Introduction

Most people believe financial success depends on earning more money. While increasing income can certainly improve financial stability, the reality is that many individuals lose thousands of dollars every year because of hidden money habits they barely notice. These habits often develop gradually and become part of everyday life, making them difficult to identify without careful financial review.

In 2026, managing money has become more convenient than ever. Mobile banking, digital wallets, subscription services, online shopping platforms, and instant payment systems allow consumers to spend money within seconds. Although these innovations offer convenience, they also make it easier to develop spending behaviors that silently damage financial health.

The most dangerous money habits are not always obvious. Few people intentionally waste money. Instead, small daily decisions accumulate over time and create significant financial consequences. A recurring subscription, an impulse purchase, a daily convenience expense, or a neglected savings opportunity may seem insignificant today. However, when repeated over months and years, these behaviors can quietly drain thousands of dollars from your finances.

Financial success is rarely determined by one major decision. More often, it is shaped by hundreds of small choices made consistently over time. Understanding these hidden habits can help you identify financial leaks, improve money management, and build a stronger financial future.

This guide explores the hidden money habits that quietly cost people thousands every year and provides practical strategies to avoid them.

Why Small Financial Habits Matter More Than Big Financial Decisions

Many people focus heavily on large financial decisions such as:

- Buying a home

- Purchasing a vehicle

- Applying for a loan

- Selecting insurance coverage

- Choosing investment products

While these decisions are important, small daily financial habits often have a greater cumulative impact on long-term wealth.

Consider two individuals earning the same salary.

The first person:

- Tracks expenses regularly

- Saves consistently

- Avoids unnecessary spending

- Reviews financial goals monthly

The second person:

- Makes frequent impulse purchases

- Ignores subscriptions

- Saves inconsistently

- Rarely reviews spending habits

After several years, the financial outcomes may be dramatically different despite identical incomes.

The reason is simple. Wealth is often built through consistent financial discipline rather than occasional financial decisions.

