Hook Introduction

Online Banking Safety Tips: Imagine waking up on a Monday morning, checking your bank account, and discovering that thousands of dollars have disappeared overnight.

You never shared your debit card. You never gave anyone your banking password. Yet somehow, criminals gained access to your account and transferred your money elsewhere.

Unfortunately, scenarios like this are becoming increasingly common.

Online banking has transformed the way we manage money. Today, people can deposit checks, transfer funds, pay bills, monitor investments, and apply for loans directly from their smartphones. What once required a visit to a bank branch can now be completed in seconds from virtually anywhere.

This convenience has made online banking an essential part of modern life.

However, the same technology that makes banking easier also creates opportunities for cybercriminals.

Hackers, scammers, and identity thieves are constantly developing new techniques to target consumers. They use fake emails, fraudulent websites, malicious software, and increasingly sophisticated social engineering tactics to gain access to sensitive financial information.

In 2026, protecting your bank account requires more than simply creating a password and hoping for the best.

Whether you use:

- Mobile banking apps

- Online money transfers

- Digital payment platforms

- Automatic bill payments

- Investment and savings accounts

understanding online banking safety has become a critical financial skill.

The good news is that most banking fraud can be prevented when consumers understand the risks and follow smart security practices.

Before learning the specific strategies that help keep your money safe, it’s important to understand why Online Banking Safety Tips security matters more today than ever before.

Why Online Banking Security Matters More in 2026

Online banking fraud is not a niche problem affecting only a few unlucky victims.

It has become a global issue that impacts millions of consumers every year.

Several trends are making banking security increasingly important.

Increasing Cybercrime

Cybercriminals have become more organized and sophisticated.

Many hacking operations now function like legitimate businesses. Criminal groups purchase stolen credentials, sell personal information, and even offer fraud services to other criminals.

The result is an increasingly professional cybercrime industry that actively targets financial accounts.

Mobile Banking Growth

More consumers now access their bank accounts through smartphones than traditional desktop computers.

Mobile banking is incredibly convenient, but it also creates new security challenges.

Lost phones, insecure apps, and unsafe networks can expose sensitive information if users are not careful.

AI-Powered Scams

Artificial intelligence has changed the cybersecurity landscape.

Scammers can now generate realistic emails, text messages, voice recordings, and fake customer support conversations that appear legitimate.

Many fraudulent communications are becoming difficult to distinguish from genuine bank messages.

Phishing Attacks

Phishing remains one of the most effective fraud methods.

A criminal may send an email claiming to be from your bank and ask you to verify account information.

The message often creates urgency by claiming:

- Your account is locked

- Suspicious activity was detected

- Immediate action is required

Many victims unknowingly provide usernames, passwords, and security codes directly to scammers.

Identity Theft

Personal information has become extremely valuable.

Criminals use stolen identities to:

- Open financial accounts

- Apply for loans

- Access banking services

- Conduct fraudulent transactions

Protecting your banking information helps protect your broader financial identity as well.

Common Online Banking Safety Tips Threats

Understanding common threats is the first step toward preventing fraud.

Let’s examine the risks consumers face most often.

Phishing Scams

Phishing scams attempt to trick people into revealing sensitive information.

These attacks commonly arrive through:

- Text messages

- Social media messages

- Fake customer support contacts

A phishing message may appear to come directly from a trusted financial institution.

The goal is usually to convince the victim to click a link and enter banking credentials.

Real-World Example

You receive a text message stating:

“Your bank account has been temporarily suspended. Click here to restore access.”

The website looks identical to your bank’s website.

However, the login page is controlled by criminals who capture your username and password.

Within minutes, your account could be compromised.

Malware Attacks

Malware refers to malicious software designed to steal information or damage devices.

Hackers often distribute malware through:

- Infected downloads

- Fake software updates

- Suspicious email attachments

- Fraudulent websites

Some malware programs specifically target banking information.

They can record keystrokes, capture passwords, and monitor online activity without the user’s knowledge.

Why It Matters

Even a strong password cannot protect your account if malware is secretly recording everything you type.

Fake Banking Apps

Mobile banking apps are popular targets for cybercriminals.

Fraudsters sometimes create counterfeit applications that imitate legitimate banking apps.

These fake apps may appear authentic and include:

- Official logos

- Similar designs

- Professional-looking interfaces

Once installed, they may collect login credentials and other sensitive information.

