At the same time, some moderate-income households build impressive savings and maintain strong financial stability.

The real difference often comes down to habits, behaviors, decision-making patterns, and financial systems.

In 2026, saving money has become more challenging than ever. Digital payments make spending effortless. Subscription services quietly drain bank accounts. Social media encourages constant comparison and lifestyle inflation. Consumers are surrounded by opportunities to spend money every hour of every day.

Despite these challenges, millions of people continue building savings successfully.

What do they do differently?

The answer is surprisingly practical.

People who consistently save money rarely possess secret financial knowledge. Instead, they follow a collection of habits that gradually strengthen their finances over time.

Understanding these habits can help anyone improve their financial future, regardless of income level.

Understanding Why Saving Money Is Difficult

Most people believe saving money is simply a matter of self-control.

The reality is much more complicated.

Human beings are naturally wired to prioritize immediate rewards over future benefits.

Psychologists refer to this as present bias.

For example:

- Spending $50 today provides immediate satisfaction.

- Saving $50 may provide benefits months or years later.

Because the reward from spending arrives instantly, many people choose short-term gratification over long-term financial security.

Modern technology amplifies this challenge.

A few decades ago, spending money often required more effort:

- Visiting stores

- Carrying cash

- Writing checks

- Comparing prices manually

Today, consumers can purchase products within seconds.

One-click ordering, digital wallets, automatic subscriptions, and targeted advertising make spending easier than ever before.

As a result, saving money requires intentional effort.

People who consistently save understand this reality and create systems that protect them from impulsive decisions.

The Biggest Misconception About Savings

One of the most common financial myths is that saving depends primarily on income.

While higher income certainly creates more opportunities to save, income alone does not guarantee financial success. Many people assume that once they earn a larger salary, saving money will become automatic. However, real-life financial situations often prove otherwise.

Consider these two examples: why some people always have money saved

Person A

Annual income: $120,000

- Expensive vehicle payments

- Frequent dining out

- Luxury subscriptions

- Minimal budgeting

- Limited savings

Person B

Annual income: $60,000

- Controlled spending

- Regular budgeting

- Automatic savings transfers

- Emergency fund

- Consistent investing

Despite earning half as much, Person B may accumulate more wealth over time.

The difference is behavior rather than income.

This principle appears repeatedly across all income levels. Financial success often depends more on what people do with their money than how much they earn.

Many high-income earners experience financial stress because their spending grows alongside their earnings. Every salary increase is quickly absorbed by lifestyle upgrades, larger expenses, and additional financial commitments. As a result, even though more money is coming in, very little remains available for saving.

On the other hand, individuals who develop strong financial habits often save consistently regardless of income level. They understand the importance of controlling expenses, planning ahead, and prioritizing long-term financial security over short-term gratification.

Another reason this misconception persists is that people often compare visible income rather than invisible financial habits. It is easy to notice someone’s salary, car, house, or lifestyle. It is much harder to see their savings account balance, emergency fund, investment portfolio, or debt obligations.

Because of this, many people incorrectly assume that higher earners are automatically building wealth. In reality, wealth is often determined by the gap between income and spending. The larger that gap becomes, the greater the opportunity to save, invest, and achieve financial independence.

Saving money is ultimately a habit. Habits are formed through repeated actions over time. Someone who saves a small amount consistently every month may build a stronger financial foundation than someone who earns significantly more but spends nearly everything they make.

This is why financial experts frequently emphasize behavior over income. Budgeting, expense tracking, goal setting, emergency planning, and disciplined spending decisions often have a greater impact on long-term financial outcomes than salary alone.

The most successful savers recognize that earning money is only one part of the equation. Keeping a portion of that money, protecting it, and allowing it to grow over time is what creates lasting financial stability.

Ultimately, the biggest misconception about savings is believing that more income automatically leads to more wealth. While income creates opportunity, financial habits determine the outcome. People who consistently save money focus not only on increasing earnings but also on managing those earnings wisely. Over time, these habits compound and create significant financial advantages that can last a lifetime.

Habit #1: Savers Pay Themselves First

People who consistently save money follow a simple rule:

They save before spending.

Although this concept sounds straightforward, it is one of the most powerful habits behind long-term financial success. Many individuals believe saving money is something they will do after covering expenses, but this approach often leads to disappointment because unexpected costs and discretionary spending consume most of the available income.

Most people manage money using the following sequence: why some people always have money saved

- Earn income

- Pay bills

- Spend money

- Save whatever remains

Unfortunately, little remains.