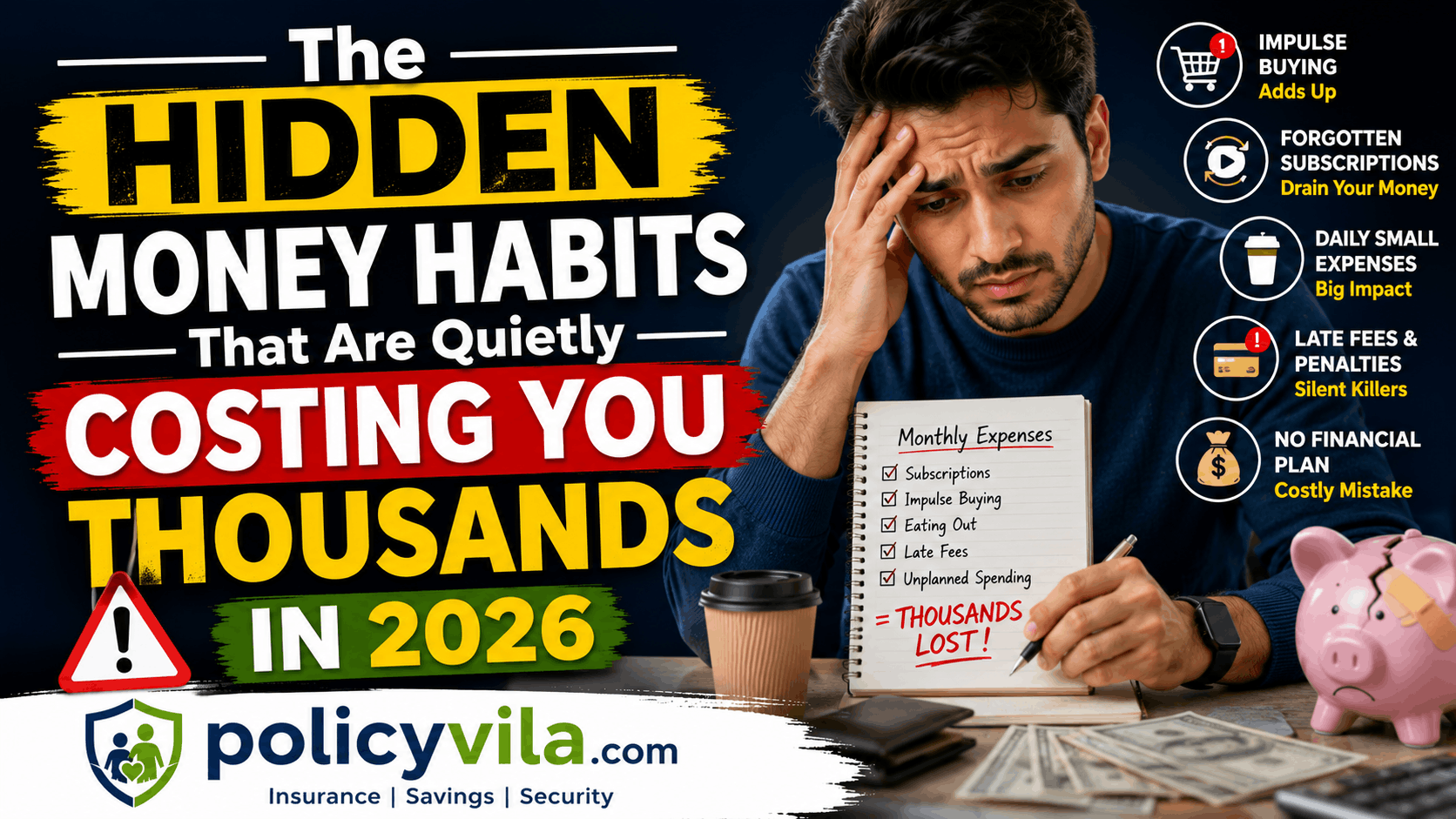

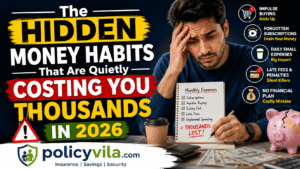

Hidden Money Habit #1: Ignoring Small Daily Purchases

One of the most overlooked financial habits is ignoring the impact of small daily purchases. While a single purchase may seem insignificant, repeated spending over weeks, months, and years can quietly consume a large portion of your income.

Many people pay close attention to major expenses such as rent, loan payments, and insurance premiums. However, they often overlook small everyday transactions that gradually add up. Because these purchases are relatively inexpensive, they rarely trigger concern. Unfortunately, their long-term financial impact can be substantial.

Common examples include:

- Daily coffee purchases

- Convenience store snacks

- Food delivery service fees

- Ride-sharing upgrades

- Mobile app subscriptions

- Impulse online purchases

Individually, these expenses may appear harmless. However, when combined and repeated consistently, they can cost thousands of dollars every year.

For example, purchasing a $5 coffee each day may not seem like a major expense. Yet over time, the numbers become much larger:

- Daily cost: $5

- Monthly cost: Approximately $150

- Annual cost: Approximately $1,800

Likewise, spending just $10 per day on convenience purchases can have an even greater impact:

- Daily cost: $10

- Monthly cost: Approximately $300

- Annual cost: Approximately $3,600

Most people never calculate these totals, which is why this hidden money habit continues unnoticed. Small expenses often feel manageable because they do not create immediate financial pressure. Nevertheless, they slowly reduce savings potential and limit progress toward financial goals.

Why This Habit Develops

Several factors make small purchases difficult to notice.

Low Individual Cost

Because each transaction is relatively inexpensive, people assume it has little effect on their finances.

Frequent Transactions

Daily purchases quickly become routine habits. Once spending becomes automatic, it often escapes attention.

Digital Payment Convenience

Mobile wallets, contactless payments, and online transactions reduce the psychological impact of spending money. As a result, consumers may spend more without realizing it.

Instant Gratification

Small purchases often provide immediate enjoyment or convenience. This short-term satisfaction can make it difficult to recognize the long-term financial cost.

The Long-Term Impact

Ignoring small daily expenses can lead to:

- Reduced savings

- Slower debt repayment

- Smaller investment contributions

- Increased financial stress

- Delayed financial goals

Over several years, these seemingly harmless expenses can represent thousands of dollars that could have been used to build wealth or improve financial security.

How to Fix This Money Habit

The goal is not necessarily to eliminate every small purchase. Instead, the objective is to become more aware of spending patterns and make intentional financial decisions.

Helpful strategies include:

- Track daily expenses consistently

- Set monthly discretionary spending limits

- Review bank and credit card statements regularly

- Identify recurring spending patterns

- Reduce unnecessary convenience purchases

- Create savings goals that motivate better decisions

Awareness is often the first step toward financial improvement. Once people understand where their money is going, they can make smarter choices and keep more of their income working toward their long-term financial goals.

Hidden Money Habit #2: Subscription Overload

Subscription services have become a normal part of everyday life. From entertainment and music streaming to cloud storage and productivity tools, consumers now pay for dozens of services through convenient monthly or annual subscriptions. While these services often provide value, they can also become a hidden financial drain when left unchecked.

The issue is not necessarily the subscriptions themselves. The real problem occurs when people lose track of how many active subscriptions they have and continue paying for services they rarely use.

Today, consumers commonly subscribe to:

- Video streaming platforms

- Music streaming services

- Cloud storage plans

- Fitness applications

- Productivity software

- News and magazine memberships

- Online learning platforms

- Gaming subscriptions

Because most subscriptions are charged automatically, they often go unnoticed after the initial sign-up. As a result, many people continue paying for services long after they stop using them regularly.

How Small Subscription Costs Add Up

A single subscription costing $10 per month may seem affordable and harmless.

However, consider the following example:

- Five subscriptions at $10 each

- Monthly cost: $50

- Annual cost: $600

Now imagine adding a few premium services:

- Two subscriptions at $20 each

- Monthly cost: $40

- Annual cost: $480

Combined, these subscriptions could cost over $1,000 per year without providing meaningful value.

Many consumers are surprised when they calculate the total amount spent on subscriptions over a twelve-month period.

Why Subscription Overload Happens

Several factors contribute to subscription overload.

Automatic Renewals

Most subscription services renew automatically. Since payments happen in the background, consumers often forget they are being charged.

Free Trial Conversions

Many people sign up for free trials and forget to cancel before billing begins.