Warning Sign

If an app has very few downloads, poor reviews, or requests excessive permissions, proceed with caution.

Public Wi-Fi Risks

Public Wi-Fi networks are convenient but can introduce significant security risks.

Networks found in:

- Airports

- Hotels

- Coffee shops

- Shopping centers

may not provide adequate protection.

Cybercriminals can sometimes intercept data transmitted over unsecured networks.

This means banking information could potentially be exposed while using public Wi-Fi.

Example

A traveler logs into Online Banking Safety Tips while waiting at an airport.

If the network is compromised, sensitive information may be visible to attackers monitoring traffic.

Password Theft

Weak passwords remain one of the most common security vulnerabilities.

Many people still use passwords that are:

- Short

- Predictable

- Reused across multiple accounts

Examples include:

- Password123

- Welcome123

- Birthdates

- Pet names

If one website experiences a data breach, criminals often attempt the same credentials across multiple services, including banking platforms.

How Hackers Target Bank Accounts

Many people imagine hackers as highly skilled programmers breaking into bank systems. In reality, most banking fraud happens because criminals trick users into giving away information voluntarily.

Understanding how cybercriminals operate can help you avoid becoming a victim.

Credential Theft

Credential theft occurs when scammers steal your:

- Username

- Password

- Security questions

- Authentication codes

Hackers obtain this information through phishing emails, fake websites, malware, and data breaches.

Real-World Example

A user receives an email claiming to be from their bank. The email asks them to verify their account information after “suspicious activity” is detected.

The login page looks legitimate.

After entering their credentials, the information goes directly to the criminal.

Within minutes, unauthorized transactions begin appearing.

Data Breaches

Data breaches occur when companies storing customer information are hacked.

Although banks invest heavily in security, third-party companies may not have the same protections.

Stolen information can include:

- Email addresses

- Passwords

- Phone numbers

- Financial information

Cybercriminals often use this data to attempt access to banking accounts.

Why It Matters

Even if your bank remains secure, compromised information from another website could still expose your financial accounts if you reuse passwords.

Social Engineering

Social engineering relies on psychology rather than technology.

Scammers manipulate emotions such as:

- Fear

- Urgency

- Trust

- Curiosity

The goal is to convince victims to take actions they normally wouldn’t.

Example

A caller claims to be from your bank’s fraud department and says your account is under attack.

To “protect” your money, they ask you to provide a verification code sent to your phone.

That code actually gives them access to your account.

Fake Websites

Fake banking websites remain one of the most effective Online Banking Safety Tips scams.

Criminals create websites that closely resemble legitimate banking portals.

Many users fail to notice subtle differences in:

- Web addresses

- Security certificates

- Login pages

Once credentials are entered, attackers gain access to the account.

Safety Reminder

Always type your bank’s website address directly into your browser instead of clicking links in emails or text messages.

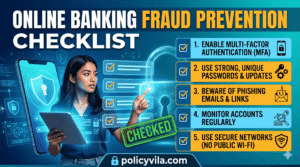

Smart Banking Safety Tip #1: Use Strong Passwords

A strong password remains one of the most important defenses against account theft.

Many people still use weak passwords because they’re easy to remember.

Unfortunately, they’re also easy for criminals to guess.

Why It Works

Strong passwords significantly increase the difficulty of unauthorized access.

They protect accounts even when hackers have access to automated password-cracking tools.

Real-World Example

Compare these passwords:

Weak:

- Bank123

- Password1

Strong:

- M7$kP!29vQ@rL6#x

The stronger password could take years to crack while the weak one may take seconds.

Practical Implementation

Create passwords that:

- Are at least 12–16 characters long

- Include uppercase letters

- Include lowercase letters

- Include numbers

- Include symbols

Never reuse passwords across multiple accounts.

Smart Banking Safety Tip #2: Enable Two-Factor Authentication

Two-factor authentication (2FA) adds an additional security layer beyond your password.

Why It Works

Even if criminals steal your password, they still need a second verification method.

This dramatically reduces account takeover risk.

Real-World Example

A hacker obtains your password through a phishing scam.

When they attempt to log in, the bank requests a verification code sent to your phone.

Without that code, access is denied.

Practical Implementation

Enable:

- SMS verification

- Authentication apps

- Security keys

- Biometric verification when available

Always activate 2FA on financial accounts.

Smart Banking Safety Tip #3: Avoid Public Wi-Fi

Public Wi-Fi networks can expose sensitive data.