By the time housing costs, transportation expenses, groceries, subscriptions, entertainment, and miscellaneous purchases are paid for, there is often very little left to save. This cycle repeats month after month, making it difficult to build an emergency fund or achieve long-term financial goals.

Successful savers reverse the process.

Their financial system looks like this:

- Earn income

- Save automatically

- Pay bills

- Spend the remainder

This small adjustment creates a major difference over time. Instead of hoping money will be left over, savings become a priority from the beginning.

Why This Habit Works So Well

Paying yourself first ensures that saving is treated as a necessity rather than an optional activity. Just as rent, utilities, and insurance payments are considered important obligations, savings become a non-negotiable part of the monthly budget.

This approach removes uncertainty from the saving process. Rather than asking whether there is enough money left to save, the money has already been set aside before spending decisions are made.

As a result, savings grow more consistently and financial goals become easier to achieve.

The Power of Automation

One reason successful savers maintain this habit is that they rely on systems rather than motivation.

Motivation changes from day to day. Financial systems remain consistent.

Common examples include:

- Automatic transfers to savings accounts

- Payroll deductions into retirement plans

- Automatic investment contributions

- Scheduled transfers to emergency funds

Because these transfers occur automatically, there is no need to make a saving decision every month. The process happens in the background without requiring constant attention. why some people always have money saved

This significantly reduces the temptation to spend money that was intended for future goals.

Creating a Strong Financial Foundation

Paying yourself first does more than increase savings balances. It helps create a stronger financial foundation by supporting important financial objectives such as:

- Building an emergency fund

- Preparing for major purchases

- Funding retirement accounts

- Reducing financial stress

- Creating long-term financial security

Individuals who consistently save first are often better prepared for unexpected expenses and less likely to rely on debt during financial emergencies.

Small Contributions Can Create Big Results

Many people delay saving because they believe they need large amounts of money to make a difference.

However, successful savers understand that consistency is often more important than the starting amount.

Even small contributions made regularly can accumulate significantly over time.

For example:

- Saving $25 per week equals approximately $1,300 per year.

- Saving $50 per week equals approximately $2,600 per year.

- Saving $100 per week equals approximately $5,200 per year.

As income grows, these contributions can gradually increase, accelerating financial progress.

Turning Saving Into a Habit

Like any habit, paying yourself first becomes easier with repetition.

Initially, it may require conscious effort and planning. Over time, however, it becomes part of a normal financial routine. Individuals adjust their spending to the money that remains rather than attempting to save what is left over.

This shift in behavior often separates people who consistently build wealth from those who struggle to save despite earning a good income.

Long-Term Impact

The true power of paying yourself first becomes visible over years rather than weeks.

Consistent saving allows individuals to:

- Build financial confidence

- Handle emergencies more effectively

- Take advantage of investment opportunities

- Reduce dependence on debt

- Move closer to financial independence

Ultimately, paying yourself first is not just a saving strategy. It is a mindset that prioritizes future financial security over short-term spending. By making savings automatic and treating it as a regular financial obligation, anyone can begin building a stronger and more secure financial future.

read also: CGL Policy Insurance: Complete Business Coverage Guide 2026

Habit #2: They Track Their Money Regularly

People who save successfully know exactly where their money goes.

They do not rely on guesses.

They review:

- Bank statements

- Credit card transactions

- Subscription payments

- Monthly expenses

Tracking expenses creates awareness.

Awareness creates better decisions.

Many spending problems exist simply because people never measure their financial behavior.

Imagine attempting to lose weight without tracking food intake.

Financial management works similarly.

When spending becomes visible, improvement becomes easier.

Regular tracking helps identify:

- Wasteful purchases

- Recurring charges

- Budget leaks

- Saving opportunities

The goal is not perfection.

The goal is awareness.

Financial awareness consistently separates savers from non-savers.

Habit #3: They Avoid Lifestyle Inflation

One of the biggest reasons people fail to build savings is lifestyle inflation.

Lifestyle inflation occurs when spending increases every time income increases.

A raise arrives.

Spending increases.

A promotion arrives.

Spending increases again.

Years pass.

Income grows substantially.

Savings remain unchanged.

Successful savers resist this pattern.

Instead of spending every additional dollar, they allocate part of income growth toward:

- Savings

- Investments

- Emergency funds

- Retirement accounts

As a result, wealth grows alongside income.