Low Monthly Costs

Individual subscriptions appear inexpensive, making them easier to justify and overlook.

Multiple Similar Services

Consumers sometimes subscribe to several platforms that offer nearly identical content or benefits.

Warning Signs of Subscription Overload

You may be experiencing subscription overload if:

- You cannot list all active subscriptions

- Multiple services serve the same purpose

- Automatic payments occur without your awareness

- You rarely use certain platforms

- Subscription costs continue increasing each year

- You discover charges you forgot about

If any of these situations sound familiar, it may be time for a subscription review.

The Financial Impact

Subscription overload may seem minor, but the long-term cost can be significant.

Unused subscriptions can:

- Reduce monthly savings

- Limit investment opportunities

- Increase unnecessary spending

- Slow financial progress

- Create hidden budget leaks

Over several years, these recurring charges can amount to thousands of dollars that could have been directed toward more important financial goals.

How to Fix Subscription Overload

Fortunately, subscription overload is one of the easiest money habits to correct.

Start by reviewing:

- Bank statements

- Credit card statements

- Mobile app subscriptions

- Online account billing settings

Then ask yourself:

- Do I still use this service regularly?

- Is this subscription providing enough value?

- Can I find a cheaper alternative?

- Do I have another service that offers similar benefits?

Canceling even a few unused subscriptions can immediately improve your monthly cash flow.

Build a Subscription Review Habit

Financially successful individuals often review subscriptions every month or quarter.

This simple habit helps:

- Eliminate waste

- Improve budgeting accuracy

- Increase savings

- Maintain better financial awareness

Even a small reduction in subscription spending can create meaningful long-term financial benefits.

Hidden Money Habit #3: Lifestyle Inflation

Lifestyle inflation is one of the most common yet overlooked money habits that quietly prevent people from building wealth. It occurs when spending increases every time income increases. While earning more money should improve financial security, many individuals find themselves in the same financial position year after year because their expenses rise alongside their earnings.

At first, lifestyle inflation may seem harmless. After all, it is natural to enjoy the benefits of a promotion, salary increase, bonus, or business growth. However, when every increase in income is matched by higher spending, financial progress becomes difficult.

For example:

- Salary increases

- Monthly spending increases immediately

- Savings remain unchanged

- Investments receive no additional contributions

As a result, income grows while wealth remains stagnant.

Common Signs of Lifestyle Inflation

Lifestyle inflation often develops gradually and can be difficult to notice. Many people adjust their spending habits without realizing the long-term financial consequences.

Common examples include:

- Dining at more expensive restaurants

- Purchasing luxury items more frequently

- Upgrading to premium subscriptions and memberships

- Buying newer and more expensive vehicles

- Moving into larger homes with higher expenses

- Increasing entertainment and travel spending

Although each upgrade may seem reasonable individually, the combined effect can significantly increase monthly expenses.

Why Lifestyle Inflation Is Dangerous

The biggest problem with lifestyle inflation is that it creates the illusion of financial success.

Income rises.

However:

- Savings stay the same

- Emergency funds grow slowly

- Investments remain underfunded

- Financial security improves very little

Many high-income earners experience financial stress despite earning excellent salaries because their spending expands to match their income.

Consequently, they may struggle to achieve important financial goals such as:

- Early retirement

- Home ownership

- Debt freedom

- Investment growth

- Long-term wealth accumulation

The Opportunity Cost of Lifestyle Inflation

Every additional dollar spent on lifestyle upgrades is a dollar that cannot be used for wealth-building activities.

For example, spending an extra $500 per month on lifestyle improvements equals:

- $6,000 per year

- $30,000 over five years

Without considering potential investment growth.

When viewed from this perspective, lifestyle inflation can become extremely expensive over time.

Why People Fall Into This Trap

Several psychological factors contribute to lifestyle inflation.

Rewarding Success

People naturally want to reward themselves after achieving career or financial milestones.

Social Comparison

Friends, coworkers, and social media influencers often create pressure to maintain a certain lifestyle.

Easy Access to Credit

Credit cards and financing options make expensive purchases appear more affordable than they actually are.

Gradual Spending Increases

Lifestyle inflation usually happens slowly, making it difficult to recognize until expenses have already increased substantially.

How to Prevent Lifestyle Inflation

The goal is not to avoid enjoying higher income. Instead, the goal is to balance lifestyle improvements with financial growth.

When income increases:

- Automatically save a percentage of the raise

- Increase investment contributions

- Add money to emergency savings

- Pay down existing debt

- Avoid upgrading every aspect of your lifestyle immediately

A useful strategy is the 50/50 Rule, where half of every pay increase goes toward financial goals and the other half can be used for lifestyle improvements.

Build Wealth Before Expanding Your Lifestyle

Financially successful individuals often prioritize:

- Saving first

- Investing consistently

- Building emergency funds

- Maintaining spending discipline

Only after strengthening their financial foundation do they increase discretionary spending.

This approach allows income growth to create real financial progress instead of simply supporting a more expensive lifestyle.

Hidden Money Habit #4: Emotional Spending

One of the most expensive hidden money habits is emotional spending. Unlike planned purchases that serve a specific purpose, emotional spending happens when people buy things primarily because of how they feel rather than what they need. While occasional emotional purchases may seem harmless, repeated emotional spending can quietly damage a person’s financial health over time.