Why It Works

Hackers often target unsecured networks because users frequently access financial accounts while traveling.

Real-World Example

A customer checks their bank account at a coffee shop using free Wi-Fi.

An attacker on the same network intercepts unencrypted traffic.

Sensitive information may become exposed.

Practical Implementation

Use:

- Mobile data connections

- Trusted home networks

- VPN services when necessary

Avoid Online Banking Safety Tips on public networks whenever possible.

Smart Banking Safety Tip #4: Update Devices Regularly

Software updates often contain critical security fixes.

Why It Works

Outdated devices may contain vulnerabilities known to cybercriminals.

Updates close security gaps before attackers can exploit them.

Real-World Example

A smartphone operating system update patches a vulnerability that could allow malware installation.

Users who delay updates remain vulnerable longer.

Practical Implementation

Enable automatic updates for:

- Smartphones

- Tablets

- Computers

- Banking apps

- Web browsers

Security updates should never be ignored.

Smart Banking Safety Tip #5: Use Official Banking Apps

Not all banking apps are legitimate.

Why It Works

Official apps are developed and monitored by your bank.

Fake apps may steal login credentials and personal information.

Real-World Example

A user downloads a counterfeit banking app from an unofficial source.

The app captures usernames and passwords before forwarding them to criminals.

Practical Implementation

Only download apps from:

- Apple App Store

- Google Play Store

- Your bank’s official website

Verify the publisher before installation.

Smart Banking Safety Tip #6: Verify Website URLs

Many scams rely on convincing victims to visit fraudulent websites.

Why It Works

A simple URL check can prevent credential theft.

Real-World Example

A phishing email links to:

Instead of:

The difference may seem small, but it changes everything.

Practical Implementation

Before entering login information:

- Check spelling carefully

- Verify HTTPS encryption

- Confirm the correct domain name

Never rush through login screens.

Smart Banking Safety Tip #7: Monitor Account Activity

Many fraud victims discover problems too late.

Why It Works

Early detection limits potential losses.

The sooner suspicious activity is identified, the faster banks can respond.

Real-World Example

A customer notices a $12 charge from an unfamiliar merchant.

Because they catch it immediately, the bank freezes the card before larger fraudulent transactions occur.

Practical Implementation

Review:

- Checking accounts

- Savings accounts

- Credit card activity

- Transaction histories

at least once each week.

Many banks also offer instant transaction alerts that provide real-time monitoring.

Smart Banking Safety Tip #8: Avoid Clicking Suspicious Links

One careless click can compromise an entire bank account.

Cybercriminals often use fake emails, text messages, and social media messages containing malicious links designed to steal personal information.

Why It Works

Avoiding suspicious links prevents you from visiting fake websites that capture login credentials or install malware.

Real-World Example

You receive a text message claiming:

“Your bank account has been locked. Click here immediately to restore access.”

The message looks legitimate, but the link leads to a fake banking portal controlled by scammers.

Practical Implementation

- Never click banking links in emails or texts.

- Type your bank’s website directly into your browser.

- Verify suspicious messages by contacting your bank directly.

- Delete unexpected banking messages immediately.

Smart Banking Safety Tip #9: Secure Mobile Devices

Your smartphone is essentially a portable banking center.

Many people use it for:

- Mobile banking

- Digital payments

- Credit card management

- Investment accounts

Protecting your device means protecting your money.

Why It Works

A secure device creates another barrier between cybercriminals and your financial information.

Real-World Example

A phone is stolen from a restaurant.

Without screen locks and security protections, the thief gains access to banking apps already logged in.

Practical Implementation

Enable:

- Strong screen locks

- Fingerprint authentication

- Face recognition

- Remote device tracking

- Remote data wipe features

Never leave banking devices unattended.

Smart Banking Safety Tip #10: Set Banking Alerts

Many consumers discover fraud days or even weeks after it occurs.

Banking alerts help you detect suspicious activity immediately.

Why It Works

Instant notifications allow faster response times.

The faster fraud is reported, the easier it becomes to limit losses.

Real-World Example

A customer receives a transaction alert for a $900 purchase they never made.

Within minutes they contact the bank and stop additional fraudulent charges.

Practical Implementation

Enable alerts for:

- Large transactions

- Debit card purchases

- Online transfers

- Password changes

- Login attempts

Most banks provide these services free of charge.