This creates genuine financial progress rather than the appearance of financial success.

Many people focus on looking wealthy.

Successful savers focus on becoming wealthy.

That difference matters.

How Lifestyle Inflation Happens

Lifestyle inflation often develops gradually.

Most people do not suddenly double their spending overnight.

Instead, small upgrades begin to appear:

- A more expensive vehicle

- More frequent restaurant meals

- Premium subscription services

- Larger housing expenses

- Luxury purchases

- Costlier vacations

Each expense may seem reasonable individually. However, when combined, these upgrades can consume most of an income increase.

As a result, financial progress slows despite earning more money.

Why Lifestyle Inflation Is Dangerous

The biggest danger is that it creates the illusion of success.

Income rises.

Lifestyle improves.

But savings and investments remain unchanged.

Many individuals assume they are becoming wealthier because they earn more money. In reality, their financial position may remain largely the same if spending grows at the same pace as income.

This is one reason some high-income earners still experience financial stress and live paycheck to paycheck.

How Successful Savers Respond to Raises

Successful savers often create a plan before additional income arrives.

For example, when receiving a raise, they may decide to:

- Save 50% of the increase

- Invest 30% of the increase

- Spend only 20% of the increase

This allows them to enjoy improved earnings while still strengthening their financial future.

A Practical Example

Imagine receiving a $500 monthly raise.

A common response might be:

- Higher car payment: $200

- More dining out: $150

- Additional subscriptions: $50

- Miscellaneous spending: $100

Result:

The entire raise disappears.

A successful saver might instead choose:

- Savings: $250

- Investments: $150

- Lifestyle improvements: $100

Result:

Financial security improves every month while still enjoying some of the additional income.

The Long-Term Impact

Avoiding lifestyle inflation creates one of the largest advantages in personal finance.

Over time, consistently directing income growth toward savings and investments can lead to:

- Larger emergency funds

- Faster debt repayment

- Greater investment growth

- Earlier retirement opportunities

- Increased financial independence

Ultimately, the goal is not to avoid enjoying higher income. The goal is to ensure that income growth improves both your lifestyle and your financial future. People who master this balance often build wealth far more effectively than those who spend every additional dollar they earn.

read also: Best Family Insurance Policies 2026: Compare Costs, Coverage & Hidden Benefits

Habit #4: They Have Clear Financial Goals

People who save money consistently rarely save without a purpose.

They know exactly what they are working toward.

Their goals might include:

- Building an emergency fund

- Buying a home

- Starting a business

- Paying off debt

- Funding retirement

- Taking a dream vacation

Specific goals create motivation.

Saving money simply because someone “should save” often lacks emotional commitment.

Compare these two situations:

Goal Without Purpose

“I should save more money.”

Goal With Purpose

“I want $10,000 saved for a home down payment within two years.”

The second goal provides direction.

Successful savers often break large goals into smaller milestones.

This makes progress visible and keeps motivation high.

Habit #5: They Separate Wants From Needs

One of the most powerful financial skills is distinguishing between needs and wants.

Needs include:

- Housing

- Food

- Transportation

- Healthcare

- Utilities

Wants include:

- Luxury upgrades

- Premium memberships

- Frequent dining out

- Impulse purchases

- Trend-driven spending

People who struggle to save often blur the line between the two.

Successful savers evaluate purchases carefully.

Before spending money, they frequently ask: why some people always have money saved

- Do I need this?

- Will this improve my life meaningfully?

- Would I rather have this item or reach my financial goal?

These simple questions prevent countless unnecessary purchases.

Habit #6: They Build Emergency Funds Early

Common examples include:

- Medical bills

- Vehicle repairs

- Home maintenance

- Temporary job loss

- Family emergencies

People without emergency funds often rely on:

- Credit cards

- Personal loans

- Borrowing from family

As a result, temporary problems become long-term financial burdens.

Successful savers prioritize emergency funds because they understand one simple truth:

Financial emergencies are not a matter of if—they are a matter of when.

An emergency fund acts as a financial safety net. It provides protection against unexpected events and prevents minor setbacks from becoming major financial crises.

Even a modest emergency fund creates:

- Greater security

- Less stress

- Reduced debt risk

- Better financial flexibility

- Increased financial confidence

Many financial experts recommend maintaining three to six months of essential living expenses. However, the most important step is simply getting started. Even a small emergency fund can make a significant difference when unexpected costs arise.

Over time, emergency savings provide peace of mind and allow individuals to handle financial surprises without disrupting their long-term goals.