In today’s digital environment, shopping has become incredibly convenient. Consumers can purchase products, subscribe to services, or order food within seconds using a smartphone. As a result, emotions often influence spending decisions before logic has a chance to intervene.

Emotional spending commonly occurs when people experience:

- Stress from work

- Relationship difficulties

- Anxiety or frustration

- Feelings of boredom

- Excitement after good news

- Celebrations and special occasions

- Social pressure from friends or social media

Although buying something new may provide a temporary boost in mood, the feeling rarely lasts. Unfortunately, the financial consequences often remain long after the emotional satisfaction disappears.

Why Emotional Spending Happens

Humans naturally seek activities that provide comfort and pleasure. Shopping can create a short-term feeling of reward because the brain releases chemicals associated with satisfaction and enjoyment.

Consequently, spending money may temporarily help people:

- Escape stress

- Feel more successful

- Improve their mood

- Reward themselves

- Gain a sense of control

However, because the underlying problem remains unresolved, the desire to spend may return repeatedly.

Common Signs of Emotional Spending

Many people engage in emotional spending without realizing it. Recognizing the warning signs is the first step toward improving financial habits.

You may be spending emotionally if:

- You shop when feeling stressed or upset

- You purchase items you do not truly need

- You frequently make impulse purchases

- You feel guilty after spending money

- Shopping improves your mood temporarily

- You justify unnecessary purchases repeatedly

- You hide purchases from family members

- You struggle to remember why you bought certain items

If several of these signs apply to you, emotional spending may be affecting your finances more than you realize.

The Financial Cost of Emotional Spending

The financial impact of emotional spending often develops gradually.

For example:

- A $50 impulse purchase each week

- Approximately $200 per month

- Approximately $2,400 per year

Many people never calculate the annual cost of these emotional purchases. As a result, they underestimate how much money could have been saved, invested, or used to achieve important financial goals.

Over time, emotional spending can contribute to:

- Increased credit card balances

- Reduced savings

- Budgeting difficulties

- Financial stress

- Delayed financial goals

Social Media and Emotional Spending

Social media platforms have amplified emotional spending in recent years.

Consumers are constantly exposed to:

- Influencer recommendations

- Luxury lifestyles

- Targeted advertisements

- Limited-time offers

- Product promotions

These messages often create feelings of comparison and urgency.

Consequently, people may purchase products not because they need them, but because they feel pressure to keep up with others.

How to Control Emotional Spending

The good news is that emotional spending can be managed with awareness and discipline.

Before making non-essential purchases:

Use the 24-Hour Rule

Wait at least 24 hours before completing the purchase.

This delay often reduces impulse buying and encourages rational decision-making.

Ask Important Questions

Before spending money, ask yourself:

- Do I truly need this item?

- Will I still want it next week?

- Am I buying this because of an emotion?

- Does this purchase support my financial goals?

Identify Emotional Triggers

Pay attention to situations that encourage spending.

For example:

- Stressful workdays

- Bored weekends

- Social media browsing

- Celebrations

Understanding triggers helps prevent automatic spending behavior.

Find Alternative Activities

Instead of shopping, consider:

- Exercise

- Reading

- Walking outdoors

- Spending time with family

- Practicing hobbies

- Meditation or relaxation techniques

These activities often provide emotional relief without creating financial consequences.

Build Mindful Spending Habits

Mindful spending involves making intentional financial decisions rather than reacting emotionally.

Financially successful individuals often:

- Create spending plans

- Set monthly limits

- Track discretionary expenses

- Align purchases with personal goals

As a result, they maintain greater control over their finances while still enjoying life responsibly.

Hidden Money Habit #5: Ignoring Emergency Savings

One of the most costly financial habits people develop is neglecting to build an emergency fund. While saving money may not seem urgent when life is running smoothly, unexpected expenses can appear at any time. Without adequate savings, even a relatively small financial emergency can quickly turn into a major financial setback.

Many individuals focus on paying bills and managing day-to-day expenses while postponing emergency savings for a later date. Unfortunately, emergencies rarely wait until the perfect time. As a result, people without emergency funds often find themselves relying on debt to cover unexpected costs.

Common financial emergencies include:

- Medical expenses

- Vehicle repairs

- Home maintenance issues

- Job loss or reduced income

- Family emergencies

- Unexpected travel costs

- Major appliance replacements

Although these situations are common, many households remain financially unprepared when they occur. Hidden Money Habits

What Happens Without Emergency Savings?

When an unexpected expense arises, people without savings often turn to alternative funding sources such as:

- Credit cards

- Personal loans

- Payday loans

- Borrowing from friends or family

- High-interest financing options

While these solutions may provide temporary relief, they frequently create additional financial challenges. A short-term emergency can quickly become a long-term debt problem when interest charges and repayment obligations accumulate.

For example, a $1,000 emergency expense paid with a high-interest credit card may eventually cost significantly more if the balance is not paid quickly.

Why Emergency Funds Matter

An emergency fund acts as a financial safety net. Instead of relying on debt, individuals can use their savings to handle unexpected situations without disrupting their long-term financial goals.

Emergency savings provide several important benefits:

Financial Security

Knowing that money is available for unexpected expenses creates greater confidence and peace of mind.