Smart Banking Safety Tip #11: Use Biometric Authentication

Biometric security has become one of the most effective protections available.

Instead of relying solely on passwords, access is verified using unique physical characteristics.

Why It Works

Biometric information is difficult to duplicate.

Unlike passwords, fingerprints cannot easily be guessed or stolen.

Real-World Example

A criminal obtains your banking password through a phishing attack.

They still cannot access the account because fingerprint verification is required.

Practical Implementation

Enable:

- Fingerprint login

- Facial recognition

- Voice authentication when available

Use biometric security whenever your bank supports it.

Smart Banking Safety Tip #12: Avoid Shared Devices

Shared computers create unnecessary risks.

You have little control over their security settings or software.

Why It Works

Public or shared devices may contain malware capable of recording banking information.

Real-World Example

A traveler logs into Online Banking Safety Tips using a hotel business center computer.

Unknown to them, keylogging software records every keystroke.

Practical Implementation

Avoid Online Banking Safety Tips on:

- Public computers

- Hotel computers

- Internet cafés

- Shared workplace devices

Use your own trusted device whenever possible.

Smart Banking Safety Tip #13: Protect Personal Information

Many scammers don’t hack accounts directly.

Instead, they collect personal details and use them to impersonate victims.

Why It Works

The less information criminals have, the harder it becomes for them to bypass security measures.

Real-World Example

A scammer learns a victim’s:

- Birthday

- Phone number

- Address

- Mother’s maiden name

Using this information, they successfully answer account recovery questions.

Practical Implementation

Avoid sharing sensitive information publicly, including:

- Full birthdates

- Home addresses

- Account details

- Personal identification numbers

Be especially cautious on social media.

Smart Banking Safety Tip #14: Review Statements Frequently

Many people only review statements when preparing taxes or balancing accounts.

This habit can allow fraud to continue unnoticed.

Why It Works

Frequent reviews help identify suspicious activity before significant damage occurs.

Real-World Example

A customer notices several unauthorized $7 subscription charges.

Although small, the charges reveal that card information has been compromised.

Practical Implementation

Review:

- Monthly statements

- Weekly transactions

- Credit card activity

- Automated payments

Look for charges you do not recognize.

Small fraudulent charges often appear before larger theft attempts.

The Psychology Behind Online Banking Safety Tips Scams

Understanding technology is important.

Understanding human psychology is equally important.

Most successful scams exploit human emotions rather than technical vulnerabilities.

Cybercriminals study behavior carefully because emotions often override logic.

Urgency Tactics

Scammers create artificial urgency to force quick decisions.

Common examples include:

- “Your account will be closed today.”

- “Immediate action is required.”

- “Suspicious activity detected.”

Why It Works

When people feel pressured, they spend less time evaluating risks.

They react emotionally instead of logically.

How to Defend Yourself

Pause before taking action.

Legitimate banks rarely demand immediate responses through email or text messages.

Fear-Based Scams

Fear is one of the strongest psychological motivators.

Criminals frequently use fear to manipulate victims.

Examples include threats involving:

- Account suspension

- Fraud investigations

- Identity theft

- Legal action

Why It Works

Fear encourages people to comply quickly.

Victims often provide information simply to make the perceived threat disappear.

How to Defend Yourself

Verify claims independently through official bank contact channels.

Never trust threatening messages at face value.

Trust Manipulation

Scammers often impersonate trusted organizations.

These may include:

- Banks

- Government agencies

- Credit card companies

- Financial institutions

Why It Works

People naturally trust familiar brands and authority figures.

Criminals exploit that trust.

How to Defend Yourself

Verify communications directly through official websites and customer service numbers.

Never rely solely on information provided in the message itself.

Social Engineering

Social engineering combines psychology and deception.

Instead of hacking systems, criminals manipulate people.

They may pretend to be:

- Bank representatives

- Technical support agents

- Fraud investigators

- Family members

Why It Works

Humans are naturally helpful and cooperative.

Social engineers exploit these tendencies.

Example

A scammer calls pretending to be from your bank’s fraud department.

They sound professional and knowledgeable.

They ask for a verification code “to secure your account.”

In reality, the code grants them access.

How to Defend Yourself

Remember:

Legitimate banks will never ask for passwords, PINs, or authentication codes over the phone.

If in doubt, hang up and call the bank directly.

Smart Banking Safety Tip #15: Use Secure Networks

The network you use is just as important as the device you use.