Habit #7: They Make Saving Automatic

Successful savers rarely keep all of their savings in a single account without a plan.

Instead, they organize savings around specific financial goals.

Common savings goals include:

- Emergency funds

- Home down payments

- Vacation funds

- Education expenses

- Vehicle purchases

- Retirement savings

When money has a clear purpose, people are often more motivated to save consistently.

For example, saving for a “Future Home Fund” feels more meaningful than simply placing money into a general savings account.

Many successful savers create separate accounts for different objectives. This approach helps track progress and reduces the temptation to spend money intended for important goals.

Goal-based saving systems also make financial planning easier because individuals can clearly see:

- How much they have saved

- How much more they need

- How quickly they are progressing

As milestones are reached, motivation increases and saving becomes more rewarding.

Rather than viewing saving as a sacrifice, goal-based savers view it as a direct investment in their future plans and priorities.

Habit #8: They Are Comfortable Delaying Gratification

One characteristic appears repeatedly among financially successful people:

They are willing to wait.

They understand that sacrificing a small reward today can create a much larger reward tomorrow.

Examples include:

- Saving for purchases instead of financing them

- Investing rather than spending

- Building emergency funds before upgrading lifestyles

Delayed gratification is not about deprivation.

It is about prioritization.

Successful savers focus on long-term outcomes rather than short-term impulses.

Habit #9: They Avoid Comparison Spending

Social media has transformed spending behavior.

Every day people see:

- Luxury vacations

- Expensive vehicles

- Designer products

- Influencer lifestyles

Unfortunately, many people compare their real lives to carefully curated online content.

This often leads to:

- Impulse purchases

- Lifestyle inflation

- Financial stress

Successful savers recognize that appearances can be misleading.

Many wealthy individuals live below their means.

Many people who appear wealthy are heavily in debt.

Understanding this distinction helps savers focus on their own goals rather than external pressure.

Habit #10: They Think Long Term

People who consistently save money tend to think differently about time.

Instead of asking:

“What do I want today?”

They ask:

“What do I want five years from now?”

This shift in perspective changes financial decisions dramatically.

Long-term thinkers are more likely to:

- Invest consistently

- Build retirement savings

- Avoid unnecessary debt

- Maintain financial discipline

They understand that wealth is usually built gradually rather than suddenly.

read also: The Simple Budgeting Mistake That Costs People Thousands Every Year

Why Modern Spending Traps Are Stronger Than Ever

Saving money in 2026 presents unique challenges.

Consumers face constant spending triggers: why some people always have money saved

Subscription Culture

Monthly subscriptions often appear inexpensive individually.

Combined, they can cost hundreds or thousands of dollars annually.

One-Click Purchasing

Buying products requires almost no effort.

Convenience encourages impulse spending.

Personalized Advertising

Algorithms analyze behavior and deliver highly targeted ads.

Consumers see products specifically designed to attract their attention.

Buy Now, Pay Later Services

These services reduce the immediate pain of spending.

However, they can encourage purchases people otherwise would not make.

Successful savers understand these traps and create boundaries around spending.

Five Common Mistakes People Make When Trying to Save

Mistake #1: Waiting Until the End of the Month

Most people save whatever remains.

Successful savers save first.

Mistake #2: Setting Unrealistic Goals

Extreme savings targets often fail quickly.

Small, sustainable goals produce better long-term results.

Mistake #3: Ignoring Small Expenses

Small purchases accumulate over time.

Many financial leaks begin with seemingly harmless spending.

Mistake #4: Not Tracking Progress

Without measurement, improvement becomes difficult.

Tracking provides accountability.

Mistake #5: Focusing Only on Income

Increasing income helps.

However, spending behavior remains equally important.

A person earning more can still struggle financially if spending rises faster than earnings.

Expert Tips for Building Savings Faster

Use Multiple Savings Accounts

Separate goals create clarity.

Examples:

- Emergency fund account

- Vacation fund account

- Home purchase account

Increase Savings After Every Raise

Whenever income increases:

- Save part of the increase

- Invest part of the increase

- Spend only a portion

Perform Monthly Financial Reviews

Review:

- Spending habits

- Savings progress

- Debt balances

- Financial goals

Small adjustments prevent larger problems.

Create Spending Rules

Examples:

- Wait 24 hours before major purchases

- Set monthly discretionary spending limits

- Avoid emotional shopping

Rules reduce impulsive decisions.