Reduced Stress

Financial emergencies are stressful enough without worrying about how to pay for them. Savings help reduce that pressure.

Greater Financial Flexibility

An emergency fund provides options during difficult situations, allowing individuals to make better financial decisions.

Protection Against Debt

Perhaps the biggest advantage is avoiding unnecessary borrowing and high-interest debt.

The True Cost of Ignoring Emergency Savings

Many people underestimate the financial consequences of not having an emergency fund.

Without savings, a single unexpected expense can lead to:

- Credit card debt

- Missed bill payments

- Loan applications

- Damaged financial stability

- Increased financial stress

Over time, repeated emergencies financed through debt can significantly slow wealth-building progress.

How Much Should You Save?

Financial experts often recommend maintaining an emergency fund equal to:

- Three to six months of essential living expenses

Essential expenses generally include:

- Housing costs

- Utilities

- Food

- Transportation

- Insurance

- Minimum debt payments

However, the ideal amount varies based on personal circumstances, income stability, and family responsibilities.

Start Small and Build Consistently

One of the biggest mistakes people make is believing they need to save thousands of dollars immediately.

In reality, every emergency fund starts with a small first step.

Consider beginning with goals such as: Hidden Money Habits

- $500 emergency savings

- $1,000 emergency fund

- One month of expenses

- Three months of expenses

Small, consistent contributions often produce better results than waiting for the perfect opportunity to save.

Simple Ways to Build an Emergency Fund

Building emergency savings does not have to be complicated.

Effective strategies include:

- Setting up automatic transfers

- Saving part of every paycheck

- Using bonuses and tax refunds wisely

- Reducing unnecessary spending

- Redirecting canceled subscription payments into savings

Even modest contributions can grow significantly over time.

Make Emergency Savings a Financial Priority

Financially successful individuals treat emergency savings as a necessity rather than an option. Instead of saving whatever remains after spending, they allocate money to savings first and adjust spending accordingly.

This habit creates a stronger financial foundation and reduces dependence on debt when unexpected expenses occur.

Hidden Money Habit #6: Carrying High-Interest Debt

High-interest debt is one of the most significant barriers to achieving long-term financial success. While borrowing money can sometimes be necessary, carrying debt with high interest rates can quietly drain your finances and make it difficult to build wealth. Many people underestimate how quickly interest charges accumulate, resulting in a financial burden that becomes increasingly difficult to manage over time.

Common forms of high-interest debt include:

- Credit card balances

- Payday loans

- Short-term personal loans

- Buy-now-pay-later balances

- Certain unsecured consumer loans

The primary problem with high-interest debt is that interest compounds over time. This means borrowers often pay far more than the original amount borrowed.

For example:

- Outstanding balance: $5,000

- High interest rate applied monthly

- Hundreds or even thousands of dollars in additional interest charges over several years

Without an effective repayment strategy, debt can continue growing even when regular payments are being made.

Why High-Interest Debt Is So Dangerous

High-interest debt affects more than just monthly cash flow. It can have a long-term impact on overall financial health and limit future opportunities.

Reduces Savings Potential

Money spent on interest payments cannot be directed toward savings goals. As a result, building an emergency fund or achieving financial milestones becomes more difficult.

Limits Investment Growth

Every dollar used to pay interest is a dollar that cannot be invested. Over time, missed investment opportunities can significantly reduce wealth accumulation.

Restricts Financial Flexibility

High debt obligations leave less room in the budget for unexpected expenses, career changes, travel, or other important life goals.

Increases Financial Stress

Constant debt payments can create anxiety and financial pressure, particularly when balances continue to grow despite regular payments.

The Hidden Cost of Minimum Payments

Many borrowers make only the minimum required payment on their debt.

While this keeps accounts current, it often extends repayment periods significantly and increases the total amount of interest paid.

For example:

- Large balance

- High interest rate

- Minimum monthly payment

This combination can result in years of repayment and substantial interest costs.

The longer debt remains outstanding, the more expensive it becomes.

Signs That Debt Is Becoming a Problem

You may need to take action if:

- Credit card balances increase each month

- Minimum payments consume a large portion of income

- New debt is used to pay existing debt

- Savings contributions have stopped

- Financial stress is increasing

Recognizing these warning signs early can prevent more serious financial problems later.

How to Reduce High-Interest Debt Faster

The good news is that debt can be reduced systematically with a clear plan and consistent effort.

Pay More Than the Minimum

Making larger payments helps reduce principal balances faster and lowers total interest costs.

Prioritize High-Interest Balances

Focus extra payments on debts with the highest interest rates while maintaining minimum payments on other obligations.

This strategy often reduces overall borrowing costs more quickly.

Avoid New Unnecessary Debt

Reducing debt becomes much harder when new balances are added regularly.

Avoid impulse purchases and unnecessary borrowing whenever possible.

Create a Structured Repayment Plan

A written debt repayment strategy provides direction and accountability.

Include:

- Current balances

- Interest rates

- Monthly payment goals

- Target payoff dates

Tracking progress helps maintain motivation and consistency.