Hackers often target unsecured internet connections because they’re easier to exploit than protected home networks.

Why It Works

Secure networks reduce the chances of attackers intercepting sensitive information during banking sessions.

Real-World Example

Two people log into Online Banking Safety Tips.

One uses a password-protected home Wi-Fi network.

The other uses an unsecured public hotspot.

The second person faces significantly greater risk of data interception.

Practical Implementation

- Use trusted home Wi-Fi whenever possible.

- Secure your router with a strong password.

- Enable WPA3 or WPA2 encryption.

- Avoid unknown public networks.

- Use a VPN when traveling.

Smart Banking Safety Tip #16: Log Out After Banking

Many people simply close their browser or app without logging out.

While convenient, this habit creates unnecessary risk.

Why It Works

Logging out ends active sessions and prevents unauthorized access.

Real-World Example

A user leaves a shared tablet unlocked after checking account balances.

Another person gains access to the open banking session.

Practical Implementation

- Log out after every banking session.

- Close browser windows completely.

- Avoid selecting “Remember Me” on shared devices.

Small habits like this provide meaningful protection.

Smart Banking Safety Tip #17: Back Up Important Data

Most people associate backups with photos and documents.

Financial information is equally important.

Why It Works

Backups help you recover critical information if devices are lost, stolen, damaged, or infected with malware.

Real-World Example

A ransomware attack locks a user’s computer.

Fortunately, important financial records were backed up and easily restored.

Practical Implementation

Back up:

- Financial documents

- Tax records

- Account statements

- Insurance documents

Use:

- Cloud storage

- External drives

- Secure encrypted backup solutions

Smart Banking Safety Tip #18: Freeze Credit When Necessary

A credit freeze prevents criminals from opening new accounts using your identity.

Why It Works

Even if scammers obtain personal information, lenders cannot access your credit file without authorization.

Real-World Example

After a major data breach, a consumer freezes their credit.

Months later, criminals attempt to open several credit accounts but are denied.

Practical Implementation

Consider a credit freeze if:

- You experience identity theft.

- Sensitive information is exposed.

- You don’t plan to apply for credit soon.

Credit freezes can usually be lifted temporarily when needed.

Smart Banking Safety Tip #19: Learn Scam Warning Signs

Many scams follow predictable patterns.

Recognizing warning signs can stop fraud before it starts.

Why It Works

Awareness reduces emotional reactions and encourages rational decision-making.

Common Warning Signs

- Urgent requests

- Threats

- Requests for passwords

- Requests for verification codes

- Unexpected account alerts

- Too-good-to-be-true offers

Real-World Example

A caller claims your bank account is under attack and demands immediate action.

The urgency itself is a major warning sign.

Practical Implementation

Pause before responding.

Verify claims independently through official channels.

Smart Banking Safety Tip #20: Verify Bank Communications

Modern scams are becoming increasingly realistic.

Many fake emails and text messages look nearly identical to legitimate communications.

Why It Works

Independent verification eliminates guesswork.

Real-World Example

You receive an email requesting account verification.

Instead of clicking the link, you log into your bank directly and discover no issues exist.

The email was fraudulent.

Practical Implementation

Always verify through:

- Official websites

- Customer service numbers

- Banking apps

Never trust contact information included in suspicious messages.

Smart Banking Safety Tip #21: Educate Family Members

Your security is only as strong as the weakest link.

Family members often become targets because scammers assume they may be less informed.

Why It Works

Educated households identify scams more quickly and make safer decisions.

Real-World Example

A teenager receives a phishing text pretending to be from a bank.

Because the family previously discussed fraud prevention, the scam is immediately recognized.

Practical Implementation

Discuss:

- Common scams

- Safe password practices

- Fraud warning signs

- Secure online behavior

Regular conversations help everyone stay protected.

The Biggest Online Banking Mistakes People Make

Even security-conscious consumers occasionally make mistakes.

Understanding these common errors can help you avoid becoming a victim.

Mistake #1: Reusing Passwords

Why It Happens

It’s easier to remember one password.

Consequences

One compromised account can expose multiple accounts.

Better Alternative

Use unique passwords for every financial account.

Mistake #2: Ignoring Software Updates

Why It Happens

Updates can feel inconvenient.

Consequences

Unpatched vulnerabilities remain exposed.

Better Alternative

Enable automatic updates whenever possible.

Mistake #3: Clicking Links Without Verification

Why It Happens

Messages appear legitimate.