Myths vs Facts About Saving Money

Many people struggle financially because they believe common money myths that sound reasonable but are often inaccurate. Understanding the difference between myths and reality can dramatically improve financial decision-making.

Myth #1: You Need a High Income to Save Money

Fact:

Income helps, but saving is primarily a behavior.

Many high-income earners save very little because their spending rises alongside their earnings. At the same time, countless middle-income households build substantial savings through consistent financial habits.

Saving success depends more on discipline than salary.

Myth #2: Small Savings Don’t Matter

Fact:

Small amounts saved consistently can create impressive results over time.

For example:

- Saving $5 per day

- Approximately $150 per month

- Approximately $1,800 per year

Over several years, these small savings can become a significant financial resource.

Wealth often grows from small actions repeated consistently.

Myth #3: Budgeting Means Giving Up Everything Fun

Fact:

A good budget does not eliminate enjoyment.

Instead, it helps people spend intentionally.

Budgeting allows individuals to:

- Enjoy entertainment

- Travel responsibly

- Spend on hobbies

- Reach financial goals

The purpose of budgeting is control, not restriction.

Myth #4: I’ll Start Saving When I Earn More

Fact:

People who cannot save a small percentage of their income often struggle to save larger amounts later.

Waiting for future income increases frequently delays financial progress indefinitely.

The best time to develop saving habits is now.

Myth #5: Emergency Funds Are Only for Major Crises

Fact:

Emergency funds help with both large and small unexpected expenses.

Examples include:

- Vehicle repairs

- Medical expenses

- Home maintenance

- Temporary income interruptions

Even modest emergency savings can prevent debt and reduce financial stress.

Frequently Asked Questions

1. How much money should I save every month?

A common guideline is saving at least 20% of income whenever possible. However, the ideal amount depends on your income, expenses, debt obligations, and financial goals.

The most important factor is consistency rather than a specific percentage.

2. What is the best way to start saving if I live paycheck to paycheck?

Begin by tracking expenses for one month.

Most people discover small spending areas that can be reduced.

Even saving a small amount regularly creates momentum and helps establish positive habits.

3. Should I save money or pay off debt first?

The answer depends on the type of debt.

Generally:

- Build a small emergency fund first.

- Then prioritize high-interest debt.

- Continue contributing to savings simultaneously when possible.

Balancing both goals often produces the strongest financial results. why some people always have money saved

4. How large should an emergency fund be?

Many financial experts recommend maintaining:

- Three to six months of essential living expenses.

However, building even $500 to $1,000 in emergency savings can provide meaningful protection against unexpected expenses.

5. Why do some people save easily while others struggle?

The difference often comes down to:

- Financial habits

- Spending behavior

- Goal setting

- Planning systems

- Long-term thinking

Saving is usually more behavioral than mathematical.

read also: How Banks Really Decide Who Gets a Personal Loan in 2026

6. Is investing more important than saving?

Both are important, but they serve different purposes in a healthy financial plan.

Savings provide short-term security, while investments help build long-term wealth.

Savings are typically used for:

- Emergency funds

- Unexpected expenses

- Short-term financial goals

- Major upcoming purchases

Because savings are usually kept in easily accessible accounts, the money remains available when needed.

Investments, on the other hand, are designed to help money grow over time. They are often used for:

- Retirement planning

- Long-term wealth building

- Future financial independence

- Achieving major life goals

While investments have the potential to generate higher returns, they also involve some level of risk and may fluctuate in value.

For most people, building a solid emergency fund should come before investing heavily. Having savings available for emergencies can prevent the need to sell investments during unfavorable market conditions or rely on high-interest debt.

The most effective financial strategy is usually not choosing one over the other. Instead, it involves maintaining adequate savings for short-term security while investing consistently for long-term growth.

A balanced approach allows individuals to handle today’s financial needs while preparing for tomorrow’s opportunities.

7. Can small financial habits really make a difference?

Small financial habits may seem insignificant in the moment, but their impact grows substantially over time. Many people focus on major financial decisions such as buying a home, changing jobs, or making large investments. While these decisions are important, daily financial choices often have an even greater long-term effect.

For example: why some people always have money saved

- Saving $5 per day can add up to approximately $1,800 per year.

- Reducing unnecessary subscriptions can save hundreds of dollars annually.

- Investing a small amount consistently each month can grow significantly through compound growth.