Debt Freedom Creates Financial Opportunities

As debt balances decrease, more money becomes available for:

- Emergency savings

- Investments

- Retirement planning

- Major financial goals

- Lifestyle improvements

Many people experience significant financial relief once high-interest debt is eliminated.

Build Better Borrowing Habits

Financially successful individuals typically use debt carefully and strategically. They understand the true cost of interest and avoid carrying balances longer than necessary.

Healthy borrowing habits include:

- Paying bills on time

- Keeping debt manageable

- Monitoring credit regularly

- Borrowing only when necessary

- Prioritizing repayment

These habits help protect long-term financial health.

Hidden Money Habit #7: Not Tracking Expenses

One of the most common reasons people struggle to achieve their financial goals is simply not knowing where their money goes. Many individuals believe they have a good understanding of their spending habits, but in reality, estimates are often inaccurate. Without proper expense tracking, small purchases, recurring charges, and unnecessary spending can quietly consume a significant portion of income.

Expense tracking is not about restricting spending. Instead, it is about gaining visibility into financial behavior. When people understand exactly where their money is going, they can make better financial decisions and identify opportunities to improve their finances.

Why Expense Tracking Matters

Many financial problems begin with a lack of awareness.

Without tracking expenses:

- Overspending often goes unnoticed

- Budget leaks remain hidden

- Savings opportunities are missed

- Financial goals become harder to achieve

- Debt may increase unexpectedly

Even individuals with high incomes can experience financial difficulties if they fail to monitor spending regularly.

The Hidden Cost of Not Tracking Spending

Consider someone who spends small amounts throughout the week without paying attention.

Examples may include:

- Coffee purchases

- Food delivery orders

- Online shopping

- Convenience store purchases

- Subscription renewals

Individually, these transactions may appear insignificant. However, without tracking them, the total monthly cost can be surprisingly high.

Many people are shocked when they review their bank statements and discover how much money has been spent on non-essential items.

Benefits of Expense Tracking

Tracking expenses consistently offers several advantages.

Identifies Wasteful Spending

Expense tracking helps reveal spending habits that may be preventing financial progress.

For example:

- Frequent impulse purchases

- Unused subscriptions

- Excessive dining out

- Unnecessary convenience fees

Once identified, these expenses can often be reduced or eliminated.

Improves Budget Accuracy

A budget is only effective when it reflects actual spending behavior.

Tracking expenses allows individuals to create realistic budgets based on real financial data rather than estimates.

Increases Savings Potential

When spending patterns become visible, it becomes easier to redirect money toward savings and investments.

Small adjustments can create significant long-term results.

Supports Financial Goals

Whether the goal is:

- Buying a home

- Building an emergency fund

- Paying off debt

- Saving for retirement

Expense tracking helps ensure that spending decisions align with financial priorities.

Why People Avoid Tracking Expenses

Despite its benefits, many people avoid monitoring their finances.

Common reasons include:

- Believing it takes too much time

- Fear of discovering overspending

- Lack of financial organization

- Assuming they already know their spending habits

Fortunately, modern technology has made expense tracking easier than ever.

Easy Ways to Track Spending

There is no single correct method for tracking expenses. The best system is the one that can be maintained consistently.

Popular options include:

Budgeting Apps

Financial apps automatically categorize transactions and provide spending reports.

Bank Transaction Reports

Most banks offer detailed spending summaries through online banking platforms.

Spreadsheets

Simple spreadsheets provide flexibility and allow complete control over financial data.

Financial Journals

Some people prefer manually recording purchases to increase spending awareness.

Build a Weekly Review Habit

One of the easiest ways to improve financial awareness is to review transactions once per week.

A weekly review helps:

- Catch unnecessary spending early

- Stay within budget limits

- Monitor progress toward financial goals

- Prevent financial surprises

This habit requires only a few minutes but can significantly improve money management.

Consistency Is More Important Than Perfection

Many people abandon expense tracking because they miss a few days or make mistakes.

The goal is not perfection.

The goal is awareness and consistency.

Even simple tracking methods can provide valuable insights and lead to better financial decisions over time.

Hidden Money Habit #8: Delaying Investing

One of the most expensive financial mistakes people make is delaying investing. Many individuals believe they need a large amount of money before they can begin investing, while others wait until they feel more financially secure. Unfortunately, postponing investment decisions can significantly reduce long-term wealth-building opportunities.

The biggest advantage an investor has is not necessarily a high income or expert market knowledge. Instead, it is time. The earlier someone starts investing, the more opportunity their money has to grow through the power of compound returns.

Even small investments made consistently over many years can potentially grow into substantial amounts. Conversely, waiting several years to start investing often requires much larger contributions later to achieve the same financial goals.

Why Delaying Investing Is Expensive

Many people underestimate the value of starting early.

When investing is delayed, individuals may experience:

- Lost growth opportunities

- Smaller retirement savings

- Reduced investment returns

- Slower wealth accumulation

- Greater pressure to save later in life

The years spent waiting cannot be recovered. Every year that passes without investing reduces the amount of time available for long-term growth.

The Power of Time in Investing

Time allows investments to benefit from compounding.

Compounding occurs when:

- Investments generate returns

- Those returns remain invested

- Future returns are earned on both the original investment and previous gains

Over long periods, compounding can become one of the most powerful tools for building wealth.