Consequences

Credential theft and malware infections.

Better Alternative

Visit banking websites directly.

Mistake #4: Using Public Wi-Fi for Banking

Why It Happens

Convenience.

Consequences

Potential data interception.

Better Alternative

Use secure networks or mobile data.

Mistake #5: Not Reviewing Account Activity

Why It Happens

Many people assume fraud won’t happen to them.

Consequences

Unauthorized transactions may continue unnoticed.

Better Alternative

Review accounts weekly.

Mistake #6: Saving Passwords on Shared Devices

Why It Happens

Faster access.

Consequences

Anyone using the device may gain account access.

Better Alternative

Disable password storage on shared systems.

Mistake #7: Ignoring Small Fraudulent Charges

Why It Happens

Small amounts seem insignificant.

Consequences

Small test charges often precede larger fraud attempts.

Better Alternative

Investigate every unfamiliar transaction.

Mistake #8: Sharing Too Much Online

Why It Happens

Social media encourages sharing.

Consequences

Scammers gather personal information.

Better Alternative

Limit public personal details.

Mistake #9: Trusting Caller ID

Why It Happens

People assume displayed numbers are genuine.

Consequences

Caller ID spoofing scams succeed.

Better Alternative

Hang up and call your bank directly.

Mistake #10: Delaying Fraud Reporting

Why It Happens

Uncertainty or procrastination.

Consequences

More financial damage may occur.

Better Alternative

Report suspicious activity immediately.

Modern Banking Scams in 2026

Online banking security has improved dramatically over the past decade, but so have the tactics used by cybercriminals. Today’s scams are more sophisticated, personalized, and convincing than ever before.

Understanding how modern scams work can help you recognize red flags before becoming a victim.

AI Voice Scams

Artificial intelligence has introduced a new threat known as voice cloning.

Scammers can now create realistic voice recordings that sound nearly identical to family members, coworkers, or even bank representatives.

How the Scam Works

A criminal obtains a short audio sample from social media, voicemail messages, videos, or online interviews.

AI software then recreates the person’s voice.

The victim receives a call that appears completely authentic.

Real-World Example

A parent receives a phone call that sounds exactly like their child claiming to be in an emergency and needing money immediately.

Because the voice sounds genuine, many victims act before verifying the situation.

Protection Tips

- Verify emergencies through another communication channel.

- Ask personal questions only the real person would know.

- Never transfer money based solely on a phone call.

SMS Banking Fraud

Text message scams continue to rise.

These attacks often appear to come directly from legitimate financial institutions.

Common Messages

- Suspicious account activity detected

- Debit card blocked

- Account verification required

- Security update needed

The goal is to convince users to click malicious links.

Protection Tips

- Never trust links in unexpected text messages.

- Open your banking app directly.

- Contact the bank through official channels.

QR Code Scams

QR codes have become extremely popular for payments and transactions.

Unfortunately, scammers have adapted quickly.

How It Works

Criminals replace legitimate QR codes with fraudulent versions.

Victims scan the code and unknowingly visit fake websites or authorize payments.

Example

A QR code placed on a public poster redirects users to a fake banking login page.

Protection Tips

- Verify QR codes before scanning.

- Avoid unknown payment QR codes.

- Review website addresses carefully.

Fake Customer Support Calls

Scammers frequently impersonate bank representatives.

These calls often sound professional and convincing.

Common Tactics

- Claiming suspicious activity

- Offering fraud protection

- Requesting verification codes

- Asking for account details

Protection Tips

Legitimate banks do not ask for:

- Passwords

- PIN numbers

- Full authentication codes

Hang up and call the official customer service number directly.

Crypto Payment Scams

Cryptocurrency-related fraud continues growing in 2026.

Many criminals exploit public interest in digital assets.

Common Schemes

- Fake investment opportunities

- Guaranteed returns

- Celebrity endorsements

- Urgent payment requests

Why They’re Dangerous

Crypto transactions are often irreversible.

Once funds are sent, recovery becomes extremely difficult.

Protection Tips

- Verify all investment opportunities.

- Avoid guaranteed-profit promises.

- Research platforms thoroughly.

Investment Fraud Schemes

Investment scams remain one of the most expensive forms of financial fraud.

Common Red Flags

- Guaranteed returns

- No risk claims

- Secret investment strategies

- Pressure to act immediately

Real-World Example

An investor is promised 25% monthly returns through an exclusive opportunity.