The key is consistency. A positive financial habit repeated hundreds of times each year creates meaningful results. Similarly, small spending mistakes repeated regularly can quietly drain thousands of dollars over time.

Successful savers understand that wealth is rarely built through one extraordinary action. Instead, it is usually the result of small, smart financial decisions made consistently over many years.

That is why tracking expenses, saving automatically, avoiding impulse purchases, and contributing regularly to savings or investments can have a powerful impact on long-term financial success.

8. What is the biggest mistake people make with money?

One of the most common financial mistakes is spending first and saving later.

Many people tell themselves they will save whatever money remains at the end of the month. Unfortunately, after paying bills, covering daily expenses, and making discretionary purchases, there is often very little left to save.

As a result, saving becomes inconsistent and financial goals are repeatedly postponed.

Successful savers typically reverse this process. Instead of treating savings as an afterthought, they make it a priority. They save first and then adjust their spending based on what remains.

This approach helps create:

- Consistent savings growth

- Stronger emergency funds

- Better financial discipline

- Reduced dependence on debt

- Greater long-term financial security

Another reason this mistake is so costly is that it often goes unnoticed. Small daily purchases, recurring subscriptions, impulse spending, and lifestyle inflation gradually consume income without attracting much attention.

Over months and years, these spending habits can prevent people from building wealth, investing for the future, or achieving important financial goals.

The most effective solution is to create a system that automatically prioritizes savings. Whether through automatic transfers, payroll deductions, or scheduled investment contributions, paying yourself first ensures that saving happens consistently regardless of monthly spending patterns.

In many cases, the difference between financial stress and financial security is not how much money a person earns, but whether they save before they spend.

The Hidden Psychology Behind Successful Saving

Financial success is often viewed as a numbers problem.

In reality, it is frequently a psychology problem.

People who save consistently tend to develop a different relationship with money.

They view savings as:

- Protection

- Freedom

- Opportunity

- Security

Rather than seeing saving as a sacrifice, they see it as purchasing future options.

This mindset shift changes behavior dramatically.

Every dollar saved becomes a tool that increases flexibility and reduces dependence on debt.

Over time, this perspective strengthens financial confidence and supports better decision-making.

Why Financial Freedom Begins With Savings

Many people associate financial freedom with becoming wealthy.

In reality, financial freedom often begins much earlier.

A person with:

- No consumer debt

- A strong emergency fund

- Consistent savings habits

may experience greater financial freedom than someone earning significantly more but carrying substantial debt.

Savings create choices.

Choices create freedom.

Freedom reduces financial stress.

This cycle explains why consistent savers often feel more secure regardless of income level.

read also: Loan Approval Process 2026: Hidden Factors Banks Never Explain

| Financial Habit | People Who Struggle to Save | People Who Consistently Save |

|---|---|---|

| Saving Strategy | Save whatever remains | Save first, spend later |

| Budgeting | Rarely follows a budget | Reviews budget regularly |

| Expense Tracking | Estimates spending | Tracks expenses consistently |

| Income Increases | Increase lifestyle spending | Increase savings and investments |

| Emergency Fund | Often unavailable | Maintains emergency savings |

| Financial Goals | Vague or undefined | Specific and measurable |

| Debt Management | Relies on credit frequently | Avoids unnecessary debt |

| Spending Decisions | Impulsive and emotional | Planned and intentional |

| Long-Term Planning | Focuses on current needs | Focuses on future financial security |

| Investment Habits | Delays investing | Invests consistently over time |

| Response to Emergencies | Uses loans or credit cards | Uses emergency savings |

| Money Mindset | Short-term gratification | Long-term wealth building |

Final Thoughts: Why Some People Always Have Money Saved—and Others Don’t

The difference between people who consistently save money and those who constantly struggle is rarely luck.

It is rarely intelligence.

And it is not always income.

More often, the difference comes from habits.

People who build savings successfully:

- Pay themselves first

- Track their spending

- Avoid lifestyle inflation

- Set clear financial goals

- Build emergency funds

- Automate good financial behavior

- Think long term

- Resist comparison spending

None of these habits require extraordinary wealth.

They require consistency. why some people always have money saved

Small financial decisions made repeatedly over time create dramatically different outcomes.

The encouraging reality is that anyone can begin improving these habits today.

You do not need a perfect budget.

You do not need a six-figure salary.

You do not need financial expertise.

You simply need a willingness to make slightly better financial decisions than you made yesterday.

Over months and years, those decisions compound.

And eventually, they become the reason you always have money saved when others do not.