This is why starting early often matters more than investing large amounts later. Hidden Money Habits

Common Reasons People Delay Investing

Although investing offers significant long-term benefits, many people postpone getting started.

Fear of Losing Money

Market fluctuations can make investing seem risky, causing some individuals to avoid investing entirely.

However, avoiding investing carries its own risk—the risk of missing long-term growth opportunities.

Lack of Financial Knowledge

Many beginners feel overwhelmed by investment terminology and financial concepts.

As a result, they delay taking action while waiting to learn more.

Waiting for the “Perfect Time”

Some investors attempt to predict the best time to enter the market.

Unfortunately, consistently timing the market is extremely difficult, even for professionals.

Believing They Need More Income

Many people assume investing is only for high-income earners.

In reality, consistent contributions often matter more than the size of individual investments.

The Cost of Waiting

Imagine two individuals with similar financial goals.

One starts investing immediately.

The other waits several years before beginning.

Even if both eventually invest the same amount each month, the person who started earlier often accumulates significantly more wealth because their investments had more time to grow.

This demonstrates why delaying investing can become one of the most expensive financial habits.

How to Get Started With Investing

Investing does not need to be complicated.

The most important step is developing a long-term plan and starting as early as possible.

Learn Basic Investment Principles

Understanding concepts such as:

- Diversification

- Risk management

- Long-term growth

- Asset allocation

can help build confidence and improve decision-making.

Set Clear Financial Goals

Determine what you are investing for:

- Retirement

- Home ownership

- Financial independence

- Education expenses

- Long-term wealth building

Clear goals provide motivation and direction.

Contribute Consistently

Regular investing helps build discipline and reduces the temptation to wait for perfect market conditions.

Consistency often produces better results than attempting to predict short-term market movements.

Think Long Term

Successful investors typically focus on years and decades rather than days and weeks.

Short-term market fluctuations are normal, but long-term investing strategies are generally built around patience and consistency.

Investing vs Saving

Saving and investing both play important roles in financial planning.

Savings are ideal for: Hidden Money Habits

- Emergency funds

- Short-term goals

- Immediate financial needs

Investing is generally more suitable for:

- Retirement planning

- Long-term wealth accumulation

- Financial growth over time

A balanced financial strategy often includes both savings and investments.

Build the Habit Early

Financially successful individuals often treat investing as a regular habit rather than an occasional activity.

They:

- Invest consistently

- Stay focused on long-term goals

- Continue learning

- Avoid emotional decision-making

Over time, these habits can create significant financial advantages.

The Compound Effect of Hidden Money Habits

Each hidden money habit may appear small on its own.

However, when multiple habits occur simultaneously, the financial impact becomes significant.

For example:

- Unused subscriptions

- Daily convenience spending

- High-interest debt

- Lack of savings

- Delayed investing

Combined, these habits can cost thousands of dollars annually.

The good news is that small improvements can also compound over time.

A few positive financial habits practiced consistently can dramatically improve long-term financial outcomes.

Financial Habits of Wealth Builders

People who build long-term financial stability often share similar behaviors.

They:

- Track expenses regularly

- Save consistently

- Avoid unnecessary debt

- Invest for the future

- Live below their means

- Review financial goals frequently

Most importantly, they understand that financial success results from daily habits rather than occasional decisions.

Small actions repeated over many years often create extraordinary results.

How to Audit Your Spending Habits

Identifying hidden money habits begins with conducting a personal financial audit. Many people are surprised when they discover how much money is spent on unnecessary purchases throughout a typical month.

A spending audit helps reveal:

- Unnecessary expenses

- Overspending categories

- Subscription waste

- Saving opportunities

- Budget leaks

Step 1: Review the Last 90 Days

Start by examining:

- Bank statements

- Credit card transactions

- Mobile payment history

- Subscription charges

A 90-day review provides a realistic picture of spending behavior.

Step 2: Categorize Every Expense

Create categories such as:

- Housing

- Utilities

- Transportation

- Groceries

- Dining out

- Entertainment

- Shopping

- Subscriptions

This process helps identify where most money is going.

Step 3: Identify Financial Leaks

Look for expenses that:

- Provide little value

- Occur repeatedly

- Can be reduced easily

Examples include:

- Unused subscriptions

- Excessive food delivery

- Frequent impulse purchases

- Convenience fees

Step 4: Create an Improvement Plan

After identifying problem areas:

- Set spending limits

- Reduce unnecessary expenses

- Increase savings contributions

- Monitor progress monthly

Small improvements can produce significant long-term results.

The 30-Day Money Habit Challenge

Improving your finances does not require dramatic changes overnight. In most cases, lasting financial success comes from small, consistent actions repeated over time. The purpose of this 30-Day Money Habit Challenge is to help you build better financial habits, increase awareness of your spending, and create a stronger foundation for long-term financial security.

By focusing on one area of personal finance each week, you can gradually develop habits that support smarter money management and long-term wealth building. Hidden Money Habits

Week 1: Build Financial Awareness

The first step toward improving your finances is understanding your current spending behavior. Many people underestimate how much they spend because they rarely review their transactions closely.

Focus

Understand where your money is going.

Tasks

- Track every expense for seven days

- Review bank account balances daily

- Monitor credit card activity

- Avoid unnecessary purchases

- Record spending categories

Goal

Develop awareness of spending patterns and identify areas where money may be leaking unnecessarily.