The scheme pays initial profits to gain trust before disappearing with larger investments.

Protection Tips

- Research investments independently.

- Verify licenses and registrations.

- Be skeptical of unusually high returns.

Online Banking Myths vs Facts

| Myth | Fact |

|---|---|

| My bank will always stop fraud automatically. | Banks help, but customers play a critical role in prevention. |

| Strong passwords alone provide complete protection. | Multiple security layers are necessary. |

| Hackers only target wealthy people. | Criminals target accounts of all sizes. |

| Mobile banking apps are unsafe. | Official apps are generally very secure when used properly. |

| Fraud is easy to detect immediately. | Some fraud remains unnoticed for weeks. |

| Public Wi-Fi is safe if a password is required. | Many public networks still carry risks. |

| Phishing emails are easy to recognize. | Modern phishing attacks can appear highly authentic. |

| Identity theft only affects older adults. | Victims exist in every age group. |

| Small transactions aren’t worth investigating. | Small charges often test stolen card information. |

| Cybersecurity is the bank’s responsibility only. | Security is a shared responsibility between banks and customers. |

Safe Banking Habits of Financially Smart People

People who rarely experience banking fraud often share similar habits.

These behaviors may seem simple, but together they create powerful protection.

They Check Accounts Regularly

Financially smart individuals monitor their accounts consistently.

They identify unusual activity before major losses occur.

Most review transactions:

- Daily

- Every few days

- Weekly at minimum

They Enable Every Available Security Feature

Many Online Banking Safety Tips customers ignore optional security settings.

Smart consumers activate:

- Two-factor authentication

- Login alerts

- Transaction notifications

- Biometric authentication

These tools provide multiple layers of protection.

They Verify Before Trusting

Smart Online Banking Safety Tips users understand that scammers rely on urgency.

Instead of reacting immediately, they verify information independently.

They never trust:

- Unexpected phone calls

- Unsolicited emails

- Random text messages

without confirmation.

They Keep Devices Secure

Safe banking starts with secure devices.

Financially responsible consumers:

- Update software regularly

- Use antivirus protection

- Lock devices with passwords

- Enable remote wipe features

They Separate Emotion From Financial Decisions

Scammers often manipulate emotions.

Smart consumers slow down when they encounter:

- Fear

- Urgency

- Excitement

- Pressure

This pause helps them evaluate situations logically.

They Educate Themselves Continuously

Cybersecurity evolves constantly.

Financially savvy individuals stay informed about:

- New scams

- Security threats

- Fraud prevention techniques

- Banking technology updates

Knowledge remains one of the strongest defenses against fraud.

read also: Loan Approval Process 2026: Hidden Factors Banks Never Explain

They Act Immediately When Something Seems Wrong

Successful fraud prevention often depends on speed.

When smart consumers notice suspicious activity, they:

- Contact their bank immediately

- Freeze affected cards

- Change passwords

- Review account activity

Quick action frequently prevents larger losses.

30-Day Online Banking Security Challenge

Improving your Online Banking Safety Tips security doesn’t require complicated technical knowledge. Small actions taken consistently can dramatically reduce your risk of fraud.

This 30-day challenge focuses on practical improvements that anyone can implement.

Week 1: Security Audit

The first week focuses on identifying vulnerabilities.

Day 1–2: Review Banking Accounts

Make a list of:

- Checking accounts

- Savings accounts

- Credit cards

- Investment accounts

- Payment apps

Many people forget how many financial accounts they actually use.

Day 3–4: Update Passwords

Change weak or reused passwords.

Create unique passwords for every financial account.

Day 5–6: Enable Two-Factor Authentication

Activate 2FA on all banking platforms.

Prioritize:

- Bank accounts

- Credit card portals

- Payment apps

Day 7: Review Security Questions

Replace predictable answers with stronger alternatives.

Avoid information publicly available on social media.

Week 2: Account Protection

Now that the basics are secure, strengthen account monitoring.

Day 8–10: Activate Banking Alerts

Enable notifications for:

- Login attempts

- Large purchases

- Wire transfers

- Password changes

Day 11–12: Review Connected Devices

Remove old devices no longer in use.

Examples include:

- Old smartphones

- Tablets

- Shared computers

Day 13–14: Verify Contact Information

Ensure your bank has your: Online Banking Safety Tips

- Current phone number

- Email address

- Mailing address

Accurate information helps fraud departments reach you quickly.

Week 3: Fraud Prevention

This week focuses on reducing exposure to scams.

Day 15–17: Review Recent Transactions

Look for:

- Unknown subscriptions

- Small test charges

- Duplicate transactions

Fraud often begins with small amounts.

Day 18–19: Clean Up Digital Accounts

Delete unused financial apps and accounts.

Every unused account represents potential risk.

Day 20–21: Learn Current Scam Tactics

Spend time reviewing:

- Banking fraud warnings

- Identity theft alerts

- Consumer protection resources

Awareness is one of the strongest defenses available.

Week 4: Long-Term Security Habits

The final week builds habits designed to protect you for years.

Day 22–24: Create a Security Routine

Schedule regular reviews of:

- Statements

- Alerts

- Credit reports

Consistency matters more than perfection.

Day 25–26: Back Up Financial Records

Secure copies of:

- Statements

- Tax documents

- Insurance records

Store them safely.

Day 27–28: Discuss Security With Family

Many scams target family members.

Share:

- Fraud warning signs

- Safe banking habits

- Emergency procedures

Day 29–30: Evaluate Progress

Review everything you’ve improved during the month.

Most people discover they are significantly more protected than when they started.

Expert Online Banking Safety Tips Security Tips

Financial security experts recommend these practical habits:

1. Never Reuse Banking Passwords

Your banking password should be unique.

2. Use a Password Manager

Strong passwords become easier to manage.

3. Enable Multi-Factor Authentication Everywhere

Every extra layer matters.

4. Review Accounts Weekly

Frequent monitoring improves fraud detection.

5. Avoid Public Charging Stations

Some compromised stations can steal data.

6. Lock Your Devices Automatically

Short lock timers improve security.

7. Keep Banking Apps Updated

Updates often contain security improvements.

8. Monitor Your Credit Reports

Identity theft frequently appears there first.

9. Be Skeptical of Urgent Requests

Scammers rely on panic.

10. Verify Before Responding

Always confirm through official channels.

11. Limit Personal Information Online

Reduce what criminals can learn.

12. Use Biometric Security

Fingerprints and facial recognition add protection.

13. Review App Permissions

Remove unnecessary access requests.

14. Avoid Storing Passwords in Browsers

Use dedicated password managers instead.

15. Report Suspicious Activity Immediately

Fast action often prevents larger losses.

read also:How Banks Really Decide Who Gets a Personal Loan in 2026

Frequently Asked Questions

Is online banking safe in 2026?

Yes. Online Banking Safety Tips is generally very safe when consumers follow proper security practices such as strong passwords, two-factor authentication, and account monitoring.

What is the biggest online banking threat today?

Phishing remains one of the most common threats because it relies on human behavior rather than technical vulnerabilities.

How do hackers steal bank account information?

They commonly use phishing attacks, malware, fake websites, social engineering, and stolen credentials from data breaches.

Should I use banking apps on public Wi-Fi?

It is best to avoid online banking on public Wi-Fi. Use mobile data, a trusted network, or a VPN instead.

What should I do if I suspect fraud?

Contact your bank immediately, freeze affected cards if necessary, change passwords, and review recent transactions.

Are banking apps safer than websites?

Official banking apps are generally very secure and often include additional security features such as biometric authentication.

How often should I check my bank account?

Weekly reviews are recommended, while daily monitoring provides even stronger protection.

Can banks recover stolen money?

Many banks offer fraud protection, but recovery depends on the circumstances and how quickly fraud is reported.

What should I do if I clicked a suspicious banking link?

Immediately change your banking password, contact your bank, review account activity, and scan your device for malware.

Is two-factor authentication really necessary?

Absolutely. Two-factor authentication remains one of the most effective ways to prevent unauthorized account access.

Final Thoughts

Online Banking Safety Tips has made managing money faster, easier, and more convenient than ever before. From paying bills to transferring funds and monitoring investments, digital banking is now a normal part of everyday life.

However, convenience comes with responsibility.

Cybercriminals continue developing new tactics designed to exploit both technology and human behavior. The good news is that most banking fraud can be prevented through awareness, preparation, and consistent security habits.

Strong passwords, two-factor authentication, secure devices, account monitoring, and healthy skepticism toward unexpected communications provide powerful protection against modern threats.

The goal isn’t to become a cybersecurity expert.

The goal is to build simple habits that make you a difficult target.