Why It Matters

You cannot improve what you do not measure. Financial awareness provides the foundation for every other money habit discussed in this guide.

Week 2: Reduce Financial Waste

Once you understand your spending habits, the next step is eliminating unnecessary expenses that provide little value.

Focus

Identify and reduce financial leaks.

Tasks

- Cancel unused subscriptions

- Reduce food delivery expenses

- Limit dining out

- Avoid impulse purchases

- Compare recurring monthly bills

Goal

Keep more money available for savings, investments, and important financial goals.

Why It Matters

Even small reductions in spending can create significant annual savings when practiced consistently.

For example:

- Saving $10 per day

- Approximately $300 per month

- Approximately $3,600 per year

Small changes often produce surprisingly large results.

Week 3: Build Better Money Habits

With wasteful spending under control, focus on creating systems that make smart financial decisions automatic.

Focus

Establish positive financial routines.

Tasks

- Create a weekly budget review process

- Set realistic savings goals

- Automate transfers to savings accounts

- Review financial priorities

- Establish monthly spending limits

Goal

Make money management easier and more consistent.

Why It Matters

Successful financial management depends less on motivation and more on systems. Automating good financial behaviors reduces the risk of making poor decisions.

Week 4: Plan for the Future

The final week focuses on long-term financial security and preparing for future financial challenges.

Focus

Strengthen long-term financial planning.

Tasks

- Review financial goals

- Increase emergency fund contributions

- Evaluate debt repayment progress

- Review investment plans

- Set goals for the next 90 days

Goal

Build greater financial stability and future preparedness.

Why It Matters

Long-term planning helps ensure that today’s financial decisions support tomorrow’s goals.

Whether your objective is:

- Financial freedom

- Retirement planning

- Debt elimination

- Home ownership

- Wealth building

planning ahead increases the likelihood of success.

How to Measure Your Progress

At the end of the challenge, evaluate:

- How much spending awareness improved

- How many unnecessary expenses were eliminated

- Whether savings increased

- Progress toward financial goals

- Improvements in budgeting consistency

Even small improvements indicate meaningful progress.

The Real Purpose of the Challenge

The goal is not perfection.

The goal is developing habits that support long-term financial success.

Many people attempt major financial changes and give up quickly. This challenge focuses on sustainable improvements that can be maintained long after the 30 days are complete.

By completing this challenge, you will gain greater control over your finances, improve financial awareness, and create habits that can positively impact your financial future for years to come.

Common Financial Myths That Cost People Money

Many hidden money habits are reinforced by financial myths.

Myth #1: I Earn Too Little to Save

Many people believe saving is only possible with a high income.

In reality, consistent saving habits matter more than income level.

Even small contributions can grow over time.

Myth #2: Small Purchases Don’t Matter

This myth is responsible for countless budgeting problems.

Small expenses repeated daily can cost thousands annually.

Tracking spending reveals their true impact.

Myth #3: More Income Automatically Solves Financial Problems

Higher income helps, but poor money habits often continue regardless of earnings.

Without financial discipline:

- Spending increases

- Savings remain low

- Debt persists

Therefore, behavior matters as much as income. Hidden Money Habits

Myth #4: Budgeting Is Too Restrictive

Many people avoid budgeting because they think it eliminates enjoyment.

A good budget actually creates freedom.

It allows individuals to spend confidently while protecting financial goals.

Myth #5: Investing Is Only for Wealthy People

Modern investing platforms allow individuals to start with relatively small amounts.

The most important factor is starting early and investing consistently.

Frequently Asked Questions

What is the most expensive hidden money habit?

Failing to track expenses is often the most costly habit because it allows many other financial problems to go unnoticed.

How much should I save each month?

Many financial experts recommend saving at least 20% of income when possible, although the ideal amount depends on personal circumstances.

How often should I review my finances?

A weekly review helps maintain awareness, while a detailed monthly review supports long-term planning.

Are subscriptions really a major problem?

Yes. Multiple small subscriptions can add up to hundreds or even thousands of dollars annually.

Can small money habits really affect wealth?

Absolutely. Small financial decisions repeated consistently often determine long-term financial success.

Conclusion: The Hidden Money Habits That Are Quietly Costing You Thousands in 2026

Financial success is rarely determined by a single major decision. Instead, it is shaped by the habits practiced every day. The hidden money habits discussed throughout this guide may seem small individually, yet their cumulative effect can quietly cost thousands of dollars over time.

Ignoring small purchases, allowing subscriptions to accumulate, increasing spending with income growth, relying on emotional spending, neglecting emergency savings, carrying high-interest debt, failing to track expenses, and delaying investing are all habits that can limit financial progress.

Fortunately, these habits can be changed. By becoming more aware of spending behavior, creating a realistic budget, tracking expenses consistently, prioritizing savings, and planning for the future, individuals can regain control of their finances and build stronger long-term financial security.

The key is not perfection. The key is consistency. Small positive financial habits practiced every day can create powerful results over time. The sooner these hidden money leaks are identified and corrected, the easier it becomes to save more, reduce financial stress, and move closer to lasting financial freedom in 2026 and beyond.